Promoted by loans.com.au

Growing your retirement savings today matters if you want your sunset years to be comfortable. The most recent Retirement Standard (June quarter 2025) of the Association of Superannuation Funds of Australia (ASFA) puts a "comfortable" annual budget at $53,289 for singles and $75,319 for couples aged 65-84.

To support that lifestyle (assuming home ownership and a part Age Pension), ASFA estimates super balances of $595,000 for singles and $690,000 for couples at retirement.

Many Australians are eyeing self-managed super funds or SMSFs to achieve that level and grow their retirement funds. SMSFs offer control over the investments; they can hold a wide range of assets, including direct property, which is part of the appeal.

But with control comes responsibility: trustees must run the fund to super law standards year in, year out. So whether you choose this route or grow your nest egg in an industry super fund depends on a few things.

SMSF vs Industry Super Fund: A quick look

An SMSF swaps convenience for control - you call the shots (and carry the compliance). Meanwhile, an industry fund delivers diversification and governance with less admin.

Generally, the right choice depends on your balance, appetite for paperwork, liquidity needs, and whether you genuinely need SMSF-only strategies like business real property (BRP). If in doubt, you should speak with your financial advisor.

Who is in charge?

With an SMSF, you are the trustee and must maintain a written investment strategy that considers diversification, risk, liquidity and insurance, and you must review it regularly. You cannot skirt around this, as auditors check this.

On the other hand, industry funds are run by licensed trustees under APRA prudential standards (investment governance, valuation, liquidity risk, unit pricing). The fund, not you, must evidence prudent practices and is subject to APRA's annual performance test regime and heatmaps.

What can you own?

SMSFs can hold a range of assets (including direct property). However, if you hold property, you need to be mindful of the rules that apply to SMSFs. For instance, while business real property can be leased to a related party if strictly on arm's length terms, there are tight restrictions for residential property and in-house assets.

Industry funds give you unitised exposure, which may include unlisted property, but you don't directly own or gear a single asset.

What do you need to report?

SMSFs must report market values for all assets each year and keep objective, supportable evidence (especially for property). Independent valuers are not mandatory every year, but you must be able to substantiate the figures each year, especially for property.

Growing retirement savings through SMSF

With an SMSF, you may grow your nest egg by owning property - pocketing rent and any long-term gains. Think of an SMSF as a way to put a rental property to work inside superannuation tax settings. In the accumulation phase, the fund's investment earnings (including rent) are generally taxed at 15%.

Fast-forward to retirement (pension) phase, and the tax picture may get even better: the income and gains from assets that actually support your retirement-phase pension can be tax-exempt under ECPI, provided you meet the minimum pension rules and keep your paperwork and valuations up to scratch.

One of our customers, Gold Coast-based public servant Jack, understood the benefits of growing his retirement savings by investing in a property through an SMSF.

"I personally believe that investing in a property through my SMSF will deliver better returns than putting the money into a typical retirement or industry super fund," Jack shared.

"I wanted to buy a property through my SMSF and, initially, I was navigating that process with the mortgage broker who had helped us with our home."

During this process, Jack decided to do his due diligence to ensure the product being recommended to him "was absolutely the best product out there".

"I was on the computer late one evening and I came across loans.com.au with their very-low interest rate and, once I worked out the figures and annualised it, that was way better than what the broker had recommended," Jack said.

Once he was set on taking out an SMSF loan through us, the next challenge for Jack was finding an investment property that could be used as security for the loan.

"The staff have been absolutely amazing. They made it a very seamless process," he added.

"At first, it was a bit of a daunting task because I felt like I was doing it on my own. But after I went to loans.com.au, I felt like my lending specialist was holding my hand with the process throughout."

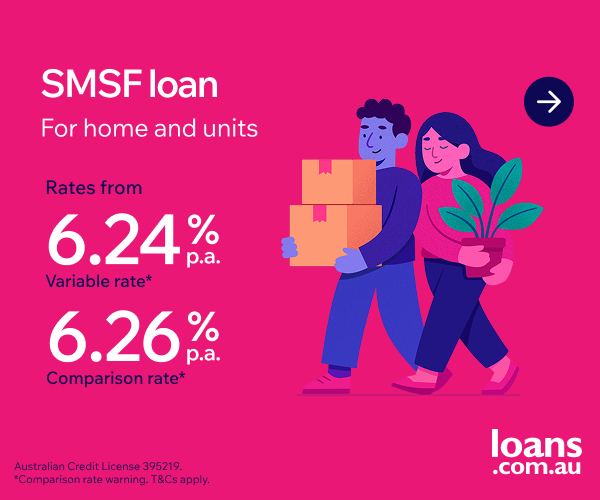

*Rates as at 22 October 2025 for SMSF Residential Loan

Investing in property through your SMSF

A headline draw of an SMSF is the control over a tangible asset and the option to use a limited recourse borrowing arrangement (LRBA). This means that if you borrow money to fund the asset acquisition, the loan is secured only by the asset acquired, and other fund assets are protected in case of default. You will likely need a guarantor for the loan, however.

Some business owners value the ability to hold business real property (BRP) in the SMSF and lease it to a related party on arm's-length terms.

Take the case of one of our customers.

Paul's wife Kylie had been renting a space for her Pilates studio in North Adelaide for over a decade. When a commercial unit became available within the same complex, they saw a golden opportunity to secure a permanent home for the business.

After consulting with their financial adviser, they decided to set up an SMSF and purchase the property through it.

Paul and Kylie's financial adviser recommended us for our specialised SMSF Commercial Loan options, which aren't readily available elsewhere. And their application was completed online, with our system guiding them every step of the way, offering transparency, seamless communication, and quick document processing.

"The whole process was seamless from start to finish," Paul related.

"This was our first time doing a loan entirely online, and while I initially had some doubts, the platform was incredibly clear and easy to use.

"Communication was spot-on, and the documentation team was exceptionally prompt - documents were checked and approved within a day, which is a big contrast to other experiences we've had."

With the funds they got through loans.com.au, Paul and Kylie were able to buy the property they were eyeing, and Kylie is now operating out of a beautifully renovated, street-facing studio with better visibility and increased foot traffic.

"It's been a game changer for both our business and our financial future," Paul said.

Ready to take the next step like Jack, Paul and Kylie? If an SMSF property strategy fits your goals, explore our SMSF loan options. Both our SMSF Residential Loan and SMSF Commercial Loan come with competitive rates and options to borrow up to 70% LVR. Book your free consultation and see how SMSF loan options could work for your fund.

Header image by Vitaly Gariev on Unsplash