With ongoing regulatory changes impacting how lenders have assessed borrowers over the last few years, there’s been another issue bubbling away beneath the surface, which many people haven’t factored in: the impact on borrowers’ privacy.

Paying by card has become the norm. Online shopping and hand-held apps that can get us places and serve us meals at the tap of a screen have taken us to the point where few of us spend with cash.

However, such transparent account activity in a tightened lending climate begs the question: is the make-up of your monthly bank statement impacting your chances of being approved for a home loan?

“We are living in more of a cashless society, and I am no different to anyone else. I just tap my card because it’s easy; it’s convenient,” says Tracey Sofra, partner and financial planner at Sofcorp. “But the pure fact is that now [lenders] have verification of how you are spending, without a doubt.”

Lenders have been digging a lot deeper in terms of asking questions – but according to Philippe Brach, CEO of Multifocus Properties and Finance, the pendulum has “gone from one extreme to the other”.

“Lenders have actually pushed the envelope too far in my mind because we are now in a situation where even discretionary expenses are being taken into account,” Brach says.

“They even take investment property expenses as part of your living expenses, so if you have a large portfolio of properties, suddenly instead of [having] living expenses of $5,000 a month, you could end up with $15k a month – and that kills your borrowing capacity straight away.”

Furthermore, while previously only basic living expenses were considered, lenders did not pay as much attention to restaurant bills and holiday bookings.

That’s because these are discretionary items that you can pause spending on if money gets tight.

“You can squeeze them if you start feeling financially stressed, so they didn’t take them into account – but now they do,” says Brach.

“So, if someone saves diligently to go on a $30,000 trip around the world, and they spend that money on travel, suddenly that will impact their borrowing capacity massively, simply because they go on holidays.”

As banks begin to initiate ways in which they can regain consumer confidence while still adhering to borrowing regulations, Brach says eventually lending conditions will “go back to somewhere more reasonable, in the middle”.

How to put your best foot forward

Instead of tapping and charging every expense to fantastic plastic, you may be better served by withdrawing cash and transacting the old-fashioned way.

“Paying in cash is certainly a way of not having to report what you are doing. If it’s on your credit card, then everybody knows, but if you’re paying cash, then you increase your degree of privacy,” Brach says.

However, he also suggests that borrowers should put themselves in the shoes of a loan assessor for a moment.

“[When lenders] look at someone’s transaction account, all they can see with the ATM withdrawals is $500 here, $400 there. It will match these up because the borrower will still have to declare their expenses, so it will match how much has been taken out of the ATM with how much the person is declaring,” Brach explains.

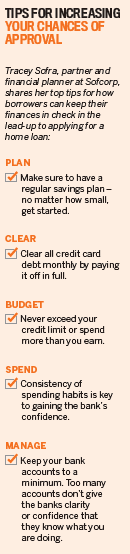

Sofra also reminds borrowers that they need to be mindful of their bottom line, whatever their spending habits may be.

“I’m not sure that the banks are interested in whether you are having a wine, or a gin and tonic, or buying 10 pairs of shoes. I just think it’s more about what’s coming in and what’s going out,” she says.

“I would be focused on the end goal: making sure that you are exhibiting good habits.”

A pattern at play

Full disclosure of where we choose to spend our money, how much we spend and how frequently reveals a lot about our overall financial behaviour. This includes how we manage money, how we perceive it, and in turn how we will potentially look after a loan when the time comes.

When a lender assesses your expenses, what they are looking for is how much a borrower earns and whether they are putting a portion of their income aside each pay cycle, Sofra explains.

“We are living in more of a cashless society … the pure fact is that now [lenders] have verification of how you are spending”

“As a lender, if they wanted to go that deep, they could see the income coming in and the expenses going out and ask the question: are their earnings justifying where they are eating? However, if at the same time they are seeing a direct debit going off to a savings account within the same bank, and that’s a pretty good percentage of the borrower’s overall income, then that signals a really good pattern,” she says.

Understanding cash flow is fundamental and will place a borrower in a strong position when they apply for a loan, Sofra adds.

The impact of credit cards

Having a credit card in your name and not having ever used it may show financial discipline, but simply having one open at all can potentially shave off a portion of your loan serviceability.

However, ideal management of credit cards depends on the borrower’s goals and whether they are already comfortable enough with their serviceability, Brach says.

“With your credit cards, if your borrowing capacity is $500k in order to buy a $700k house, then obviously you won’t get enough [financing], so you will need to start squeezing your liabilities and your expenses somewhere – and one of the things you can do is close the credit cards that you are not using,” he explains.

It provides peace of mind that in the case of life presenting an unexpected financial expense, there will be redraw available on an existing home loan. But from the point of view of a lender, Sofra asks, “If you did pull the money out, where does that leave you in terms of your ability to repay the new loan?”

It provides peace of mind that in the case of life presenting an unexpected financial expense, there will be redraw available on an existing home loan. But from the point of view of a lender, Sofra asks, “If you did pull the money out, where does that leave you in terms of your ability to repay the new loan?”

She explains how a client was required to close down their redraw option in order to get approval for a refinance from their new financier.

“The new financier said, ‘We will count that as money that you already have access to, which you can pull out at any time, so we are going to count that into the equation when assessing you for a refinance’,” Sofra says.

Being mindful of the loan features and credit access that you actually need is an important step, so it’s advisable to consult with an experienced and qualified finance broker.

“Debt is a beautiful thing, done well and done properly, so we should respect it in such a way that we can continue to borrow”

A return to normality?

When asked about the direction that access to lending is heading in, Brach says, “We always get back to something that’s reasonable, but we just have to go through that phase.”

The shift has already started to happen, he explains, with some lenders lowering their assessment rates.

“That automatically gives people more borrowing capacity,” he says.

Sofra adds, “Where there is a roadblock, there will be some evolution around that.”

Throughout her years of advising, she has seen reluctance from some borrowers when it comes to taking out a loan. But she encourages them to look through a different lens.

“Understand and know the income that is coming into your household, and be comfortable with the debt levels that you want to take on,” she says.

“Debt is a beautiful thing, done well and done properly, so we should respect it in such a way that we can continue to borrow, so that we can build wealth and live rich. Because debt is leverage to greater places.”