As the cycle moves on to the next level, so has sentiment, and predictably forecasts of doom and gloom in the market have started to gather pace. So what’s really happening in the property markets and should you be worried?

If there’s one thing constant about the Australian property markets, that’s the obsessiveness of pundits who freely share their views about its impending doom. They declare the bust is just around the corner and it will be bigger and more catastrophic this time. They would cite bits of data to support their claim, scaring people in the process.

The latest one doing the rounds is that the Australian housing bubble is already here, thanks to the Reserve Bank’s continuing low interest rate stance. Former property market cheerleader Chris Joye argues that housing is currently overvalued by around 19% as property prices surge past income growth. In addition, he opines that the banks’ race to gain market share by offering lower interest rate mortgages is further fuelling the ‘nascent housing bubble’ that will inevitably get bigger.

So, is there truth to these dire warnings and what are the potential risks property investors should be aware of and prepare themselves for in the near to medium term?

Current state of the market

There’s no denying the strength of the broader property markets in Australia. Since the market bottom in June 2012, median dwelling price surged to a cumulative 17.4% according to the latest RP Data Rismark Index. Sydney led the outperformers with a staggering 25% total growth during the same period. Darwin came second with an equally impressive 20.4% growth while Melbourne gained 18.5%. Adelaide recorded the lowest growth of all capital cities at a meagre 5.5%.

But while the markets are still rising at the moment, the rate of growth has slowed according to the RP Data figures. Over the six months to July, capital city dwellings rose by just 3.7%, almost half the 7.2% growth the market recorded over the six months ending November when the market was at its strongest.

Year on year, Sydney recorded a total return of 19.5% while Melbourne racked up 14.9%. Brisbane gained 12% and Darwin notched up 13.2% total return.

Tim Lawless, RP Data’s research director, explains that the easing growth rate is further evidenced by the slower growth in mortgage demand thanks to worsening affordability and low rental returns.

What does it mean for investors?

While it may be a bit discomforting to see price growth moderate, it’s actually a good thing, according to AMP chief economist Shane Oliver.

That’s because it reduces the risk of the Reserve Bank hiking rates too quickly and killing off the property market recovery.

“We’re 18 months into recovery and we’re still in the upswing,” Oliver says. “Interestingly, during the first half of this year, property prices have actually cooled a bit and slowed to around 6% annualised pace. It’s still going up but going up at a more moderate pace which I think makes the RBA quite happy. I was more worried last year that prices would take off too quickly and we could head to another bubble and the RBA would then jump in and kill it off. That worry I think is fading as the momentum in the property market has slowed down. It’s telling me property price growth is not out of control.”

What this means is that investors could at least relax in the knowledge that there is still enough heat in the market to fuel further growth in the near to medium term, albeit slower, as the RBA keeps the 60-year low interest rate.

“Sydney and Brisbane still have some heat and momentum to keep going whereas Brisbane is where momentum is starting to pick up,” says Angie Zigomanis, research analyst with BIS Shrapnel. “We think growth will be fairly strong over the next 12 months.

