In other words, the work you do now as an investor will secure your future.

This is the first discussion I had with couple Adam and Melinda. They are in a fantastic position to invest, but they had no idea where to start, what to buy or even what their goals were.

On a scale of 1 to 10, Adam’s appetite for risk used to be very high at 10. He has scaled this back to 8/10, now that he is married and has a family. He would feel comfortable engaging in strategies that could help them to fast-track the elimination of their mortgage.

However, Adam does not like debt – but he recognises that this is the right time for the couple to use the opportunity they have to establish a foundation that will allow them to reduce their PPOR loan in record time, while also acquiring assets that will support their lifestyle in retirement.

While Adam is comfortable in theory with leveraging and investing for his family’s future, I also have to consider the other influences that will put this to the test, not just for Adam but for Melinda and Adam as a couple. Melinda by her own admission is extremely reluctant to take on any extra debt and is very conservative about spending in general. Melinda rates her risk profile quite low at 2/10.

Melinda recognises that they need to be more creative to produce an outcome that would enable them to expedite the reduction of their PPOR loan.

Having two people who are so polarised in their risk profile can make for an interesting discussion and can sometimes result in me engaging in on-the-spot marriage counselling! Fortunately, in Adam and Melinda’s case, they are happy to focus on strategies that strike a balance between being conservative and taking some risk.

I’m so glad this couple is taking this proactive step forward, because too often I see clients who enjoy a strong and secure income that they take for granted by spending it all on lifestyle and consumables. It’s so important to consider the future, not only so you have financial security but also to ensure that you are not a burden on others.

The great news is, I’m a big believer that most investors can become financially secure regardless of their investment risk profile. Adam and Melinda are only 40, and I am confident that they can establish a strategy that will result in them reaching their first goal of fast-tracking the elimination of their PPOR while also accumulating a profitable property portfolio.

Our clients Adam and Melinda* have both recently turned 40. They have two children aged seven and eight, and both children are in private school.

Adam is the main income earner, working as a project manager at a large multinational company. Adam’s employment is considered secure and he has no intention of changing jobs in the next three years. His base annual salary is $270,000 plus bonuses and commission, which pushes his wage above $300,000.

Melinda works part-time and earns $40,000 per year. Melinda’s employment is also secure and she is happy to continue doing part-time work as her income contributes towards the everyday family expenses and overseas travel. Both of the couple’s parents reside overseas, so they have to make at least two major trips abroad each year to see their ageing parents.

After allowing for all the costs and budgeting for the family’s expenses and lifestyle commitments, they have the capacity to budget $3,000 each month towards investing in property.

The couple’s home is their only asset. It is valued at $1.5m, with a debt of $600,000. Based on an 80% LVR they can access $600,000 in usable equity to fund deposits and buying costs to acquire suitable investment properties.

Their broker has assessed that they have the potential for up to $2.4m in borrowing capacity.

* Names have been changed.

Properties are a medium- to long- term asset class ... the hold time should be around 10–15 years

The challenge:

To redeploy a $130k tax bill

Adam’s gross income is substantial, and well above the average wage. However, he has fallen into the trap of other professional high-end income earners who build their lifestyle around frequently rewarding themselves

for the hard work and high level of commitment and hours they devote

to earn their substantial salary. This can be counter productive from a wealth-building perspective and needs to be kept in check in order to effectively balance lifestyle with future wealth goals.

Without any efficiently structured investments, Adam is paying $130,000 each year in taxes. The amount he pays in taxes is more than some people and families earn in a year!

If Adam’s investment structures enabled him to divert his money away from the taxman’s pocket and instead back into his own pocket, he would then have a greater capacity to fast-track the reduction of his $600,000 mortgage on his PPOR. More importantly, he could also leverage himself into financially efficient, income-producing growth assets.

Currently, the couple’s capacity to leverage and service ‘good debt’ is high. Their conservativeness and aversion to debt is preventing them from optimising their potential to make a significant impact on their mortgage. In fact, their conservativeness is counterproductive and runs the risk of sabotaging their opportunity to reach the goal they have set.

What is the goal of these investors?

• Pay off their current PPOR loan of $600,000 as fast as possible. Property is the preference for the wealth creation vehicle they want to use to reach their first goal of paying off their home.

