Depreciation is essentially a tax deduction available to property investors. Your investment property earns an income (in the form of rent from your tenants), so – as with any activity that produces an income – there are various tax deductions available to you.

Normally these tax deductions are things you’ve spent money on, such as property management fees, council rates and other miscellaneous items. You pay an amount of money, you receive a tax invoice and receipt, and you use that piece of paper to claim a tax deduction when tax time comes around.

However, property depreciation is what the tax office calls a ‘non-cash deduction’ – which means you don’t physically fork out cash in order to claim a deduction. I have also heard it referred to as ‘on-paper deductions’ for the same reason. Depreciation allows you to claim a tax deduction for the wear and tear on an investment property over time.

This tax deduction recognises the fact that the building itself, as well as its plant and equipment (air conditioners, blinds, carpet, etc.), will become worn out over time and eventually need to be replaced. It doesn’t matter that these items were paid for by someone else – a developer or previous owner – you, the current owner, can continue to claim deductions as they continue to depreciate in value.

How is it calculated?

The two accepted methods of depreciation calculation are:

-Prime cost or straight-line method

Calculates your depreciation deduction evenly over the useful life of the item. For example, if an item costs $10,000 and its useful life is 10 years, it will be depreciated at a rate of $1,000 per year ($10,000 divided by 10).

-Diminishing value method

Allows you to depreciate the item in question more quickly up front. This recognises the fact that most plant and equipment items tend to lose a higher proportion of their value earlier on.

As with any tax deduction, depreciation basically reduces your taxable income. So if your income is $100,000 for the year and you claim $10,000 worth of deductions, you only pay tax on $90,000.

Each property is different and many varying factors must be considered when preparing a property tax depreciation schedule. Try searching for a free property tax depreciation calculator online to get an estimate of potential depreciation deductions.

The dos and don’ts of claiming

As mentioned earlier, air conditioners, blinds and carpets are some examples of items that can be included in a depreciation claim. There are hundreds more items found in the vast majority of Australian investment properties that you may also be entitled to claim on. An accredited quantity surveying firm will know exactly what to look for, and it’s likely that the more experienced the company, the greater the deductions for the client.

For example, in a typical unit block or high-rise apartment building there will be a considerable amount of common property and assets. Engaging a qualified and experienced quantity surveying firm will ensure that you are claiming your portion of this. The accurate inclusion of items such as pools, gyms, car park assets and lifts, as well as security and fire safety assets, will significantly increase your deductions.

When it comes to renovations, many people don’t realise they can claim depreciation, and therefore miss out on potentially thousands of dollars in tax deductions. Depending on the item itself, some common renovation inclusions can result in ongoing yearly tax deductions for the next 40 years!

Also, items that cost under $300 can be deducted in full straight away, which immediately boosts your tax deductions for the year. Due to the costs involved and the usual inclusions, kitchen and bathrooms renovations typically yield the greatest depreciation allowances.

Lesser-known construction elements that can and cannot be claimed on

Can claim

• Design/professional fees

This includes costs associated with architectural fees, engineering costs and any other design fees that were an essential part of creating the property.

• Council costs

A lot of investors overlook claiming the costs associated with council fees related to application submissions. This is not just limited to building application and development application fees but may include council contributions, for instance costs a developer may have to spend on local community works like building a playground.

• Building Profit

If you engage a builder directly to complete your investment property, then the profit component of the work can also be claimed.

Can't Claim

• Site clearing

Similar to demolition, the costs associated with clearing the land are not eligible to be claimed. These two jobs essentially involve getting the site ready to begin work. However, it is important to note that excavating the site for a basement can be claimed as that is considered part of the new basement.

• Landscaping

Soft landscaping such as trees and grass, which grow, don't depreciate over time. However, it's worth noting that landscaping can consist of different elements. Hard landscaping items such as as retaining walls can be claimed. So it's important to distinguish between the two. In summary, if it grows, you can't claim it.

