IT IS a universal truth that everyone wants a secure future so they can live out their golden years in comfort. In our youth, we study with the aim of being able to land great positions in the workforce. Then as working professionals we strive to build up a nest egg that will enable us to live comfortably and be prepared for emergencies as we ease out of our working life.

“In general, people should anticipate needing between 70% and 80% of their pre-retirement income after they retire in order to maintain the same standard of living they’re used to,” says Laura Menschik CFP, director of WLM Financial Services Pty Limited.

“If they want to travel more in their retirement, then the cost needs be added into the budget for the years planned, such as $10,000 every two years. Also, an allowance for upgrading a motor vehicle should be added; if $10,000 is needed to upgrade a car every few years, then you would need to allow an additional $2,000 per annum in their budget.”

This income level can be difficult to save ahead for if you’re working a typical day job, especially for families. As a result, many look to invest in property to grow their finances through a passive income stream. Other popular methods of generating retirement income include superannuation pensions, index funds, term deposit interest, share dividends, and unit trust or managed fund distributions.

For everyday Australians, living off a property portfolio’s rental income is a particularly appealing option. A good portfolio can be built with proper research and guidance, and the income generated can be sustained for a long period of time – while you hold on to the underlying asset.

In fact, there have been many success stories of typical middleclass employees succeeding so well at investing that they are able to retire early from nine-to-five jobs and either make a living out of their properties or spend their days travelling in style. But just how does one get to that point of financial independence through property investment?

“Most property investors lack an overall strategy – the most common misconception is that you should just buy as much property as possible and it will all eventually work out”

How much income do you need?

The Association of Superannuation Funds of Australia (ASFA) offers an annually updated Retirement Standard to guide it in determining an adequate annual budget for living without an active income. This standard is regularly updated to account for factors like inflation, and goes into detail about the likely expenditure both individuals and couples should budget for.

“For Australians looking to retire at the age of 60, the average male has a super balance of $292,510 and the average female has a super balance of $138,154. From age 60 to 64, at the minimum pension draw-down rate of 4%, a couple’s combined super pension income would be approximately $17,226,” explains Dominic Aarsen, CEO of MakeTheMostOfYourMoney..JPG)

“From 65 to 74 the draw-down rate increases to 5%, meaning a combined pension income of $21,533.” The roughly estimated budget for singles to have a comfortable living is about $40,000 per year, according to ASFA, whereas for couples without children it is approximately $60,000.

While this takes usual needs into account, it doesn’t factor in many of the luxuries you typically want to experience upon hitting retirement, like travel, eating out, engaging in hobbies, or perhaps upgrading your home – nor does it consider emergencies such as illness or accidents, which can eat up a sizeable chunk of your savings in a very short time. This is where investing in property can help you significantly.

“With an investment property in addition to your super balance, an average weekly rent of $500 would add an estimated $26,000 to your annual retirement income. Combining the minimum pension withdrawal of $17,226 with $26,000 from your rental property results in an annual income of $43,266,” Aarsen says.

“Your retirement income can also increase significantly depending on your entitlement to the aged pension or partial aged pension, which can reach up to $36,301 per year. Just one investment property could be the difference between living a moderate or comfortable retirement.”

Planning effectively for retirement is a process that should begin early. Most retirees in Australia are working with annual incomes in the range of $60,000 to $80,000, which doesn’t leave a lot left over for saving for retirement.

“At the very least, for those on average incomes, your goal should be to replace your income in retirement with your mix of superannuation and potentially other investments, which might include shares, managed funds or property,” says Ben Kingsley, managing director of Empower Wealth.

“There are different price points you can enter the market at. Your job is to find the best locations that will deliver the best returns”

“Those who shoot the lights out by generating over $100,000 in passive income in retirement would, more than likely, have been disciplined with their money, invested wisely and, more often than not, started their investment journey early.”

This journey ultimately begins with determining what you will need in retirement in accordance with your personal situation and lifestyle. The ASFA standard is a good measure of what the typical individual or couple will need, but ultimately, the best way to know how much you ought to have in retirement is to examine your own circumstances. “I would recommend that every investor review their own annual expenditure to establish how much they would need to live off, as it really differs from person to person,” says Joshua Dalton CFP, director at Dalton Financial Partners.

