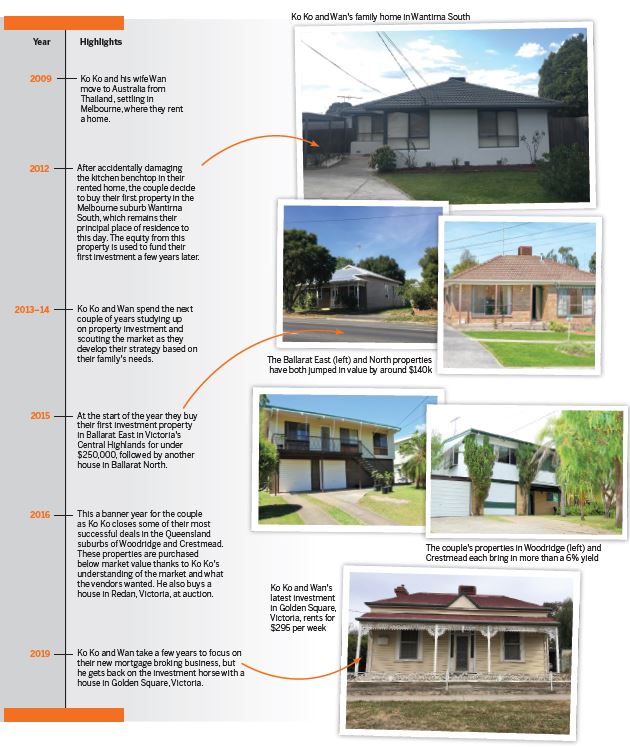

When Ko Ko Naing first migrated to Australia from Thailand with his wife Wan at the end of 2009, he wasn’t sold on the idea of property investment.

“With only $10,000 cash in our hands, I was very sensitive to debt – I was not a fan of any debt at all. Back then I had no idea about the difference between good and bad debt,” he says.

“But my wife kept on saying that if we bought a property, one day it would be ours.”

The couple decided to rent a home for a few months, during which time Ko Ko began to consider becoming an investor.

“We thought we would try to get into the property market without knowing anything about mortgages or property at all,” he says.

“We remember asking a mortgage broker how much we could borrow, and she asked us how much deposit we could contribute. After mentioning that we only had $6,000 in our savings, she told us that we’d better save more to be able to buy even a very small one-bedroom unit.”

We had only one income stream, so we didn’t want to be negatively geared on our first purchase and get stuck with only one property in our portfolio

Ko Ko and Wan took the broker’s advice to heart and continued as tenants until the end of 2012, when an unexpected kitchen incident at their rented home spurred them to take the big step.

“The trigger point happened in October 2012 when my wife accidentally placed a hot pan on the kitchen benchtop, leaving a very pale burn mark. We went back and forth with the property manager and the landlord with regard to compensation and insurance,” Ko Ko says.

“We got quotes from multiple tradespeople to repair the damage, and it was quite a hassle for us both mentally and physically. The case was closed by paying $900 to the landlord as compensation.”

The experience, he says, “triggered my inner motive” to get off the rental ladder and become a property owner. It finally convinced him that he and his wife needed to buy their own home, so within just two months the couple purchased their first property in the Melbourne suburb of Wantirna South.

