The debate over whether a free-standing house is a better investment compared to units remains a hot button issue among investors.

So, in this article, I’ll dispel a common myth about the houses vs units debate using statistics. It’s sure to challenge well-established ideas and highlight how hard it is to find investment grade units.

Disclaimers

I have to say that less than 10% of the properties I’ve bought have been units. You might think that disqualifies me as an expert on the subject of ‘rules for investing in units’, but that’s missing the point.

You see, I’ve always been open to buying units. However, there’s something more important than units vs. houses – it is risk vs return.

After considering risk and return for thousands of potential investments, I simply haven’t found as many great opportunities that have been units compared to those that were houses.

Land asset ratio

Most investors think that houses make better investments because they have a higher component of land. After all, it is land that appreciates while buildings depreciate. That’s true, but do you know how much it costs for a developer to build a single unit?

Per unit, the construction cost is easily under $200,000. But the construction cost could easily be double that for a two-storey house.

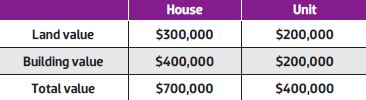

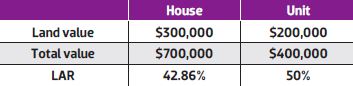

Let’s look at a hypothetical example to get to the crux of the issue about land content.

Assume we have a house and a unit in the same market. The house is worth $700,000 while the unit is worth $400,000.

Both were constructed at the same time. The construction cost of the unit was $200,000 while the construction cost of the house was $400,000. That means we have the following:

This might be a slightly unrealistic example, but what matters is how we break down the data and examine it to see what is really going on.

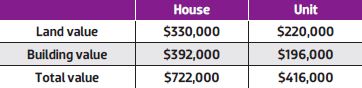

The house might be on 500sq metres of land and the unit’s total floor space may only be 90sq metres. So it’s clear which property has the higher land component. But let’s see what happens to the values if there is 10% capital growth.

Now remember that land appreciates while buildings depreciate. So only the land has grown by 10%. The buildings have actually depreciated by 2% over the same time frame.

So we now have:

The land for both properties appreciated by the same amount: 10%. That moved the house’s land to a new value of $330k. The unit’s land component moved from $200k to $220k.

But note the 2% depreciation has brought the building value of the house down from $400k to $392k. That’s 2% of $400,000, which is $8,000.

A similar thing happened to the unit. But since its construction cost was lower, the loss is smaller – 2% of $200k is only $4k. So the new building component is now $196k.

Who won?

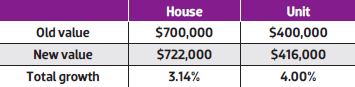

Did the higher land component of the house make it a better investment? No.

The percentage growth of the house was only 3.14%. That’s $22k as a percentage of $700k.

The unit on the other hand experienced an overall growth of 4% over the same period.

The point is that although the house has more land, the proportion of land in the total asset’s value is lower than for the unit.

The unit has a higher land to asset ratio or LAR:

It’s not how much land, but how much of the total value of the asset is attributable to land in percentage terms. The higher the LAR the more of your money has purchased land.

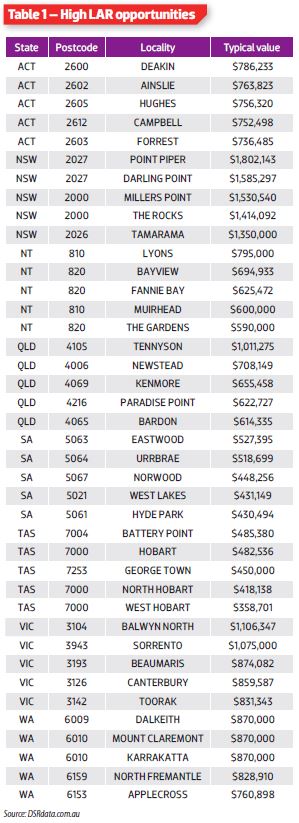

The highest LAR properties you will find are on the most expensive land and have the cheapest dwelling on them. Although this might be a house, quite often you’ll find units with higher LARs than houses around the same price tag.

Factors to consider

Factors to consider

Now before you go off buying some of the most expensive old apartments in the country, there are a few gotchas to consider.

1. Development opportunity

One of the major reasons why houses make better investments than units is development potential. A unit is already fully developed. But depending on the amount of land available and the council zoning, a house may have tremendous value-adding opportunity.

