Buy an older home, give it a refresh, and sell it for a whopping profit. Sounds simple, right?

Buy an older home, give it a refresh, and sell it for a whopping profit. Sounds simple, right?

In theory, this is how the reno and flip strategy works – and it can be very profitable for those who know what they’re doing, says Charyn Youngson, renovation specialist at Houses to Impress in Adelaide.

“Renovating for profit is simple, but it’s not easy. The basic principle is to buy something that’s under market value, cosmetically change it to make it more appealing, and then sell it for a higher price.

“To be successful, you need to buy at the right price in the right location, making sure all your figures stack up. Then you need to complete in a very quick timeframe to ensure your holding costs don’t eat into your profits.”

Youngson completed her first reno and flip in 2005, achieving a profit of $30,000. At the time, that was more than her annual wage as an administration assistant, so she began exploring the strategy further and eventually began managing renovation projects on behalf of other investors.

She believes the pros of a reno and flip strategy far outweigh the cons, but concedes that inexperienced renovators can make mistakes that eat through their potential profits.

“People tend to choose things that they personally like, instead of what the target market would be satisfied with. So instead of paying $65 on a kitchen flick mixer, they might spend $250 on one tap,” Youngson says. “It may not seem like a lot of extra money, but if you do that across every item, those things add up.”

The ultimate aim of your renovation should be to “take away any objections”, she adds, because people don’t want to buy a property that looks like a lot of work.

“The little faults in a bathroom, a green benchtop in a kitchen, peeling paintwork, chipped doors – people see these things and think they have to replace it and start again. But a number of small, strategic upgrades can make a home look brand new again, without having to gut the place and spend a fortune.”

What are the biggest risks?

A straight reno and flip project can be profitable. However, it is also “one of the riskier development strategies” an investor can undertake, according to Jo Chivers, property development project manager and owner of Property Bloom in the Hunter region of NSW.

It’s the high entry and exit prices that have the potential to eat through your profit and tank your project, she warns.

“The problem is, you’ve really got to get the property for a sum that is very much below market price to make it work,” she says.

Keeping control of your costs is one of the biggest challenges for renovators, particularly due to the inherent ‘unknowns’ involved in transforming an older house.

In many instances, you don’t know what you’re going to be dealing with until you start “ripping up tiles and pulling things out”, Chivers warns – and those hidden repair bills can stretch into the thousands of dollars.

“For instance, if the property needs a bathroom renovation, you might discover that the original bathroom has never been wet-proofed, so you’re going to need to pull everything out to be waterproofed,” Chivers says.

“Bathroom and kitchens are what you need to focus on most, and cheap kitchen renovations can be really noticeable. So, if you want people to pay a premium price for the completed property, then you have to take into consideration that they tend to expect a new kitchen and new bathroom of a certain quality.”

Going over budget is one risk, but it’s not the only one. The other risks of embracing a reno and flip strategy include:

Failure to complete the property

Some renovators underestimate the project and then run out of steam, so they place a half renovated property back on the market. “If you renovate one part of the house and not the other part, then the rest of the house looks shabby and unfinished,” Chivers says.

Minimise this risk by: Ensuring you budget the time, money and resources to complete the property. “Make sure you paint the entire house at a minimum, and install new floor coverings throughout,” she advises.

Overcapitalising

“It’s really important to not overcapitalise, which is really easy to do once you’re in the middle of the project,” Chivers warns. “You need to look at your figures carefully and buy the property at a discount, to ensure you can make a profit at the back end.”

Minimise this risk by: Creating a strict renovation plan and budget – and then sticking to it. Also, work your numbers backwards – ie start with your projected (realistic) sale price, then subtract your profit and expenses. The figure remaining is the maximum you should pay for the original property.

Not researching the market

Many investors dive into a renovation project without researching the market properly to ensure that there is actually “demand for the quality and level of finish” they’re installing, Chivers says. There’s no point in creating an executive residence suitable for cashed-up professionals if the local market is typified by young families and students.

Minimise this risk by: Researching the market thoroughly, asking local agents what types of properties are in demand and at what price points. This would greatly reduce your risks.

“It takes rigorous due diligence and observing the location closely to get this right,” Chivers adds.

Undervaluing your own time

Consider: Would you be able to earn more money doing something else? “You must take that into consideration because you’ll need to be on site doing as much work as possible to maximise your profits, only hiring in the tradies in areas where you can’t do it yourself,” Chivers says.

Minimise this risk by: Valuing your contribution to the project. “You’ve got to put a cost on your own time and labour,” Chivers says.

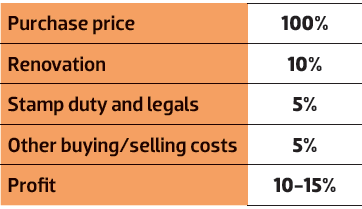

After weighing up the risks, those who are still interested in this type of investment strategy can use a basic formula to help them easily identify potential projects.

“The formula I use is to multiply the purchase price by 135%, as it allows you

to rule in or rule out a property really quickly,” Youngson says.

