Expert Advice with Cam McLellan 27/05/2016

Why Property for Me?

... Land.

The British royal family is a perfect example. They have amassed huge wealth, simply because they owned all the land and collected rent from everyone who lived on that land.

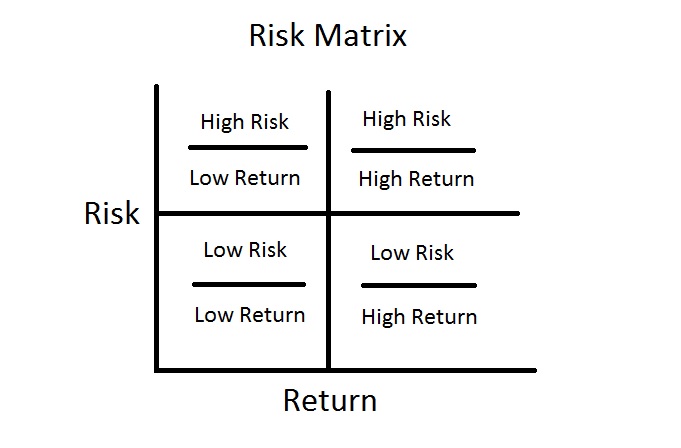

Now, smart investors know that if you want to assess an investment opportunity, you must consider a Risk v Return ratio.

Unfortunately, most investment opportunities fall into the ‘low risk/low return’ or ‘high risk/high return’ quadrants. This doesn’t mean they shouldn’t be considered. It just means that you need to do your research to try to understand the risks so that you can manage them. In other words, you need to maintain control and compensate for the risk.

I want to discuss a few of the basic must-knows to building a portfolio and why history was important to me when choosing property as my wealth-building vehicle.

Let’s talk about market history. The reason you look at each market (city) first is because that’s the way sophisticated or smart investors pick good investments. You firstly assess each market, you then choose the appropriate area within a market and finally you look at the actual property itself.

Market – Area – Property

Firstly pick the city market which has the best potential for growth.

Then determine the best area within this market that will provide a good balance of yield and growth.

Finally, select the optimum size and quality investment property for that area.

This is a very important process to remember when investing.

Now, you will often hear people telling stories about what some lucky person they know paid for a house 20, 30 or 50 years ago. Why then can’t these people give you a calculated estimate on what a house will be worth in even 20 or 30 years’ time from now?

Let’s take a quick history lesson. History is the first thing we look at when looking at any market. Don’t worry, we don’t play the market by trading, but it’s good to understand what drives a market. The two long term drivers are population growth and housing affordability.

Quick tip

“What’s the median house price?” The median value is the middle price in a series of sales. For example, if nine sales are recorded in an area and arranged in order from lowest to highest value, the fifth sale price is the median price. Don’t get confused with the average sale price (mean or medium), the median house price is not the same as the mean or medium house price. This is a common mistake people make.

“Where can I find these types of charts?” The Australian Bureau of Statistics website is a good start (www.abs.gov.au). It’s not a fun site to navigate but there is lots to find. Also take note of other stats and charts that you come across. Most will have reference points.

Forty years I feel is a good length of time to study data. When looking at this amount of time, you’re able to focus on a number of decades, which gives you an understanding of average growth over time. It also enables you to focus on yearly spikes and dips and then consider what caused these movements.

Also you will notice that when you think back to major economic events you can see how the markets at times do get knocked around. Look at what happened after the 1987 stock market crash. People pulled their money from shares and invested in property and prices went up. Then came the recession of the early 90s, with interest rates at 17%. The high prices took a dive until the economy resettled and everyone realised that a recession didn’t mean the world was going to end.

Now let me ask you a question whilst taking this information into consideration. If you purchased a property in 1989, would you have been unhappy with your purchase in 1992? Over that period, in most cities you would have to answer, yes, you would be disappointed. But remember that the key to building wealth is to buy as soon as you can afford it and hold for growth over the long term. Now I’ll ask a slightly different question. If you purchased a property in 1989 and held that property until today, would you be unhappy with your purchase considering the current price value? Of course not. You’d be stoked. That’s why checking all the graphs and stats in the world doesn’t really matter if you stick to the basic purchasing criteria.

Can you imagine in 50 years the price of a standard house being worth $40m? I’m sure 50 years ago people who purchased a house at $14k could never imagine a house being worth half a million dollars today, but that’s the reality. Even 30 years ago, being a millionaire was a very impressive feat. It seemed that only people like Alan Bond and Kerry Packer were millionaires. These days, being a millionaire is really not that impressive at all. That’s the effect of the ever-decreasing value of cash in the economy.

Remember, past history is never a guarantee of future performance. Continually do your homework on each city market and then the areas within that market. This will maximise your success and reduce the risk of investing your money in an underperforming asset.

Now let’s look at a few other factors that help us to determine future growth.

It’s useful to understand some of the broader factors that provide the foundation for appreciation over the long term. Some of the key points are summarised below:

- The Australian population is growing faster than ever

- With rental vacancy rates in the capital cities at a low, demand for rental property remains exceptionally strong.

- Australia has one of the world’s best performing economies, we are now earning more than ever before.

When sourcing information it is always good to be discerning. Think about the source of the information. Who gathered it, what is their underlying agenda.

My Top Tips

- Over 90% of the world’s millionaires made their first million from property.

- Investing in growth property is like a bad haircut; time fixes everything.

- Realising capital appreciation on your properties is the foundation to wealth building.

- Remember, to maximise your investment’s growth potential, you firstly need to determine:

- The city market most likely to increase in value.

- Then, the area or suburb within this city.

- Finally, we look at the investment property that best suits that area.

...............................................................................................

Director of OpenCorp, Cam McLellan is committed to sharing his passion and property investment knowledge with everyday Australians.

Director of OpenCorp, Cam McLellan is committed to sharing his passion and property investment knowledge with everyday Australians.

After thriving in the telecommunications, technology and recruitment sectors and making six BRW Lists in 8 years, alongside accomplished OpenCorp. entrepreneurs Matthew Lewison and Allister Lewison, founded OpenCorp eight years ago. Cam started investing in real estate at a young age and quickly mastered the art of building sustainable wealth. He has used the same wealth building strategy to develop a multi-million dollar business, sharing his knowledge and skill with ordinary Australians. Cam has personally bought, sold and developed numerous properties and has an extensive residential and commercial investment portfolio.

Read more Expert Advice from Cam here!

Disclaimer: while due care is taken, the viewpoints expressed by contributors do not necessarily reflect the opinions of Your Investment Property.