Our experts explain how to make your property a weapon of tax deduction and save you 30% in next year’s tax bills.

Our experts explain how to make your property a weapon of tax deduction and save you 30% in next year’s tax bills.

Anyone who has experienced a few fairy tales as a youngster would recognise “Raise taxes!” as the catchcry of an evil king, bent on funding a few more royal banquets

David Shaw, director, WSC Group

WSC Group director David Shaw believes the following to be the main areas where people fall short on claiming correct deductions. By following these tips, he says you will be able to get additional tax benefits of somewhere between 25 and 65%.

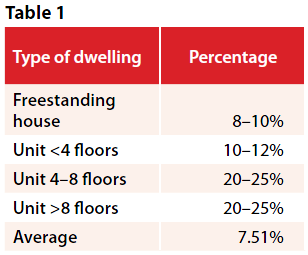

WSC Group director David Shaw believes the following to be the main areas where people fall short on claiming correct deductions. By following these tips, he says you will be able to get additional tax benefits of somewhere between 25 and 65%.People can still get a quantity survey for depreciation purposes and can claim depreciation on older properties. Even if they were built before July 1985 and building depreciation doesn’t apply, they’ll still get fittings depreciation.

Otherwise, they could miss out on between $2,000 and $10,000 per year on an average residential property, which is worth between $400,000 and $500,000.

2. Claim interest and holding costs during construction period

People who construct their investment properties can claim the interest and the holding costs during the construction period, according to the tax ruling 2004-4. Many investors miss out on that claim in the first year of construction, which can cost them between $10,000 and $20,000 in deductions.

3. Claim all charges to your property

There are a number of property groups out there that charge you a fee, but pay rental protection insurance to you if your property doesn’t rent. You shouldn’t assume that the fees charged are not deductible, especially in relation to rental protection insurance, which could be paid up to 12 months in advance.

4. Amend your tax return if you missed a claim

Tyron Hyde, director, Washington Brown

Tyron Hyde, director, Washington Brown

4. Deduct items as quickly as possible

Individual items under $300 can be written off immediately. An important thing to remember here is that provided your portion is under $300 you can still write it off.

For instance, say an electric motor to the garage door cost an apartment block $2,000. If there are 50 units in the block, your portion is $40. You can claim that $40 outright because your portion is under $300.

You can also try to buy items that depreciate faster. Items between $300 and $1,000 fall into the low pool category and attract a higher depreciation rate. So for instance, a $1,200 television attracts a 20% deduction while a $950 television deducts at 37.5% per annum.