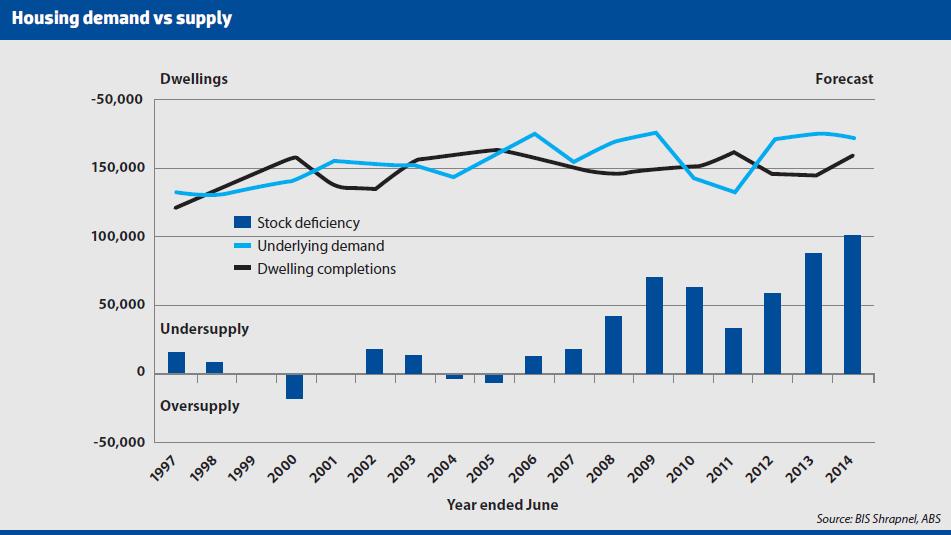

Housing Demand vs. Supply (Click to enlarge)

Over the next three years, Zigomanis is expecting Melbourne to grow by a total of 8% and progressively slowing, while Sydney is expected to grow by 10% during the same period.

What’s different in this cycle?

Unlike the previous recovery, this cycle hasn’t seen the same degree of follow through that some experts had forecast or feared according to Oliver.

“Compared to the 1990s this kind of low interest rate environment would have attracted more money,” says Oliver. “In the previous cycle, home buyers were more worried about missing out and were more confident in taking on debt in the belief that prices will keep going up and debt will be serviceable. In this cycle, that confidence is weaker. Borrowers are less inclined to take on debt.”

Another distinct difference according to Oliver is that a decade ago, housing as weighted credit was growing at 24% per annum whereas now it’s growing at just around 6%.

“The market has changed a bit,” he says. “People are reluctant to extrapolate the current growth into the future and are not inclined to pile on debt. So it’s not surprising that the momentum has slowed this year. But the result is a healthier market and extended growth cycle that we probably had.”

How about the current building construction boom?

Alongside property price growth, building construction has also staged a strong rebound thanks to low interest rates.

“The sector has responded better than we expected to low interest rates. And so we are now forecasting a record peak this year of 190,000 dwelling commencements which will be an all-time record that will surpass the previous peak of around 187,000 recorded in the 1994 boom, according to Kim Hawtrey, associate director with BIS Shrapnel.

This surge in construction is making investors nervous and worried that this will create an oversupply of dwellings that could dampen, or worse, crash property prices.

Oliver says this is highly unlikely.

“We’re building more houses this year but this follows years of underbuilding so there’s a massive undersupply to catch up on. We’re getting back to underlying demand but we still have the shortfall built up over the years to fill," he says.

The main constraint according to Oliver is the availability of land and the slow development process. “If you compare land development in Australia to the US, in the US, land development is fast and cheap whereas Australian cities still have regulations in them which slow the supply of land. That’s the biggest problem. We concentrate in the five major cities and then we put onerous restrictions on what goes in those cities. The cost of that is high property prices. By not supplying enough dwellings to meet demographic demand, we end up with price to income ratio which is high by global standards.”

BIS Shrapnel estimates the national dwelling stock deficiency is currently around 100,000 dwellings.

“Home building has been punching below its weight for about a decade, and has not kept pace with population growth for some time now,” says Hawtrey. “Australia’s rapid population growth of 1.7% per annum, which is among the fastest in the developed world, is translating into strong demand for new dwellings. As such we estimate that it will take the next five years to eliminate the unmet demand for housing. We therefore do not see this housing shortfall closing until 2018.”

This remains true despite expected national population growth slowing from its recent highs to just 1.18% by 2017/18 as net overseas migration falls back from its peak.

“Pent-up demand from recent strong population growth – coupled with the lowest interest rates in 50 years – is generating a record-breaking home building outlook for 2014/15 that will maintain its momentum into 2015/16,” says Hawtrey.

This means over the next two years, there’s still scope for a healthy price growth based on unmet supply.