There may be little difference in long-term capital growth potential between a house with no development potential and a unit in the same street. So don’t just blindly choose a house – check out its development potential.

2. Cost

One of the arguments in favour of units is a lower entry price. In order to afford a house of equivalent value, an investor may need to venture away from safe economic epicentres or wait longer for the deposit.

A unit is better than nothing and getting in early is better than waiting.

3. Rental demand

Demographics are shifting. A lot more people are choosing an apartment lifestyle. For some, it is the convenience of being closer to desirable amenities or not mowing a lawn.

Depending on the nature of the area, it’s quite possible the demographic is happy enough to live in units. The customer is always right, right?

One problem with units, however, is that there can easily be an oversupply. Units come in a block. It’s hard to say one unit in the block is unique.

Units also come onto the market at the same time. That means there may be a number of landlords looking for a tenant at the same time with little to compete with other than lowering rent.

4. Yield

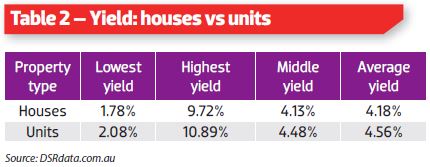

The yield for units is generally higher than the yield for houses. Table 2 shows a summary of some yield figures for houses versus units in capital cities around Australia as they were at the end of 2015.

Yield is not the most important part of creating wealth through property. But it becomes very important when investors approach loan serviceability limits or when it’s time to retire.

5. Capital growth

Capital growth is the ant’s pants of property investing. This is what makes investors wealthy. Long term (around 20 years), it is hard to argue a case for units. Houses will not only have development potential but scarcity value too, as more units pop up.

However, in the short term (less than 10 years) it is quite possible that a specific unit market will outperform a certain housing market. It all comes down to supply and demand.

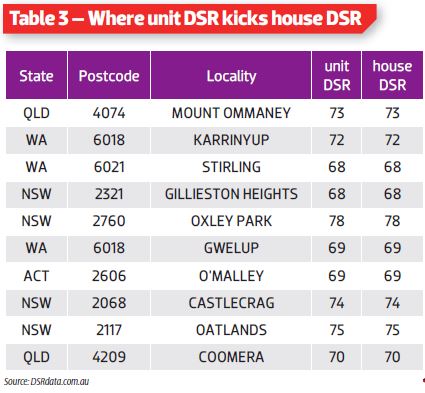

If demand for units exceeds their supply, then of course prices will rise. The degree to which demand exceeds supply, that is the demand to supply ratio (DSR), will determine the level of pressure there is on prices to rise.

If the DSR is higher for units than it is for houses, then you can expect prices to rise faster for units than for houses in the short term.

Table 3 shows a list of property markets in which the DSR for units is comfortably higher than the DSR for houses.

6. Depreciation

6. Depreciation

Depreciation is often thought to be higher for units than it is for houses. This is because the common thinking is that a unit has no land, it’s all building.

But, as can be seen from the section previously discussed about the Land Asset Ratio (LAR), this might not hold true. It’s quite possible that a house will have higher depreciation.

A valuation that breaks up the ‘land’ value and

‘improvement’ value will help. Better still, a depreciation report will give a precise breakdown.

Also, note that depreciation should not be a big drawcard anyway. Whatever you claim as a tax deduction for depreciation has to be put away for some future day when you actually need to replace that depreciated item. Depreciation is not a gift from the government.

7. Oversupply potential

Obviously investors want limited supply of additional stock around their investment property. This ensures greater capital growth potential. Any additional developing will diminish that potential.

The infrastructure government must provide to support a new suburb is a big drain on their budget. Allowing a developer to knock down a house and build a block of units doesn’t require such costly additional infrastructure, such as roads, electricity, water supply and sewerage.

You’d expect the cost to be passed on to developers. But developers may consider that additional cost unfeasible for the project. So it’s easier to go up rather than out.

Given decreasing availability of land, the easy option is to build more units, not more houses.

This doesn’t mean houses are a sure thing. Councils can rezone areas to allow for greater density dwellings. But, in this case, being a house owner is a bonus with the opportunity to develop.

Picking the right suburb for units

The best suburbs for units are generally the ones closest to employment, transport, cafés and nightlife. Parks and schools might also feature, but not as prominently. Remember that the typical unit occupier will not be a large family.

Most importantly, you want a council that is ideally opposed to further densification. The whole idea is you don’t want extra stock to pop up overnight adding to supply.