• Developer's profit

If you buy property from a builder/developer, the developer profit cannot be included as a construction cost.

Avoiding the ATO

With the ATO targeting property investors in the 2015/16 tax year, the best way to avoid attracting unnecessary attention from the ATO when it comes to your depreciation claim is to engage an expert.

Using a firm that specialises in depreciation, has at least 20 years’ industry experience, and that is a registered tax agent will ensure that you are within ATO guidelines, that you are audit-ready, and that you are receiving the maximum legal depreciation deductions.

You also want to make sure the property is inspected as part of your tax depreciation report. A comprehensive ATO-compliant depreciation schedule that includes an inspection and outlines both methods of depreciation calculation over 40 years should typically cost around $770 including GST for an average residential property in a metropolitan area.

Some cheaper operators exist in the market but rely on the owner to provide the specific and detailed information regarding items they can potentially claim on. This DIY approach leaves the owner exposed if the ATO ever wishes to question any of the deductions claimed as part of the report.

It is important to note that depreciation is the only part of your property investment tax equation that is subjective. The amount you are able to claim is a direct result of the collective skill, experience and reputation of the firm preparing the schedule. The figures can vary significantly due to these factors.

Also, unless you plan to carry out extensive renovations/extensions to this service is fully tax deductible, it is worth spending a bit more to ensure that the firm you engage is going to conduct an inspection (in the case of a pre-existing property) and that you are going to get the highest possible ATO-compliant deductions.

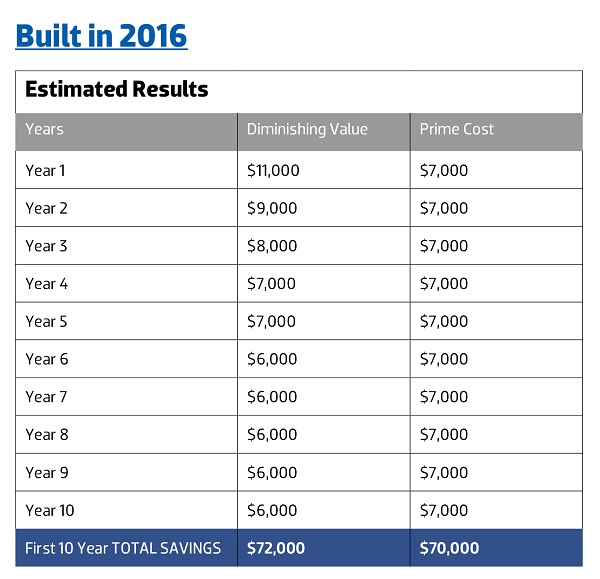

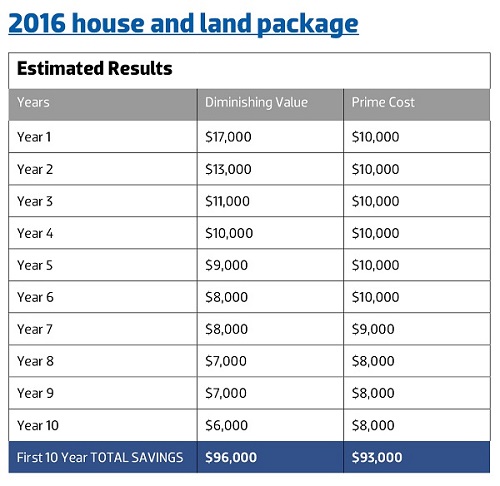

Tax depreciation benefits are greatest when the property is brand new. With brand-new property you maximise your available tax deductions, which adds a significant boost to your cash flow position.

Depreciation allowances for new properties can yield big tax breaks. Investors can claim a 2.5% depreciation allowance on the construction cost – plus be entitled to claim the full amount of depreciation allowances on plant and equipment items such as blinds, ovens, carpets and air conditioners, which will all be brand new. For a brand-new apartment purchased in Melbourne for $700,000, you could expect approximately $19,000 in tax depreciation benefits in the first full year.