In this case, it is wise to consult a financial advisor who can take a good, hard look at your expenses and earnings and tell you where you’re at before you start on the investment road.

How to generate income in retirement

.JPG)

When you have a clear view of where you’re at and where you need to be by the time you hit retirement age, the next step is to figure out what you need to do to make that kind of income happen.

“Most property investors lack an overall strategy – the most common misconception is that you should just buy as much property as possible and then it will all eventually work out. This thinking is normally based on other investors’ past successes, but I think people need to be more selective when it comes to property in the current market,” Dalton says.

This mindset can cause those with funds at their disposal to make unwise purchasing decisions, because they have the means to take action – but not the education or a clear strategy.

Many also mistakenly believe investing is only for ‘the rich’, which Kingsley counters is false.

“Contrary to popular belief, and indeed a lot of misconceptions out there, you don’t need to have a big income to invest in property; you can look for properties that offer a good mix of rental income and capital growth,” he says. He highlights four “levers” investors can use to build wealth through property investment: income, expenditure, time and target.

Income. is where it all begins, as it dictates how big a loan you will be able to get; naturally, it also determines how much your net profit will be after accounting for expenses.

.JPG) Expenditure is what many struggle with and what aspiring investors have to overcome, especially in today’s instant gratification culture in which the temptation is to live – and spend – in the moment. You need to balance being able to live comfortably today with budgeting well enough to live comfortably tomorrow.

Expenditure is what many struggle with and what aspiring investors have to overcome, especially in today’s instant gratification culture in which the temptation is to live – and spend – in the moment. You need to balance being able to live comfortably today with budgeting well enough to live comfortably tomorrow.

Time is your deadline: when you want to be free of the typical rat race. While most of us want to stop having to work as soon as possible, the feasibility of this varies, and so you have to set your own investment timeline based on your income levels and spending habits. Your timeline helps you refine your target, which ultimately shapes the kind of portfolio you construct.

Target – or your goal – is the most crucial aspect of investing, whether you do it for the purpose of early retirement or not. “If your target is only to have a comfortable retirement income – no investor will be targeting a basic or standard living in retirement – then the time to achieve this target might be in earlier retirement. Hence, the use of levers,” Kingsley explains.

“If you want a bigger wealth base and passive income in retirement, then you might need to extend the time frame out to, say, 65 years of age. You must be diligent in working through each expense item, based on essential spending and discretionary spending, to trap as much surplus as you can and then put it to work as soon as possible.”

With this in mind, you can begin to work out the right strategy to apply to your investment portfolio.

“Once you know the surplus you have and the borrowings you can obtain, you must go after the bestsuited property you can. If your surplus is strong, you can focus on capital growth properties, given that, traditionally, these offer less rental yield and hence your own money can cover the shortfall,” he says.

“If you have less surplus, the pendulum swings in the other direction to chase high-yield, cash flow-style properties – just make sure they don’t also have high holding costs!” Generally, most investors will be in the middle, with a surplus that’s neither particularly high nor especially low. Thus, Kingsley advises the building of a balanced property portfolio composed of investments that produce ‘middle of the road’ yield but have potential for longterm growth.

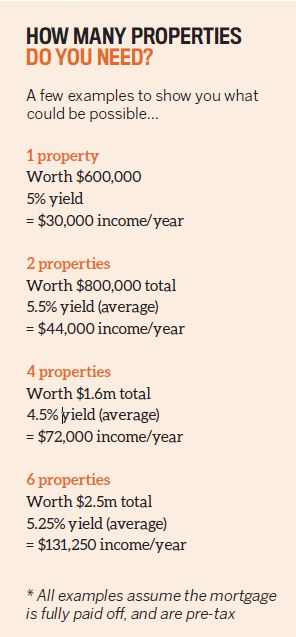

.JPG) How many properties will get you there?

How many properties will get you there?

You’ve decided on the right investment strategy and you’re working towards building a portfolio. You know that it’s not just about buying as many properties as you can afford. But how many do you really need to get to that nice, cushy retirement?