“If the figure you get is an achievable sale price for a renovated property in the neighbourhood, then you may be able to make it profitable. It’s not fail-safe, but this gives you a framework to guide you.”

The 135% figure is comprised of:

How to ensure a profitable reno and flip

1. Research the end sale price

“You need to discuss this with agents well before you sign on the dotted line,” Youngson says. “Don’t just rely on the figure that you think it would sell for; look at comparable sales for already renovated properties, and ask a few agents, so you’re not just relying on one avenue of information.”

2. Target the low end of the market

You can make more money and there’s less risk involved in lower-priced property, Youngson says. “If you buy a $1m house, you’ve got to spend a lot on the renovation, and achieving your target profit is a lot riskier,” she says. “At the low end of the market, your target buyer is less fussy, so you don’t need to put in Smeg ovens and fancy granite benchtops to satisfy the market.”

3. Budget your renovation strategically

You need to make sure your renovation costs no more than 10% of the purchase price, Youngson says. “If the property costs $300,000, don’t spend a dollar more than $30k,” she advises.

4. Allow 5% of the purchase price for stamp duty and legals

You’ll also need to account for a range of other costs that may include lenders mortgage insurance, building and pest inspections, mortgage interest, agent commission and other costs of buying and selling.

5. Factor in the holding costs

Mortgage interest, electricity, council rates and water rates will be payable during your renovation, and none of these expenses will be offset by any rental income. “Interest rates are low at the moment, which is helpful,” Youngson says.

6. Aim for a 10-20% profit after all costs

Youngson usually aims for a minimum of 12%, but considers over 10% a win.

7. Negotiate for access prior to settlement

“It’s not easy to negotiate this with the vendor, but if you do get it, it allows you to start renovations immediately so you can put the property on the market straight away and cut down on holding costs,” Youngson says. “You have to be 100% sure your finance is solid, because if the deal falls over for any reason, the vendor gets to keep the renovations.”

Which market works best?

A reno and flip strategy can work with a range of property types and in any market, whether it’s slow or fast, says Youngson.

“If you sell the property within a short period of time and you don’t overcapitalise, you can make money – and you can do that in a slow or a growing market,” she says.

“When I first started in renovating with my first flip back in 2005, it was a slow market. The thing to remember is that you can have micro climates and different dynamics within a suburb, with some areas that are doing better than others. So you need to really do your research because you make your money when you buy, not when you sell.”

She recently project managed a reno and flip for an investor client, who wished to gain a fast profit from a quick-turnaround property.

“We purchased the property for $250,000 and spent about $20,000 on the renovation, so it was a little less than 10%,” she explains.

“We put in a brand-new kitchen, a new laundry, repainted throughout, and styled it with rented furniture for the photos and inspection.”

Once listed, the two-bedroom apartment promptly sold for $330,000. After all of the fees and expenses were accounted for, including stamp duty, holding costs and real estate agent commission, the investor cleared a profit of approximately $20,000.

“It may not seem like a huge amount of money, but you have to remember that he did not do a thing, apart from signing the contract and supplying the funds. We completed the whole renovation within three weeks on his behalf, and he honestly made a profit without having to lift a finger, so it

can be quite a hands-off approach.”

How to make reno and flip strategy work

While Youngson is an advocate for this strategy and believes it can help investors make money in any market, Chivers counters that it’s also possible to lose money in any market on a reno and flip.

In Chivers’ view, the risks of employing this strategy will almost always outweigh the potential financial rewards, which is why she suggests investors take a different approach.

"If you buy in a low market and then renovate and fl ip, is that really the best market to sell it in? Or would you be better off buying low, popping a tenant in, and waiting for the market to change so you can renovate and sell when conditions have improved?"" she says.

Alternatively, if you try to buy, reno and fl ip in a rising market, such as Sydney at the moment, you could be overcapitalising and you may be paying an inlated purchase price.”

These risks have the potential to strip away your projected profits, so Chivers suggests investors continue with a reno and sell strategy – but tweak the timeline to adopt a longer-term view.

“I think a five-year plan can work best. Buy low, wait for the market to improve, then renovate and make some good money,” she says.

“The only caveat to this is if you can add a lot of value without a huge outlay, such as by adding another bedroom. If you turn a three-bedroom home into a four-bedroom home, and you’re able to create this extra bedroom by reworking your existing floor plan and without the cost and hassle of extending, then that’s another great way of adding value under a renovation strategy.”

Strategic renovation delivers six-figure profit

A strategic renovation to overhaul a tired, dated property in Sydney's west has achieved a six-figure profit for its owner. And according to renovation expert Cathy Morrisey, it's possible for investors all over Australia to replicate these results.

.PNG)

When Martin, a Sydney property investor, decided to sell his South Penrith investment property earlier this year, he initially intended to put it on the market in ‘as is’ condition.

Fortunately, his friendship with renovation expert Cathy Morrisey took things in a different direction – and it certainly paid dividends for the long-term investor. Read on for the full story.

Martin purchased the property as an investment in 2008, paying $330,000 for the four-bedroom home.

