HAVING AN interest-only loan is undoubtably the best option for investors as it keeps more money in their back pockets so they can reinvest.

That said, the point at which the investor most commonly needs to dig into those savings is when the interest-only period expires and they are suddenly required to start paying o the principal of their loan.

Over the last two years, lending restrictions have exacerbated stress for investors who find themselves in this position, because the kinds of loans and interest rates available to them have fluctuated so much. In addition, the servicing calculators used by the banks to determine a borrower’s ability to refinance or take on additional loans are the toughest I have seen in my 20 years in property.

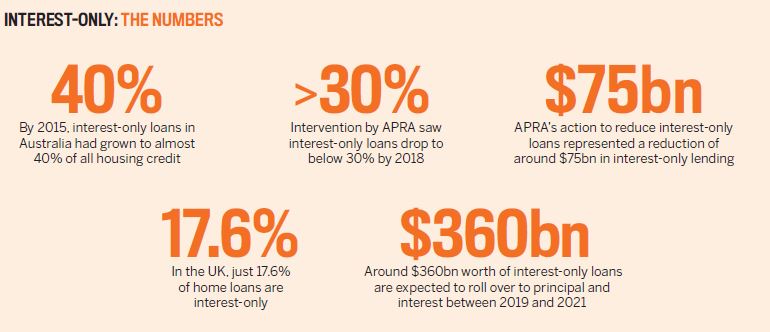

In 2015, interest-only loans accounted for 40% of all mortgages. As a result of market growth in Sydney especially this percentage increased to the point where, in February 2017, 60% of all loans applied for were interest-only.

This posed a significant risk to lending institutions as speculative investors were chasing quick returns at the top of the boom in Australia’s most expensive market. This effectively triggered the 2017 lending changes, whichI will elaborate on.

The Reserve Bank of Australia was quite vocal in its commentary in 2018 about the $360bn worth of interest-only loans due to expire over the next three years. This posed a new risk in a climate of softening median house prices and investor activity, especially for those investors who did not buy wisely and chased quick wins.

The truth about residential loans

Let’s be clear: $360bn is a huge number. But let me provide some context. The overall residential market in Australia comprises about 9.5 million residences worth a collective $7.4trn. Therefore, these interest-only renewals represent less than 5% in dollar value of the overall underlying asset base. It is understandable that APRA had to act with respect to lending restrictions, but in context it is not the doom and gloom you may be hearing in the media regarding availability of credit.

In March 2017, APRA restrictions required most lenders, including the big four banks, to have less than 30% of their loan book made up of interest-only loans. A ‘correction’ was necessary, and as an incentive to consumers the banks were offering appealingly low interest rates in order to move people over to principal and interest repayments.

This 30% restriction was lifted in December 2018, and banks are again warming to the prospect of interest-only loans. This is great news for investors, which is why I would like to offer some advice about what to do in this environment when your interestonly term is expiring,

I am a big believer in the big picture with respect to property investment, and feel that taking a long-term approach is the safest and most secure way to create financial freedom. Everything cycles in the short term, from interest rates to lending criteria, inflation, wages, rents and property prices in any number of different markets around the country.

Things may be tough now with respect to lending, but it won’t stay this way forever. Effective investment is about staying focused on what you can do right now to improve your portfolio, and remaining committed to your long-term goals.

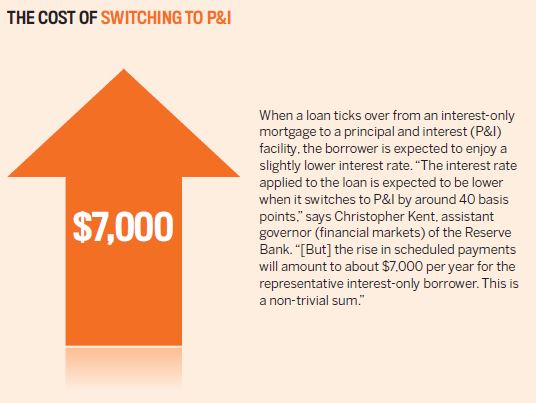

Due to the changes already discussed, as an investor you’ve probably been bombarded with loan offers by lenders trying to sell you on their competitive interest rates. However, low interest rates should not be your only priority. It is just as important to focus on loan features that can help you minimise out-of-pocket holding costs. After all, being forced to adopt a principal and interest loan repayment on a $500,000 loan amount at 4.5% per annum will add $659 to your monthly repayment. And because any principal repayment is not tax deductible, your holding cost will increase by the same amount. This is a lot of extra money, which is only compounded the larger the portfolio you have.

Three actions all investors must take

There are far better things you could be doing with your money than ploughing it into the principal repayments for your investment property loan – such as building your portfolio when your equity and borrowing capacity allow. The three things you need to do right now are:

- Become aware of when your interest-only period will expire.