“We expect prices to keep rising a little bit more because there is still unmet demand, but gradually over the next three to four years, the rate of price growth will ease. And that would be because interest rates have risen by that time and the extra supply that would have come through by then will be starting to meet the demand,” says Hawtrey.

Mortgage Rates and RBA's cash rate (Click to Enlarge)

Looking ahead, Hawtrey expects growth will resume again in the 2018/19 financial year - five years awsy from now.

"The pent-up demand will be satisfied by 2017/18 and the market will be more or less balanced. But then with continued population growth, demand pressures will again resume in 2019. And in 2020 we will again have a build-up of demand and will see basically a repeat of the kind of cycle that we have been seeing for the past 12 months,” he says.

Outlook for interest rate

Those who are worried about rapid rate rises soon can rest easy for now according to our experts.

“We’re still in a world of relatively constrained growth even though the economy has picked up, so the interest rate doesn’t need to rise. We don’t think interest rates will move in the next 12 months. It will stay the same until early 2016 when the fixes in the economy start to take effect. That's when we might see rate rises,” says Zigomanis.

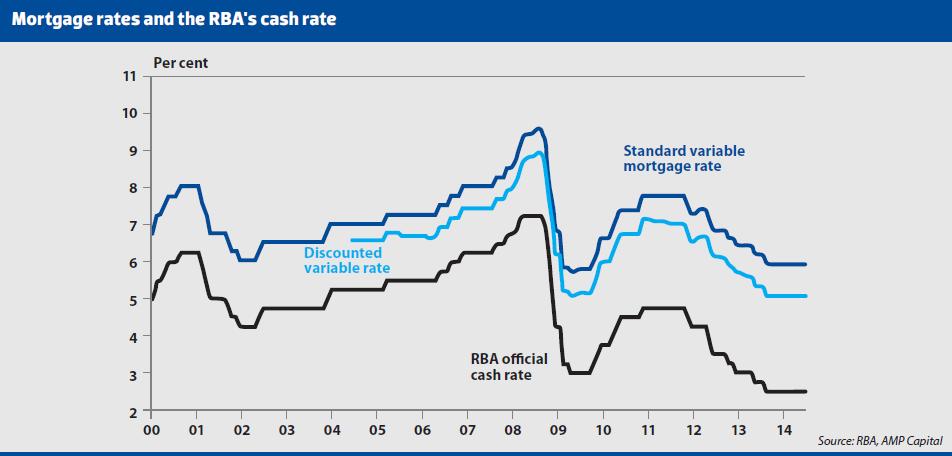

Another piece of good news: Oliver expects interest rates to peak at a lower level compared to the previous tightening cycle when the mortgage rate surged close to 9% in 2008.

“This cycle, the peak would see the cash rate peaking at around 4–4.5% which is about 6.5% mortgage rate,” he says. “Assuming the cash rate will go from 2.5% to 4%, the mortgage rate will be 6.5%, which is down a little down from the peak of 7.15% in 2010."

Cause for concern

While our experts are generally upbeat about the prospect of the market, they have a few concerns including:

1. Inability to rebalance the economy from mining to broader growth

Oliver explains that at the height of the mining investment boom, the resources sector was accounting for 1–1.5% of the GDP. Now that it’s going in reverse, it’s knocking 1–1.5% from the GDP growth.

While the economy is currently holding up, the main risk is if mining investment slows too fast and there’s something that will stall growth outside the mining sector, according to Oliver.

“The big question is whether the mining sector investment has slowed faster than desired or whether the investment has slowed faster than desired or whether the rest of the economy picks up less than necessary to fill the gap,” he says.

2. Price growth to be constrained over the next decade Perhaps a more worrying prognosis is for property price growth to remain subdued for an extended period of time as affordability takes its toll.

“What I think is going to happen is that we spend the next decade with constrained price growth as income catches up and the overvaluation will be worked off over time,” says Oliver.

This feature is from the October issue of Your Investment Property Magazine. Download the issue to read more!