“After speaking to his agent, he was told that he could put it on the market in its current condition for ‘offers above $450,000’, and she estimated he wouldn’t get more than $500,000 for it,” Cathy explains.

This was partly due to Martin’s unique tenancy situation. For a number of years, his South Penrith home had been tenanted by the Department of Housing. “His real estate agent approached him a few years ago and told him the Department of Housing was looking for homes in the area to rent out to tenants, and he jumped at the opportunity. Not only was it a guaranteed tenancy with no vacancies, but as part of the agreement the department will pay for any repairs or damage done by the tenant,” Cathy says.

“The tenants didn’t physically punch holes in the walls or intentionally wreck things – it could have been worse. But the property was definitely in a tired state and needed a bit of TLC.”

Bankrolling repairs through the tenancy agreement

After agreeing to proceed with a renovation, with Cathy managing the project, Martin was pleased to discover a welcome silver lining of his departmental tenancy agreement.

“We spent around $25,000 in total on renovations, but he ended up getting $11,000 worth of repairs and upgrades paid for by the Department of Housing,” Cathy says.

Although it was dirty and tired, the bones of the property were in great condition – something that Cathy says is often the case with older homes. As a result, they didn’t “go crazy” by replacing the entire bathroom

or kitchen; instead, they looked for opportunities to add maximum value for minimal outlay.

“Just cleaning it up to begin with really made a difference, because it was in quite filthy condition. Then we commenced a lot of cosmetic renovations, such as painting the kitchen cupboards, replacing the shower screen and painting the bathroom vanity.”

Knowing that first impressions truly count, Cathy also focused on improving the property’s curb appeal.

They covered the unappealing baby-blue paint job with a modern grey tone, complemented by bright white window edges and charcoal trims. They also tidied up the landscaping to create a smart and welcoming entry.

Inside, other renovations included fresh paint, new carpets and new light fittings.

Sticking to a tight deadline

Cathy set a strict four-week timeframe for completing the renovation, which meant there were tradies coming and going at all hours of the day and night.

Before starting the renovation, Cathy did extensive research to ensure the reno and flip project would actually deliver. She reviewed the house across the road, which was a three-bedroom brick veneer home.

“Martin’s property was fibro, but we had four bedrooms where they only had three. It sold two months prior to the date that we commenced renovations for $599,000. That gave me the confidence to move forward with this project, knowing we would get a good return,” Cathy says.

“We were lucky, because the market was organically growing, which delivered a natural increase. But we achieved a final sale price of $658,000, and I think from where we started it wouldn’t have sold for any more than $550,000 in its original state. Realistically, this renovation gave him $100,000 profit. You really do have the potential to make a lot of money in a short period of time, and in real estate this is one of the best strategies to make cash fast.”

Key elements of a profitable reno and flip: 5 tips for success

Buy in a desirable area

“The places where we make the most money are the places where people really want to live,” says Cathy Morrisey. “Research is key.”

Look for evidence of success

Comparable sales of renovated properties help you plan your project from a financial perspective. “I make sure I have figures that represent what the nearest houses have sold for, post-renovation,” Cathy says.

Get educated

The biggest risk for the uneducated is “the potential to lose a lot of money if you buy a property that has not been researched correctly to renovate and profit", Cathy warns. “You must know your numbers to be successful at this game. I can't stress enough: educating yourself first will save you a lot of money in the long run, and cut years off your learning curve.”

Be strategic

Some renovations add more value than others, Cathy advises. “When you know that an extra bedroom is going to earn you more money when it comes time to sell, you can try and plan for these types of improvements that deliver the most bang for your buck," she says.

Set a firm budget

"I teach my students to stick to around 7% of the property’s value, pre-renovation, as a reno budget,” Cathy advises. “Going much higher than 7%, in my experience, can see investors overcapitalise and risk their profits.”

5 criteria for choosing the right suburb for reno and flip strategy

You can dramatically enhance your prospect of achieving big profits by ensuring that the suburb meets the following criteria:

1. Broad range of values

Your success as a renovator lies in finding a cheap property among very expensive properties that you can renovate quickly and cheaply. This won’t be possible if all the properties are the same price. Therefore, you want a broad range of properties in your target suburb.

2. Low days on market (DOM)

In order to lower your risks and costs, you want a suburb

where properties are selling quickly. This is indicated by the low days on market, which measures the time it takes for properties to sell once they’re listed for sale.

3. High auction clearance rate (ACR)

Hot markets generally have high auction clearance rates. You want your property to sell high and quickly if you’re renovating to flip.

4. Low proportion of renters

Owner-occupiers take better care of their properties than tenants, so there’s less chance of overcapitalising when renovating to flip in these markets.

5. High demand relative to supply

A market with a higher demand in relation to supply is obviously going to have better potential for growth, so make sure that you take this into account when you’re doing your research. While this may not factor in highly if you’re renovating to flip, potential buyers are likely to be interested in future growth. Indicators of demand include low discounting, high auction clearance rates, low vacancy rates and high yield.