The term might sound relatively new, but Arthur Naoumidis, CEO of DomaCom, says the strategy of fractional investing has been around for much longer than people might think.

“Syndication has been happening for 100 years or so at the rich end of town, where people go to their accountants and get private syndicates created. What we have done is democratise the syndication process, but it’s happening all over the world,” Naoumidis says.

Through DomaCom’s platform, you can invest in a property for as little as $1,000 after opening an account for a minimum of $2,500.

Naoumidis says “syndication drops the barrier to entry, but it also allows you to spread your risk”.

Naoumidis says “syndication drops the barrier to entry, but it also allows you to spread your risk”.

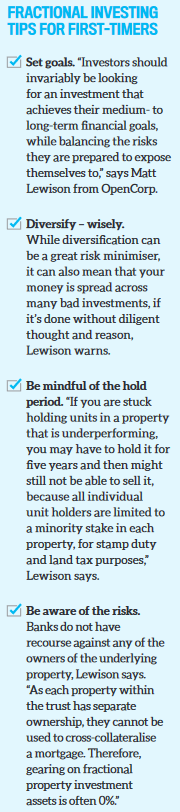

So, how does fractional investing work? As the name suggests, you buy a ‘fraction’ of a property in conjunction with thousands of other investors.

When investing a smaller amount of cash, investors shouldn’t lose focus on property being a long-term strategy.

“That’s the thing about diversification; you can take your investment portfolio and build an investment portfolio of properties – put $5,000 in this [property], $6,000 into that one, and over five years you have four or five properties across different locations that are growing,” Naoumidis explains.

Once investors gain a return from their units, they have the option to reinvest it through the platform and gradually accumulate a small fortune.

“If you’re saving your deposit in cash, it’s liquid but not returning much in this low-interest environment. But if you are saving it in property, it’s tracking property, so you are in the market that you are trying to buy into, which is a great way to build your deposit,” Naoumidis says.

“Each year you save another $1,000 or $2,000, and you just go into the secondary platform and offer to buy shares or units from the other owners, and then over time you are building up your ownership.”

Selling units to other investors

Like the fundamentals that govern demand and supply in the broader market, the same rules apply to the secondary market of fractional property investing.

“If your goal is to try to fast-track building up a deposit for your own investment property or for some other strategy that you have down the track, if you can’t sell in that secondary market, that’s where the risk potentially is,” says Ben Kingsley, director of Empower Wealth.

“Syndication has been happening for 100 years or so at the rich end of town ...we have democratised the process”

Also, if there happens to be a high volume of investors who want to sell their units, Kingsley says “potentially the cost of your unit in that particular fractional investment could be lower than you might have anticipated”.

While an investor can benefit at any time from the freedom of being able to offer their units up for sale, Naoumidis explains how another liquidity event can take place.

“When we crowdfund a syndicate, it has a life, which is normally five years, and at the end of the five years all of the investors vote to renew for another five years or not, and it’s got to be 100% to renew,” Naoumidis says.

In the case that you don’t want to renew, and the other investors do, Naoumidis says the investors will need to buy you out using the secondary market.

“We would value the property just before the vote,” he adds

Read more:

Low-cost ways to profit from property