• Develop a passive income for the future of $190,000 within 15 years, to enable them to do what they want, when they want. This will be supplemented by their superannuation balance.

• Be able to do two overseas trips a year to visit both families.

3 STRATEGIES FOR SUCCESS

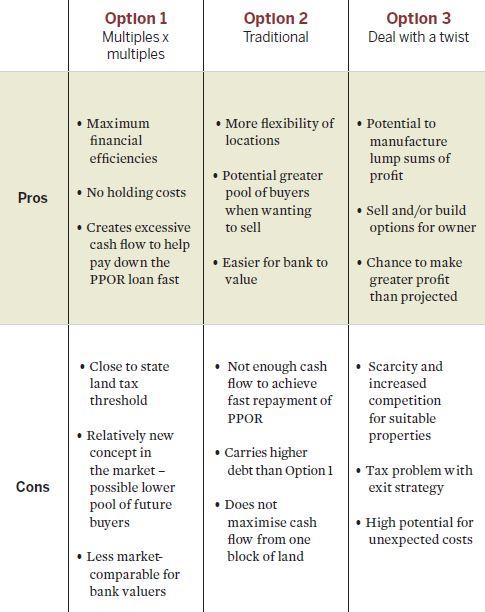

OPTION 1: Multiples x multiples

Build 3 multiple-income properties

• Passive acquisition strategy

• Lower acquisition costs

• Maximise financial efficiency through depreciation

• Positive cash flow

• Capital growth

This option caters to Adam and Melinda’s conservative risk profile while achieving their focus of eliminating their home loan as quickly as possible.

