John Pidgeon is known as “Pidge” on the footy field and he has had many proud moments there.

John Pidgeon is known as “Pidge” on the footy field and he has had many proud moments there.One example is winning the 2000 Premiership (in Victoria), playing centre for the Kalkee Football Club. But it’s actually outside the oval where he has been kicking goals in recent times.

These days, the 38-year-old spends his time as an AFL coach of the local Central Coast Bombers, as well as coaching property investors at Positive Real Estate.

John acknowledges that the countless days spent kicking footballs around with his teammates have helped shape him as an AFL coach, in the same way as the many hours he has devoted to his property investing portfolio have moulded him as a property investing coach.

“You earn respect having been in the trenches living and breathing it, but it also means you can give real-life examples to help others,” he says.

“However, coaching is all about solving problems and having a rapport with those who you are coaching. If you can’t do either of those two things, it doesn’t matter how much experience you have.”

John adds that the motivational skills required are also very similar for his dual passions.

“For both you have got to be focused and you have to have a goal at the end of it,” he says.

“You need to take action and believe that you can reach the goals that you set. Do not deviate from that, even when it gets hard.”

This never-say-die mindset has helped John accumulate a portfolio of five properties collectively worth $3.07m.

“I see property as a safe wealth creation tool, particularly compared to shares and other commodities,” he says.

“This is based on property’s performance, but also its lack of volatility.”

Starting small

For many investors, the greatest regret they have is not starting their property investing journey sooner.

Fortunately, John latched on to an opportunity at a young age.

While he was at the University of Ballarat studying for his degree in physical education, he was also learning much about the art of property investing and wealth creation strategies.

“I learned from reading books, listening to tapes and CDs, but not actually studying any course at uni that related to wealth creation,” he says.

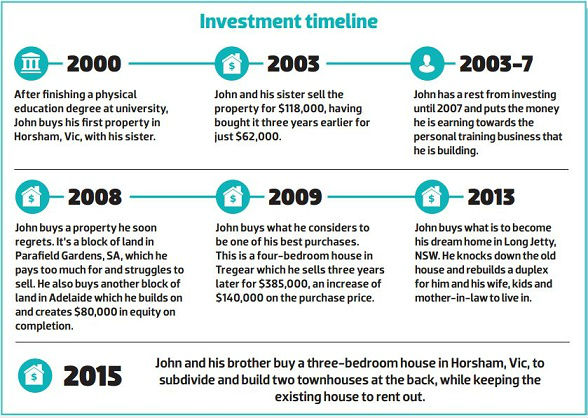

He bought his first property for $62,000 in 2000 when he was just 21 and straight out of university. It was a two-bedroom weatherboard house on a corner block in Horsham, Victoria. And like all keen investors looking for a means of getting into the market, he explored smart options to make it possible.

“I went into a joint venture with my sister, so we only needed roughly

$4,000 each,” he says. “We did a basic cosmetic reno, put up a carport and essentially cleaned up the property from the state it was in.”

Three years later, they sold it for $118,000. But despite this success, John acknowledges that he probably should have done more research before he decided to buy the property.

“It was achieving a good rental yield, and that was my main concern at the time,” he says.

“I always do interest-only loans, but holding costs are crucial for cash flow, and being the first investment this was the main thing I was concerned about.”

Following this purchase, John had a rest from property investing until 2007. During this time, the money he was making was going into growing his personal training business.

Where John has been buying lately

John’s success with his first property has helped enable him to buy and sell many more since then. He now owns five properties and has bought two in the past two years.

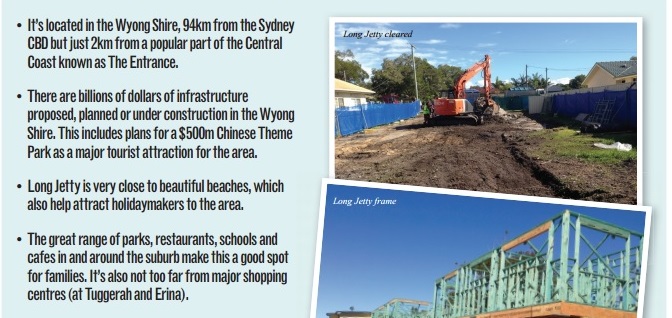

One of those properties is in the Central Coast suburb of Long Jetty, NSW, which he bought in 2013.

At the time he was looking for somewhere to live and was also looking for an old house on a block that he could knock down, subdivide and put a duplex on.

He decided to buy in Long Jetty after coming to the conclusion that the property was undervalued, based on the market value at the time.

“I had seen what other duplexes had sold for in the area, so I saw value straight away at the right price,” he says.

“The market has not moved much since 2006, so there was potential there. It’s also within walking distance of the beach.

I knew capital growth was to come, but we would also make money without capital growth. This was simply the icing on the cake.”

