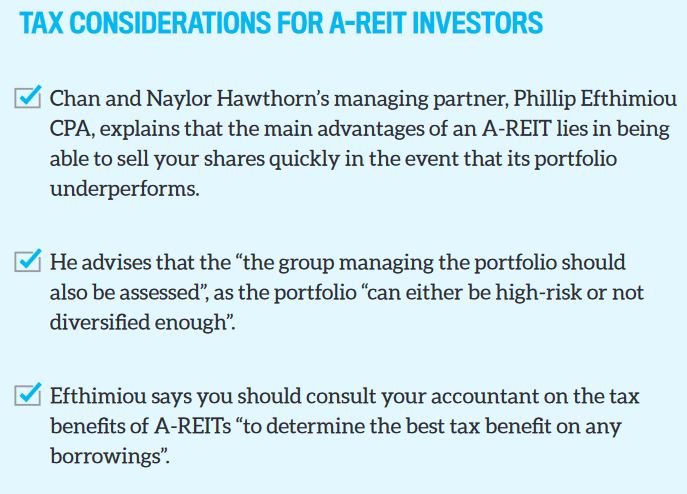

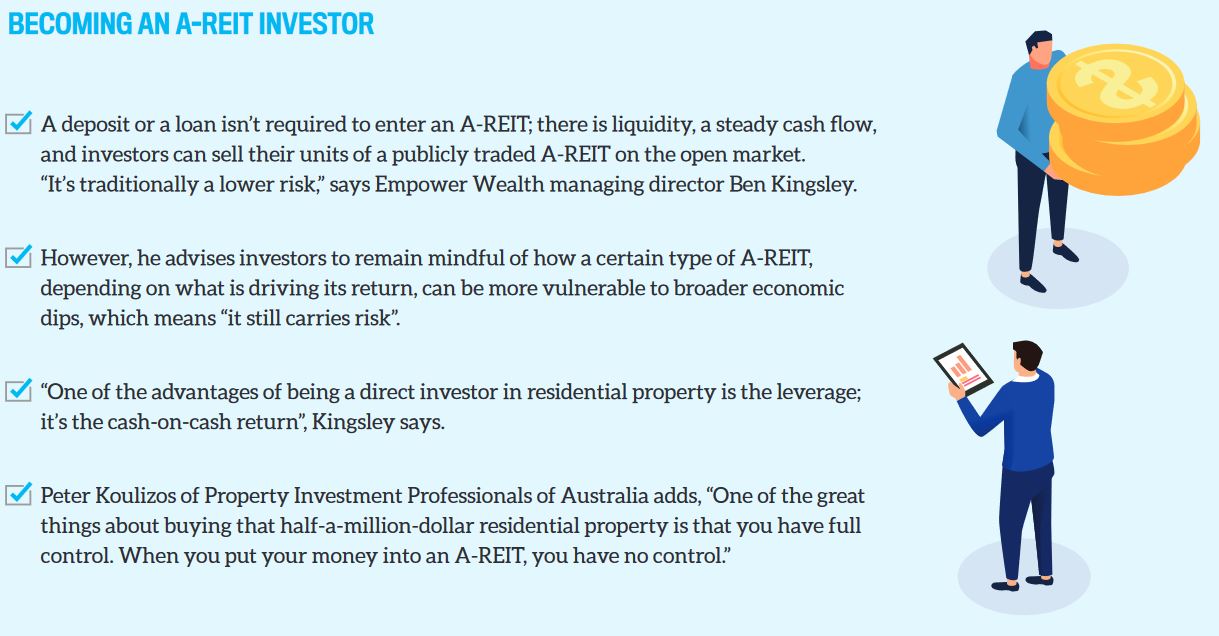

Investing in Australian Real Estate Investment Trusts (A-REITs) is an option for investors with a lower pool of capital, as you can get started with just a few hundred dollars in your bank account.

Paul Wilson of Income2Wealth says this opens up the opportunity for an investor to buy into an asset class that would otherwise be unreachable, as they are able to invest small amounts of capital.

“There is really no minimum – maybe, say, $500,” he says.