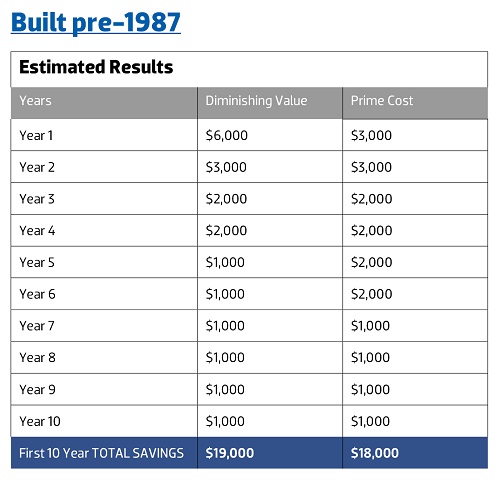

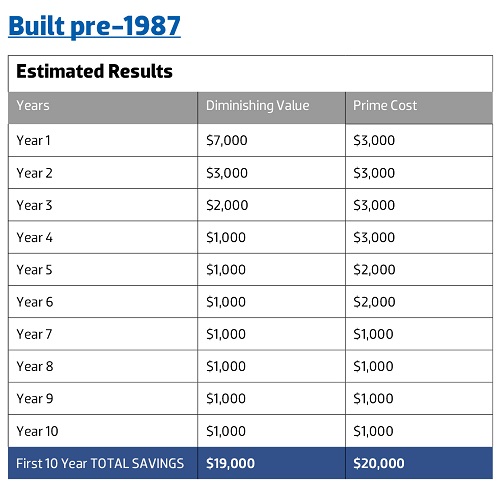

It is important to remember, though, that even properties built before 1985 (when the building allowance kicked in) are worth depreciating. If you had just paid $700,000 for a house in Melbourne that was built in the early ’80s, a first-year deduction of around $6,500 is very likely! Despite the property being older, there is still some value associated with the plant and equipment items, and you are entitled to claim depreciation on this.

Even if you’ve purchased a property that previous owners have renovated, you may be able to claim a depreciation benefit. In accordance with ATO requirements, as long as you are using the property for income-producing purposes you are entitled to claim depreciation on renovations completed after July 1985, regardless of who paid for them.

Tax depreciation calculator

“If only I knew then what I know now!” the saying goes. But when it comes to depreciation, you can! Investors can use the Washington Brown Tax Property Depreciation Calculator free of charge to produce an instant estimate of the likely tax depreciation deductions on a property before they buy it. While expected depreciation results should never be the sole reason one purchases a particular property, knowing the approximate depreciation deductions can certainly help when looking at projected cash flow and affordability post-purchase.

This calculator uses real-life data collated from every inspection we do on behalf of our clients. So the data gets more accurate with time.

The following examples show Washington Brown Property Depreciation Calculator results produced for a number of property types of varying ages at different purchase prices.

Tyron's top depreciation tip

Don’t bother with DIY depreciation.

As an expert in the market, I am baffled by the number of companies offering a DIY option. I personally think there are some legal anomalies here, but, more importantly, I think you will be missing out on deductions. Here’s one example.

The DIY options in the marketplace give you a tick sheet and ask you to take your own measurements. Now let’s say you measure from one bedroom wall to the other. If you do that all around the house you would reduce the property by 10% in gross area. At around $1,500 per square metre to build, you would have missed out on something like $15,000 worth of tax deductions.

But don’t just take it from me. General manager of the Australian Institute of Quantity Surveyors Terry Sanders says: “The AIQS has produced guidelines for the preparation of property depreciation reports by qualified quantity surveyors, which are aimed at ensuring property owners get a comprehensive and professional report that meets the ATO’s requirements.” He adds that owners who attempt to estimate their own depreciation, or who use non-qualified quantity surveyers, risk submitting an incomplete or poor depreciation report which “could not only cost them in missed deductions but could also possibly attract an audit by the ATO if their report is not up to standard”.