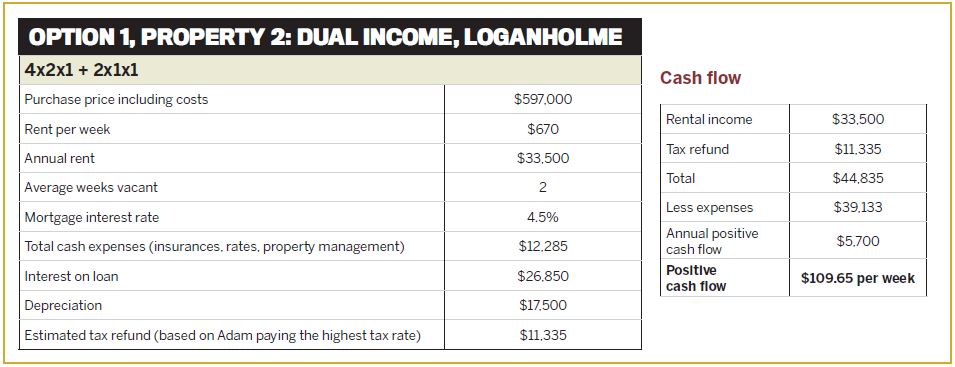

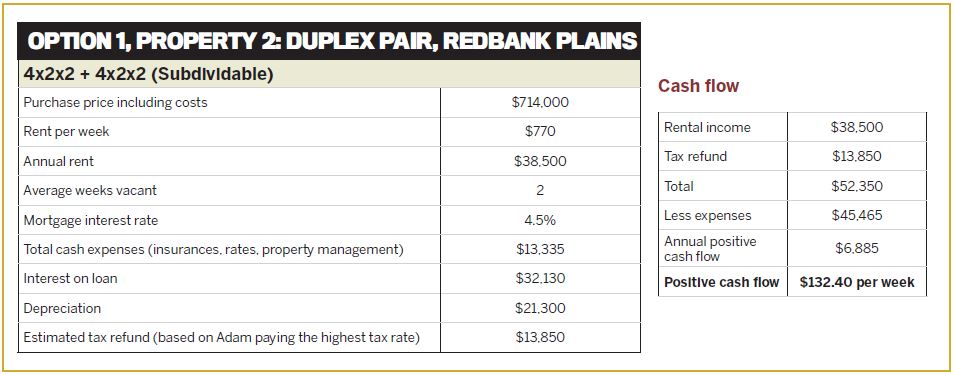

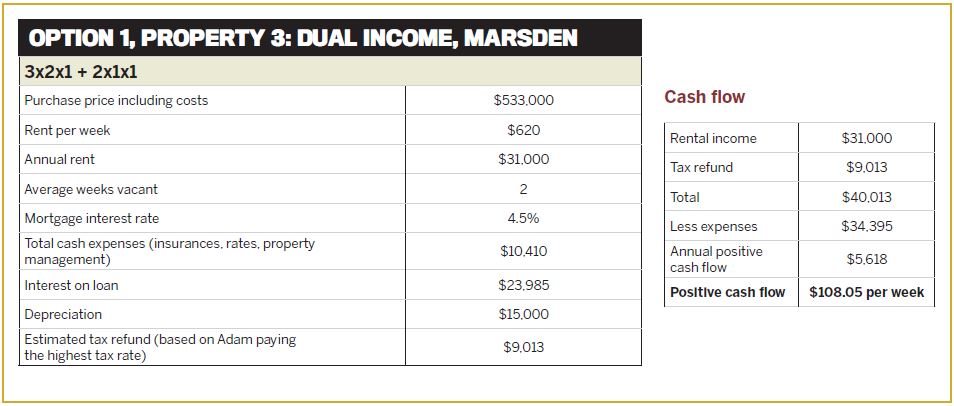

The three properties highlighted here (see boxouts, p49 and p50) fit this strategy as they produce positive cash flow and also allow Adam to extract the maximum income from one block of land, while also maximising depreciation, as these properties have more deductibility than a standard home.

The beautiful thing about depreciation is that you are able to claim a tax deduction without first incurring a cost (unlike any other deductible expenses), yet it injects cash back into your pocket from the tax refund you receive.

As this strategy needs maximum deductibility, this could also be achieved by buying a new established home. However, Adam and Melinda would have an extra boost if they built a new property, as demonstrated below.

Investment timeline

The multiples x multiples passive investment strategy recognises that properties are a medium- to long-term asset class. I like to emphasise that the hold time should be around 10–15 years.

Clearly, these types of properties are easy to hold due to their potential for positive cash flow. In addition to this, I would ensure that the properties are located in identified capital growth areas where the infrastructure and population growth underpin the long-term viability of the properties.

Growth over the long term will ensure that the properties are inevitably worth more in the future, and it would be expected that the right locations would run at growth ahead of inflation. While I do focus on the growth drivers when selecting a location, as mentioned above, I am usually conservative in projecting expectations of capital growth. Instead I prefer to focus on the income and financial efficiencies a property generates to determine its financial viability for the portfolio.

Proposed property acquisitions

The properties considered for this strategy are located in the Southeast Queensland growth corridor. Two of them are dual income, which provides enough of a financial upside to justify being considered for this strategy.

The potential downside of dual-income properties is that they cannot be subdivided. This makes them more affordable to acquire, as you don’t incur council contribution fees and you still benefit from the extra depreciation and cash flow compared to a standard house.

However, the exit strategy needs to recognise that you are not able to sell the separate sides individually.

As purpose-built dual-income properties are relatively new to the market, there is no long-term data to indicate their appeal in the years to come and whether the need to sell to a buyer wanting a dual-income property will limit the potential future pool of buyers.

Like any property, I see dual income dwellings as being a long-term asset that is profitable from day one. I expect the income that they generate will underpin the capital value of the properties.

All three Option 1 properties are based on a ‘build then hold’ strategy.

By acquiring three multiple-income properties, Adam and Melinda can spread the income generated from six modest rents, instead of relying on one tenant to pay one large rent.

The positive cash flow nature of these properties will enable Adam and Melinda to divert at least $100 each week from each property into their home loan.

As the properties don’t require any additional cash injections out of the weekly family budget, they will also still be able to contribute an extra $700 per week towards their PPOR. Combined with the extra cash flow of $300 per week from their investment properties, financial modelling demonstrates that the extra $1,000 per week repayments off their mortgage will enable them to:

• reduce their remaining loan term down to only seven years

• put $207,000 of interest savings back in their pockets, instead of the bank’s

The above assumption is based on the additional repayments being made to the loan on a weekly basis. To do this, Adam would need to lodge a PAYG withholding variation application. This will result in his employer deducting less tax from his pay, and instead of waiting to lodge his annual tax return to get his refund, Adam will get it in his weekly pay, enabling him to distribute his extra funds to his loan.