“If you are looking at Stocklands or commercial properties in general, then there are much larger acquisition costs, and the average person can’t get their foot in the door with those types of assets. So this allows them to tie themselves to an asset class – an asset particularly in commercial – that they probably wouldn’t have access to as an individual.”

Contributing money towards a diversified portfolio, ideally across more than one A-REIT, doesn’t require the investor to save for a massive property deposit and the other costly expenses that come with buying a property directly.

But Wilson says investors still need to do their own due diligence and “not assume that the A-REIT is a good investment just because it exists and is available for investors”.

“Investors have got to be able to do the research and understand what’s backing the actual investment they are going into. But they are also equally able to ride on the shoulders of experts who have done their high-level expertise in assessing and identifying opportunities,” Wilson says.

“Investors have got to be able to do the research ... but they are also able to ride on the shoulders of experts who have done their high-level expertise in assessing and identifying opportunities”

How to find a solid A-REIT

Commercial property can generate a considerable rental yield, allowing investors to pocket a steady income that exceeds what they earn from their residential investments.

"The cash flow you would get is fairly predictable, and most of the buildings have A-grade tenants and long-term leases,” says Ken Raiss, director at Metropole Wealth Advisory.

However, as A-REITs don’t tend to dabble in different property types, each one holds different risks for the investor.

“The listed [A-REIT] normally would have less risk than an unlisted one, and it has liquidity,” Raiss explains. “So for the listed one you can go in and buy and sell because there is a market, whereas with the unlisted one you are really bound by what the manager said they would do, and it might be that you can’t get your money back for five or 10 years.”

Empower Wealth founder and managing director Ben Kingsley adds that “it’s very uncommon to see structures of A-REITs in the residential space, because effectively the capital gains are a little bit lower, so you want to be careful of the types of A-REITs that are on offer”.

Paying attention to the broader economic climate is an “excellent observation”, he says.

“When we are talking about retail, we need to make sure that the foot traffic is really, really strong in a particular location, so the high-street retail has been struggling and there are potentially going to be changes in the way we buy and receive our goods,” Kingsley explains.

Recently evolving threats such as COVID-19, which have the potential to massively impact the economy and the retail sector in particular, are risks that investors need to consider in the short term.

Recently evolving threats such as COVID-19, which have the potential to massively impact the economy and the retail sector in particular, are risks that investors need to consider in the short term.

It’s also important to ensure that your investment strategy aligns with your goals. A-REITs are most attractive to those who want the extra cash flow, says Peter Koulizos, chairman of Property Investment Professionals of Australia (PIPA) and program director of the Master of Property at Adelaide University.

“A-REITs don’t necessarily have great capital growth. Capital growth of a commercial property is dependent on the rent that they collect. If you can’t increase the rent, you can’t increase the value, and generally you increase the rent because the owner or the A-REIT spends money on fixing [the asset] up,” Koulizos says.

While the costs of a facelift or a larger-scale improvement will come from the pool of invested cash, Wilson adds that this can work to drive demand and consequently boost the property’s performance.

“The investor will benefit from the fact that [the A-REIT is] upgrading the asset or they are manufacturing the asset because they are subdividing it, or they are increasing the yield or the value of the asset, so that type of investment should have a growth component, and they can manufacture that growth as well,” Wilson explains.

How to monitor an A-REIT

To minimise the risks of not only a volatile environment but the chance of a location or sector nosediving, an A-REIT will often disperse its asset base.

“Even if they are in the same sector, which is retail, but they’ve diversified into a number of different geographical locations and different types of shopping centres – so one might be large, one might be midsized – then it does give you some diversity,” Koulizos says.

However, Kingsley advises investors to pore over an A-REIT’s prospectus so they can be fully aware of what their invested cash will be tied to and what the fund’s future plans are for the underlying asset.

“What [the A-REIT’s] strategy is, what they are looking to do with that particular opportunity, what their focus is, what their angle is – all of those things are very well documented in those product disclosures and any of the sort of statements that they offer in terms of the investment strategy,” Kingsley says.

In most cases investors can expect dividends to be paid to them yearly or every six months, and in some instances quarterly, he says, but these specifics will also be outlined in the product disclosure statement.

Read more:

Low-cost ways to profit from property