- Review your loan structure and capacity to refinance.

- Engage a mortgage broker who is experienced in investment finance

Knowing when your interest-only period will expire gives you as much control as possible. Firstly, because banks are no longer required to keep interest-only loans to a minimum, you are more likely to be able to extend your interest-only period if you meet their servicing criteria than at any other point in the last two years.

However, the process for extending the interest-only period of your loan is more extensive than ever before. While a conversation with the bank or a ‘tick and flick’ approach may have worked in the past, a whole new application process now needs to be undertaken. A full credit review will be done by one of the bank’s credit assessment teams and you’ll be required to provide full supporting documentation, such as proof of income, liabilities and expenses.

Although it’s no more onerous than any other loan application process, it does take time, so make sure you allow for this before your existing interestonly loan term expires. Provided you meet the servicing criteria, however, an additional interestonly period of up to five years should be achievable.

Prevention is better than cure, so set a reminder for six to 12 months prior to your interest-only period ending and review your loan at that point. This will give you plenty of time to explore the market for your best option.

Being prepared allows you to make the necessary changes to your financial situation to maximise your chances of meeting the bank’s serviceability requirements once your interestonly term expires. Banks will generally want to see three months’ evidence of living expenses, but they may require as much as six months, so being prepared and minimising spending for a short period if necessary is possible when you plan in advance.

"Lending restrictions have exacerbated stress for investors [whose interest-only terms have expired] because the loans and interest rates available to them have fluctuated so much"

Opportunity to start afresh

If you have left your loans in place and not reviewed or changed them during the interest-only period, then the end of your interestonly loan term provides a great opportunity to review your current loan structure and potentially refinance to a new lender – with a brand-new interest-only period.

This also gives you the benefit of ensuring that the loan features you have are still meeting your needs, and you are being charged the most competitive interest rate.

You may be surprised to find that generally banks offer the most attractive rates to new customers, not existing ones. Being prepared to move your business to a new lender can often result in securing a better deal.

Loans and the lending environment are constantly changing. It is impossible to stay across the latest offerings and servicing calculators of all the different lenders, and the common belief that all of the banks assess your situation in the same way is not true. One lender may have an appetite to lend to you, where others don’t.

I can’t recommend enough the benefits of engaging a mortgage broker who is experienced in the investment market and understands the best loans. Obviously, they should have access to multiple servicing calculators and lenders, but optimal investment structures require specialised expertise, which may be different to that offered by a broker who is primarily experienced in obtaining lowrate loans for owner-occupiers. Make sure your finance broker has a wealth of experience in investment, and be wary if their recommendations to you are focused purely on the interest rate, or bundling everything together with the one bank for convenience.

Lending conditions are changing weekly, so be persistent. If one lender tells you refinancing is not possible, don’t assume you will be turned down across the board. There are many lenders in the marketplace, and your mortgage broker can help guide you through this process.

Everything cycles in the short term, from interest rates to lending criteria, inflation, wages, rents and property prices in any number of different markets

The worst-case scenario is that you don’t meet the lender’s servicing requirements and your loan is converted to principal and interest. In this case, my advice is to constantly review your borrowing capacity and understand the refinancing options available to you at any point in time. This extends to second- and third-tier lenders who have very favourable servicing calculators compared with the major lenders. Their rates are slightly higher, but the overall holding costs may still be more manageable than the principal and interest repayments, especially once the negative gearing benefits of investment lending are factored in. These lenders are an option to be considered.

As a safety net, it is prudent to have cash flow buffers in place. These may take the form of savings, equity loan facilities or a line of credit, which cover you if something changes during your investment journey.

This buffer will finance your investment if you experience a prolonged period without a tenant or need to cover the cost of unexpected expensive property maintenance. As I said earlier, the most common reason investors rely on their buffer is because their property holding costs increase when the interest-only loan term ends. It is much easier to sleep soundly at night if you know you have the cash flow to cover your loan repayment obligations. I consider a buffer a non-negotiable when it comes to investment.

"Effective investment is about staying focused on what you can do right now

to improve your portfolio, and remaining committed to your long-term goal"

As your portfolio grows, a smart strategy is to stagger interestonly expiration dates across your loans. That way, regardless of the market you will be protected and not caught in an unmanageable situation with multiple loans potentially shifting to principal and interest repayments at once, if refinancing is not possible. The larger your portfolio, the more sensible this suggestion becomes.

As an investor with multiple properties myself, I am always trying to maximise my interestonly repayment time frame, while maintain a competitive interest rate and my preferred variety of lenders across my portfolio. Hopefully these tips will help you to do the same, and remember: stay focused on the long term.

Michael Beresford is director – investment services at OpenCorp

Michael Beresford is director – investment services at OpenCorp

and has successfully guided over a thousand Australians in amassing

more than $500m in property wealth.