Expert Advice with Cam McLellan 10/11/2017

Type ‘Housing Affordability’ into Google and you’ll find a ton of doomsday headlines. A search today found headlines like ‘Housing affordability just got worse across Australia' and ‘Housing affordability set to be a problem for 40 years’.

With articles like these, it’s no wonder potential first home buyers are being put off. But what a lot of these articles fail to mention is the historical data of the Australian property market, which illustrates how entering the market has not changed much over the past 50 years.

Yes, Australian house prices have risen substantially but this doesn’t mean that houses are now unaffordable. It just means that prospective property buyers must be savvy and find an entry point into the market.

Why Australian housing is still affordable

Let’s face it: buying in blue chip areas was and will always be a stretch for new home buyers. These affluent, established, tree-lined suburbs are highly expensive and don’t make much sense for first home buyers.

Just as very few of us can afford to buy a Ferrari as our first car, young and aspiring property owners should not set their sights on fanciful and unattainable suburbs or properties straight away, but should instead focus on realistic targets.

This is the same principle property buyers have been grappling with since real estate was invented. What’s important is understanding the context and to see the property market for the vehicle that it is. Wealth is not generated overnight.

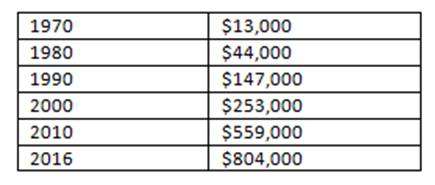

In a recent ‘Workout of the Day’ OpenCorp video, Michael Beresford breaks this down using Melbourne’s median house prices since 1970:

Melbourne Median House Prices:

In simple terms, let’s say that your parents (or grandparents) bought a property in Melbourne in 1970 for the median price of $13,000, with a loan of $11,000. In 1980, this property would be worth $44,000.

If they sold and upgraded their property, they would have at least $35,000 in cash due to the rising market. They decide to take a loan of $18,000, giving them $53,000 (more like $50,000 after stamp duty, solicitor’s fees etc.) to purchase a new house.

Assuming that they then upgrade their principal place of residence once a decade, they would today be able to afford a house well above the median Melbourne price range of $1.1m.

This not only helps us understand how to go about getting a foothold in the property market but also why the housing prices keep rising…a lot of people who did invest in property in past decades are constantly upgrading to something bigger and better.

What you can do to get a foot in the property market

Therefore, housing is still affordable. The principle hasn’t changed. Yes, the numbers have gotten larger but the property market is still the same slow process of capital and compound growth it was 50 years ago, as the above calculations indicate.

At OpenCorp, we believe new property investors should follow three principles, which are key to getting started in the property market:

• Making sacrifices with cash flow

• Delayed gratification

• Patience - real wealth isn’t created overnight

In today’s housing market climate, property buyers must chip away and work hard to get into a first home in a growth area. To select the right house, we use the M.A.P (Market, Area, Property) process to pinpoint good value investments in burgeoning areas during the ‘value’ phase of the property market cycle.

Once this is done, you can begin to pay down your mortgage and begin the process of developing equity, enabling you to upgrade your home every 10 years or so.

...............................................................................................

Director of OpenCorp, Cam McLellan is committed to sharing his passion and property investment knowledge with everyday Australians.

Director of OpenCorp, Cam McLellan is committed to sharing his passion and property investment knowledge with everyday Australians.

Cam started investing in real estate at a young age and quickly mastered the art of building sustainable wealth. He has used the same wealth building strategy to develop a multi-million dollar business. Cam has personally bought, sold and developed numerous properties and has an extensive residential and commercial investment portfolio.

Read more Expert Advice from Cam here!

Disclaimer: while due care is taken, the viewpoints expressed by contributors do not necessarily reflect the opinions of Your Investment Property.