Once the PPOR loan has been paid off the couple can now divert their extra cash flow towards the next loan. To have the biggest impact on debt reduction, it’s important to maximise the contributions towards one loan rather than spreading the extra repayments over all the loans.

I have worked with many conservative couples who could only focus on repaying their PPOR with the income left over from their after-tax dollars and not leverage into any investment properties until their PPORs were paid off. Fortunately, Adam and Melinda don’t have as narrow a focus and are still willing to embark on strategies which can achieve both, enabling them to have their home paid off as well as their investment properties.

In other words, they can have their cake and eat it too!

Mortgage management tip

My preference, if possible, is to not rely on the predetermined payment schedule set by the bank, because, let’s face it, the bank’s business model flourishes when you make the lowest repayments over the longest possible term.

Rather, always pay into the loan on a weekly or fortnightly basis, because this has the largest impact on reducing the interest charged, as interest is calculated on the daily balance.

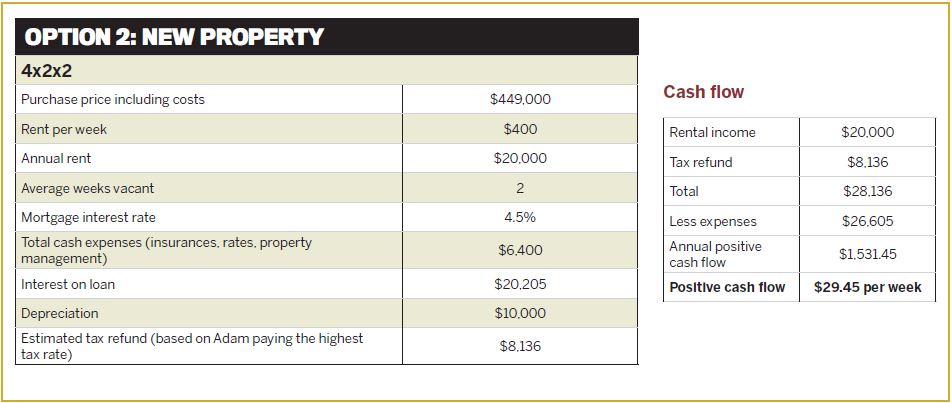

OPTION 2: One property at a time A variation of the above ‘multiples x multiples’ strategy could be a more traditional ‘one at a time’ strategy.

In this case, the couple could buy

a modern three- or four-bedroom home. However, financial modelling in this scenario is less attractive, for the following reasons.

With a deposit of $600,000 and assuming an 80% LVR and 5% buying costs, the total amount they could borrow to either build or buy established properties would be $2.4m. This would need to be done gradually so that the additional income from each property would contribute to their serviceability from the bank’s perspective and also give them the best borrowing capacity through the acquisition process.

On an established property priced at $449,000 and assuming an 80% LVR,

$90,500 would be used for the deposit and $17,500 would cover the buying costs.

The borrowing capacity for each lender varies, depending on how each bank’s formula for calculating serviceability is structured. Based on income and projected serviceability, assuming a 5% gross return on each property, Adam and Melinda would only be able to buy five additional properties with a total property value of $2,245,000 and costs of $87,500, giving them a total debt of $2,332,500.

Some issues that could result include:

• If buying established properties, Adam and Melinda would incur higher stamp duty costs, which are less tax effective than enjoying the deductibility of interest incurred on the loans during the construction.

• A standard house doesn’t create as high a cash flow as the couple would get from a multiple-income property. In most cases, even if the property being purchased is modern, it will still be negative or at best neutral from a cash-on-cash perspective. This means there will be less funds available to divert towards the PPOR loan they are trying to eliminate.

• While they could build a standard home, as it would enable them to maximise their depreciation, the cash flow buffer upon completion would be a lot smaller, as demonstrated by the figures in the table above.

We can see clearly from this example how a new build would at best be approx. $30 per week positive. Meanwhile, a multiple-income property based on Adam’s tax bracket generates at least $100 in positive cash flow, with a similar location and land size.