Note that there are suburbs on city outskirts or in regional markets that have low unit counts. This could be interpreted as low supply. But for prices to take off, you also need strong demand. And if demand is strong for units there’s no easier place for them to pop up than in areas where there is still room to put them. It won’t take long for devil-opers to ruin that market for you.

What to look for in a suburb when buying units

• Proximity to the amenities that suit singles and young couples

• Demand that comfortably exceeds supply

• A restrictive local council development policy

• Development has already maxed out

• Units are old (higher LAR)

• Units are expensive

(higher LAR)

Picking the right unit

Most unit complexes are constructed in built-up areas. This means noise is a problem. You do not want a unit on a main road or next to a railway line.

You want the smallest number of units in the complex to improve scarcity factor and reduce competition with other landlords in the complex.

As a general rule, the higher the level your units is on, the better. However, in a three-storey walk-up without lifts, the lower the level, the better.

A unit within the complex that has views and doesn’t face a main road is preferred. A north- or east-facing aspect is ideal – that’s the direction the main balcony faces. And multiple balconies are better than one, especially if they face different directions.

Facilities such as pools and gyms are a waste. Strata fees are much higher to maintain them and they rarely get used anyway. However, extra expense towards improved security, a better lift and visual appeal from the curb, such as a simple garden, is a plus.

Extra visitor parking spaces come in handy. An extra space for every half a dozen or so units would be good.

Fees and rules

On-going fees for units are called strata fees, which cover upkeep of common areas and building insurance. Owning a house, you’d pay your own building insurance.

Check if the strata sinking fund has been emptied recently, or if there is some fat in the account.

Council rates are applicable to both houses and units, but the rates for a unit are much lower than for a house.

When living in a unit complex, the residents (your tenants) must abide by a unique set of by-laws peculiar to each complex. The policy towards pets in particular could be a deal breaker for some potential tenants.

Voting at an annual owners meeting will determine what happens concerning issues that pop up. Whatever issues arise will probably not go your way. Extra control

is a plus for owning houses.

1-bedder vs 2-bedder

For a long while now, one-bedroom units have been frowned upon. However, there is a growing demographic of lone occupier households.

Many older apartments may not have any one-bedroom units. This might represent an opportunity if there is strong demand in the area from singles.

However, for most markets, a two-bedroom unit appeals to a wider tenant pool and should be an investor’s default choice.

Off-The-Plan

When an investor buys off-the-plan, they’re taking a risk. Instead of seeing the actual state of the property, you have to imagine what it will be like and hope it turns out that way.

In return for the additional risk, the increased return is capital growth during the construction phase, when you don’t have to pay interest on a mortgage.

The problem is that many developers will not agree to a price that is at today’s standards. Some even factor in some capital growth eliminating the only appeal to investors. The big lure is that the property is new. But that will fade pretty quickly after settlement.

For an off-the-plan strategy to work, you need to have the longest possible settlement period, ideally in the middle of a property boom for the area.

What to look for when buying units

• 2 over-sized bedrooms 2 bathrooms

• An internal laundry

• High ceilings

• Ducted A/C with living area and bedroom zones

• Built in wardrobes

• Internal storage space, such as a closet and more secure storage in the garage/car park

• All the latest appliances and top quality finishes

• As much floor space as possible - anything over 100sq metres, not including the parking space, is great

Some of the stats may need an explanation. The DSR+ is the demand to supply ratio. This is a score out of 100. The higher the DSR, the more pressure there is on prices to rise. The DSR+ consists of 17 different indicators. Some of these indicators are also shown in the table.

Some of the stats may need an explanation. The DSR+ is the demand to supply ratio. This is a score out of 100. The higher the DSR, the more pressure there is on prices to rise. The DSR+ consists of 17 different indicators. Some of these indicators are also shown in the table.

The DOM is Days on Market, a reflection of how long it typically takes to sell.

The discount is the difference between the original asking price and the eventual sale price as a percentage.

The SOM% is the percentage of Stock on Market.

The higher this figure, the more supply there is – bad.

The MCT is a score out of 100 for the Market Cycle Timing. This is the likelihood the market is in the perfect stage of its property cycle for growth. The higher the number the better the market is.

The REP is the Ripple Effect Potential. This is a measure of the growth in neighbouring markets recently that might flow over into the target market.

As you can see, all these figures are quite poor for the markets listed, which is why the DSR+ is so low.