The answer lies in the return you get from your investments, both short- and long-term.

“Different locations and properties can deliver different returns. Right across Australia there are different price points you can enter the market at. Your job is to find the best locations that will deliver the best returns. And you don’t need 10 or 20 properties – two to five really good ones will do all the heavy lifting you need to achieve your financial goals,” Kingsley says.

“However, around 72% of all property investors own just one property. That should give you a clue that not too many are shooting the light out when it comes to getting a great return.” For most people, a portfolio worth around $2m is about the sweet spot – in accordance with their personal risk profile, investment timeline and goals.

Your portfolio could be composed of four property assets worth $500,000 each, two assets at $1m each, or even six assets worth $350,000. The key is to narrow it down to the precise figure you need and work backwards.

“Start with your spending habits and work out from there the cash flow you receive from each property, adding in CPI as living expenses will increase each year. This will help you work out the magic number plus volume of properties required,” says wHeregroup director Todd Hunter.

“There are also various strategies that could help investors get ahead of the game, like renovating, flipping, subdivision, investing in overseas property, and buying well below market value.”

Dalton also suggests that investors look into putting their properties under their SMSF, which could help them avoid having to pay taxes in the long run.

“Once you establish how much you need to cover your annual living expenses, you need to gross this amount up for tax. The tax would depend on how your properties are owned, though ideally the income should be split between a couple,” he says.

“Investors would benefit from property owned in super, where earnings may be tax free once you reach preservation age – 60 for most people. You could also buy property with more capital gain potential, then sell it at a later stage to purchase higher-yielding investments; these are normally commercial property, residential units and townhouses.”

By focusing on the numbers, investors can make informed rather than emotional decisions when it comes to buying the right type of property for their portfolios.

How realistic should your expectations be?

How realistic should your expectations be?

When it comes to investing, many things are far easier said than done. So without a well-rounded view of the hard work it takes to get rental income flowing, you could end up making potentially costly mistakes that lengthen the road to retirement.

One mistake that investors often make, Hunter says, is “setting up investment loans as interestonly – and then only paying interest-only”.

“The fastest way to get ahead is to pay down debt. Combining this with increasing your rents where you can, plus capital growth, is the fastest way to create equity within your portfolio,” he explains.

“Not every property you own is going to be a hit; every investor with a portfolio has properties that perform better than others. Sell bad investments and get investing again.”

When it comes to debt, however, Menschik has seen investors who have a rosy view of their financial situation that doesn’t entirely match up with reality.

“They think their debt will be repaid more quickly than they really are able to repay it; that the property will always be tenanted; that the value will always increase; that maintenance costs will be easily managed; and that it will be easy to sell if they need money quickly,” she says.'

“Rather, investors need to start planning early, set goals, ensure their needs are covered, and save regularly. Invest in what you understand, and/or seek professional advice along the way. Follow your plan, but review it and revise it regularly.”

Indeed, the ‘get rich quick’ perception is a misconception that many investors fall prey to. “It’s the one that does most of the damage to people’s future retirement. Don’t chase the silver bullet, because maybe 1% of people are successful. That leaves the other 99% out of pocket,” Kingsley says.

“The vast majority of people across the world have achieved financial peace slowly and steadily, learning the process and getting educated and better at it along the way.”'

Property investment is a long game, so it’s important to plan with near-future changes in mind, such as whether you may want to start a family in the next few years.

You also need to ensure that you have a considerable amount of savings in your emergency fund – enough to see you through for six to 12 months, in the event of a sudden disaster. If you have less than six months’ worth of funds, in terms of covering your basic housing and food needs, you could run into trouble.

Moreover, down the line, your loans may shift from interestonly to principal and interest, and you need to be financially prepared for the effect this will have on your cash flow. “It’s ultimately the planning decisions – the trade-offs between the here and now versus your future – along with your property strategy in terms of what to buy, and your ability to buy well, that will determine your future retirement result,” Kingsley says.

“If property investment was easy, then everyone would be doing it, and everyone would be doing it well. But it is very much a case of tailored approaches for each individual or household as opposed to a one-size-fitsall strategy. Property investing is an investment science; it’s a process of elimination.”