AT A GLANCE

Years investing as a couple: 5

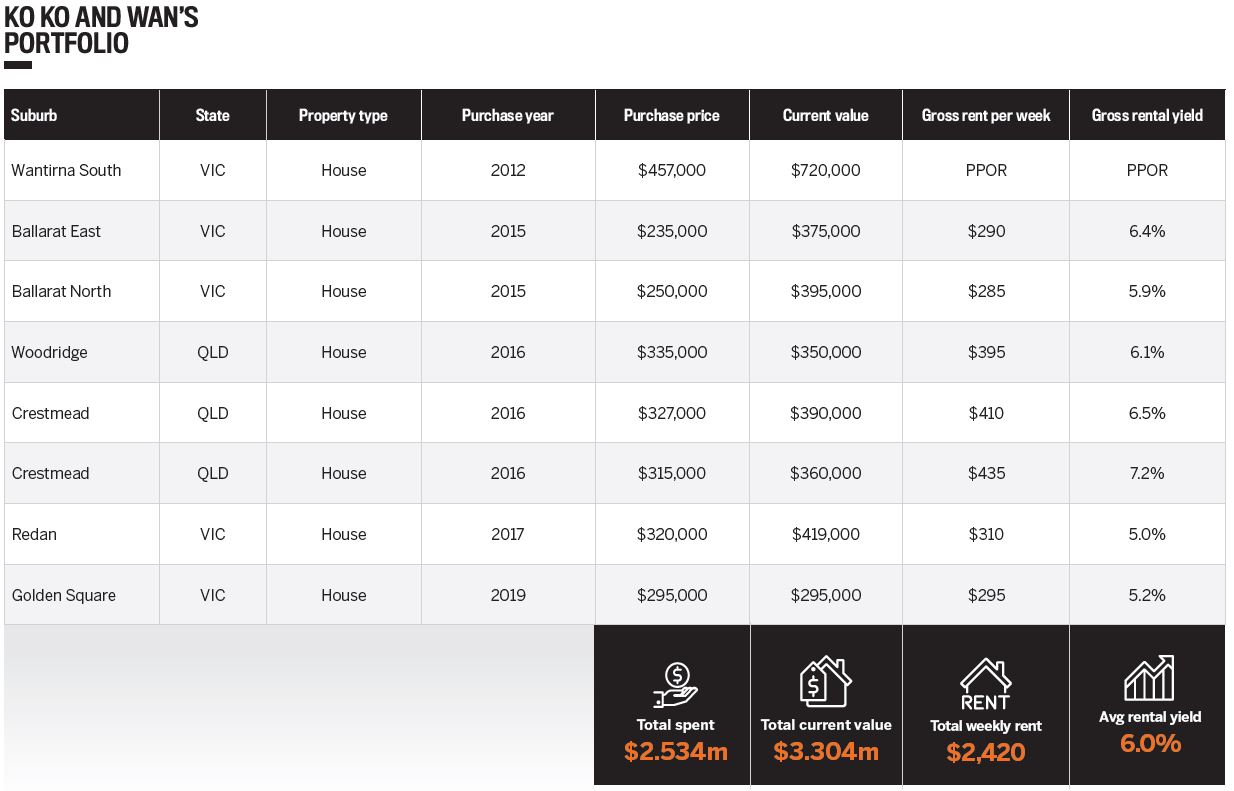

Current number of properties: 8

Current portfolio value: $3.3m

DIY due diligence

Their first buy opened up the floodgates, so to speak. No longer content with just having their own home, Ko Ko and his wife began educating themselves on how to build a property portfolio by frequenting online forums, as well as reading books and magazines on the subject.

“We didn’t know which area to invest in, what to watch out for and how to identify an investment-grade property. We didn’t go to any property seminar or have anyone to guide us, so we did a lot of due diligence ourselves.”

With Ko Ko being the sole breadwinner in the family, it was imperative that their investment made money from day one. This meant looking beyond a capital city for a positively geared property.

"At the time, we had only one income stream, as my wife was a stay-at-home mum looking after our younger son. We didn’t want to be negatively geared on our first purchase and get stuck with only one property in our portfolio. Also, we’d always wanted to invest in fully detached houses with a decent land component, so Melbourne was out of the question.”

After two years of preparation, and with the equity from their home in hand, the couple bought their first investment property in Ballarat at the beginning of 2015.

“It was a 100-year-old period home in Ballarat East, located very close to the city centre. To be honest, at the time we didn’t know what a period home was. But people in Ballarat love and value period homes, as builders don’t build them any more,” he says.

To date, this investment has paid off in spades for the couple, recording considerable capital growth over the last five years, while generating a significant rental yield. Ko Ko’s careful personal research also led him to make what he considers his most successful investment, in 2016.

“Knowing the market well and understanding the zoning of the area helped me a lot with closing the deal on our Woodridge property successfully. The agent was from another area and didn’t know the property was in the townhouse precinct. Properties in those zones were selling for much higher prices than the ones that were not, because a lot of investors were looking for development potential in the Logan area,” he explains.

PORTFOLIO TIMELINE

“The land, which can easily fit at least three three-bedroom townhouses or four two-bedroom townhouses, according to the guidelines provided by the council, was sold to us for $335,000, while properties in the townhouse zone sold for $50,000 more.”

Over the years, Ko Ko has focused on properties that generate great cash flow, while having strong growth prospects and add-value potential. He also aims to buy below market value as much as possible so he can “make money on the way in [buying], rather than on the way out [selling]”.

To this end, Ko Ko says that “knowing the motive behind the reason why the vendor is selling the property is the most successful strategy we have used”.

“Money is not always the most important thing. Depending on what the vendor is looking for, we found that some vendors are willing to accept a lower offer for a transaction with less hassle, such as an unconditional offer without any finance clause or building/pest clause,” he says.

Minimising risk continues to be a major factor for Ko Ko, so he avoids buying in areas known as being prone to damage from weather events.

“When we buy, we always check that the property is not in a bushfire or flood zone. While such properties might come at a cheaper price, potential buyers will ask for the same discount when the time comes to sell. It’s not worth it to pay higher insurance premiums for many years and take a risk of experiencing hassles while dealing with insurance companies.”

Beyond monetary gain

With eight properties under his belt currently valued at over $3m, Ko Ko is looking to expand into more avenues for adding value.

“As all of our properties are fully detached houses with large land components, we will be looking at subdividing and developing at some point. We will also look at optimising our portfolio to maximise its capacity,” he says.

Financial freedom continues to be part of Ko Ko’s main goal as an investor, but he’s looking to leave a more intangible legacy as he continues his journey.

“Our ultimate goal with investing is to have options when retirement time comes, and to be able to help others in need,” he says.

“Financial freedom is one goal that we would like to achieve for ourselves, but on the other hand, what’s the point if one is to come into the world and pass away without doing any good to the community? So eventually we will be looking at setting up a philanthropy foundation.”

“Knowing the motive behind the reason why the vendor is selling the property is the most successful strategy we have used”