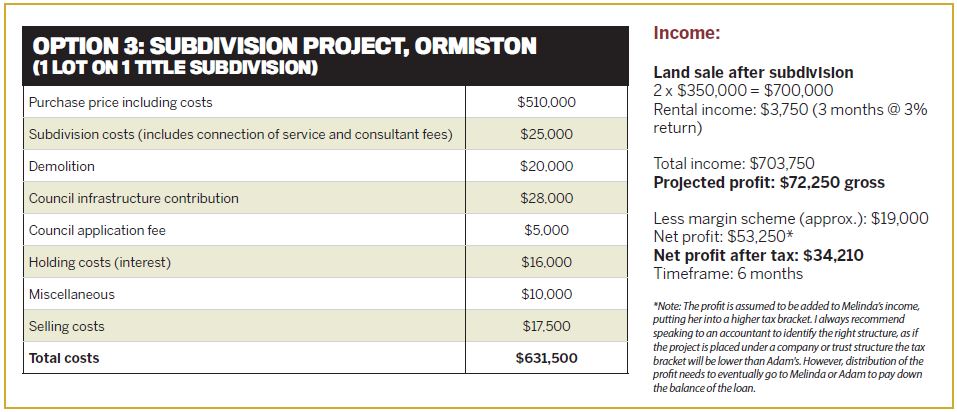

Option 3: A ‘deal with a twist’

Due to Adam’s income bracket, it’s important that any strategy should consider the impact taxation will have on the bottom line of any project.

To reduce debt, a ‘deal with a twist’ would only be an option for Adam and Melinda if the end result enabled them to make a lump-sum repayment off their mortgage.

As Melinda’s income is in a much lower tax bracket than Adam’s, it would be wise for them to discuss with their accountant whether a project should be purchased within a trust structure or solely in Melinda’s name to minimise the overall tax payable.

Taking all of the above into consideration, let’s look at the types of property investments that would be suitable for this strategy (see tables above).

Splitter/subdividable block

Splitter/subdividable block

This involves buying an existing property where there is sufficient land and appropriate zoning that allows you to retain the existing dwelling while splitting or subdividing the block to create another title.

Once the project is completed there are a variety of options to hold or sell; however, as the ultimate purpose of the strategy is to create a chunk of money to pay off the PPOR mortgage, the feasibility needs to show that there is viability to sell at least one of the properties.

The project needs to consider not only the value created, the holding costs and all costs associated with undertaking it, but also whether upon the sale of one block the bank will require any debt to be paid down from the profits of the sale. This is because the remaining property still needs to satisfy the bank’s LVR for the retained property.

Options include building on the vacant land to take advantage of the depreciation benefits, or building on the vacant land and selling the new house.

Which of the three options is the best way forward?

For these investors, based on their level of conservativeness and risk profile combined with the sole focus of being able to eliminate their PPOR loan, Option 1 (multiples x multiples) is best.

It offers the financial efficiencies that Adam needs to reduce his tax obligations, while also providing for the cash flow that effectively enables Adam and Melinda to control an investment portfolio valued $1.8m with no out-of-pocket cash holding costs.

Adam is able to claw back $34,000 annually in taxes, which he can now combine with the family’s cash surplus of $36,000 to fast-track the repayment of their mortgage.

Final considerations

With all investment strategies, you need to consider: what are the biggest risks for the investor’s future, and what can they do to mitigate these risks?

Adam and Melinda’s conservativeness and aversion to debt may hold them back. It could prevent them from acquiring the types of properties that would expedite the elimination of their mortgage via the establishment of a portfolio that enables them to track towards a passive income in retirement.

Conservativeness may delay their decision-making process, causing them to miss opportunities, and slowing their momentum down. Often as an investor you need to be quite decisive in your approach. Due to their diverse risk profiles (Melinda, 2 and Adam, 8), it may be difficult for them to come to a consensus.

I’m a big fan of assisting my clients in gaining control of an opportunity, with a safety net to protect them if for any reason they don’t want to proceed. By doing this they can be confident in making quick decisions while protecting themselves from making the final decision until they have had time to completely assess a project.

Disclaimer: The advice contained in this article is for general information only and should not be taken as financial advice. Please make sure to speak to a qualified professional person before making any investment decision.