John bought the property for $1m and has since knocked it down and built a duplex. The result comprises a four-bedroom on one side and a three-bedroom on the other, with his family living in one and his mother-in-law in the other.

“Now there has been more than $600,000 created in equity in just two years,” he says.

Subdividing is something John has done twice, and he has found that it’s a fantastic way to add value to a property. However, he acknowledges that it can be a challenging experience for those who are unprepared for it.

“It can be difficult if you do not know your numbers and overestimate returns or underestimate costs,” he says.

“But if you have done your due diligence this can be minimised.”

He recommends that investors considering a subdivision should specialise in one or two suburbs and calculate the potential return based on a worst-case scenario.

“It’s better to be an expert in one area than to just be all right in all areas, unless other experts can fast-track that knowledge for you without you studying up on it.”

Buying with his brother

The other property that John has bought in the past 24 months is a three-bedroom house in Horsham, Victoria. He purchased this with his brother, who was looking to buy an investment property for the first time.

“He trusted me to do the numbers and negotiate the price to pay and the right block to do what we wanted,” he says.

“He wanted to get into property, and I wanted to help him out in a market that we both know well. He also lives out there so he can do hands-on renovation and work with the builders we know."

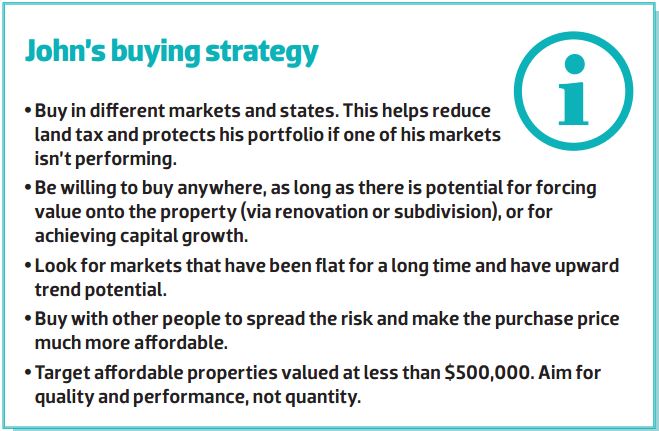

John is a big fan of joint ventures as they allow him to get into the property market using less money, which leaves more for him to put into other markets for diversification.

“Two of my purchases were to help my relatives get into property investing for the first time. It’s a really powerful and satisfying thing you can do for those close to you,” he adds.

John’s best deal

In 2009, John bought a property in Tregear, 46km west of the Sydney CBD. This was a four-bedroom house on 600sqm that he purchased for $245,000.

The property was ideal for renovation, a characteristic that he took advantage of. He painted the inside, added new steps, updated the bathroom and installed new window frames and blinds.

Despite the rise in growth he was seeing with this property, he ended up selling it in order to help pay for his principal place of residence at Long Jetty.

“I was told from an early age to not buy my own house to live in until I had cash for this,” he says.

“[By this I mean] no loan required as it is bad debt.

“I caved in with this when we had our third child, and sold the Tregear property at the height of the property market to pay down debt.”

He sold the property for $385,000 just three years after buying it, which was a whopping 57% increase on the purchase price.

“I attribute the growth to the small renovation, but the majority of it was identifying potential capital growth in the market, which had been flat for years,” he says.

“The rental yield was also already high, and growth usually follows yield.”

Looking back

While John doesn’t have many regrets about his property investing journey so far, he says he would have reconsidered buying a block of land at Parafield Gardens, SA, in 2008 if he could start all over again.

“I had intentions to build on that land, but I soon realised that I had paid too much and consequently didn’t build. It took me a while to sell that land,” he says.

“I lost about $30,000, but this was offset against a gain, so it probably ended up neutral in the end.

“However, the opportunity cost was evident.”

Additionally, John regrets not buying another property after his success in selling the house in Horsham. This was during the period from 2003 to 2007 when he was building the personal training business that he ran for 10 years.

“I definitely should have continued to buy,” he says.

“But a lot of my cash flow was going back into my business, so it was a bit harder at the time.”

Looking forward

In the short term, John plans to expand his portfolio further. He’s eyeing Brisbane at the moment because he believes this market has been flat for a long time and has a lot of upward trend potential.

“I am looking just north of the Brisbane CBD and I also see some value in Ipswich as well,” he says.

“I like Kedron and Chermside for housing, as well as Woolloongabba for apartments.”

While John’s investment portfolio is growing strongly, he says he’s not about to quit his day job any time soon.

“I love what I do, so I am not looking at an early retirement,” he says.

“For me it’s not about reaching a certain number of properties. It’s more about the quality of them and the performance of them.”

“What motivates me is to spend time with family, provide financially for my family and to help educate those closest to me,” he says.

“I believe that everyone wants a better lifestyle but they just don’t know a way out!”