Major banks predict 14% house price drop. Really! | Property Insiders [Video]

In the past week, three of our four major banks have changed their outlook for house prices and are now predicting the biggest housing crash in decades.

Will they be right?

Economists at Commonwealth Bank and National Australia Bank are forecasting house prices to fall by 10% next year and Westpac forecast house price falls of 7% in 2023 and a further 5% in 2024.

The forecasts are predicated on the assumption that the Reserve Bank will begin raising interest rates later this year and housing will be “collateral damage in the RBA’s efforts to keep inflation on target in the medium term.

But how likely are these forecasts to come about?

That’s one of the topics I’m going to discuss today with Australia’s leading housing economist, Dr. Andrew Wilson chief economist of My Housing Market.

Banks forecast housing crash

The Australian banks don’t have a good track record of housing market forecasts.

I remember two years ago, in March 2020, when the same economists who are making these let’s call them “interesting” predictions today, similarly predicted a double-digit fall in house prices to occur then, and that didn’t eventuate.

They underestimated the strength and resilience of the housing markets.

This time last year the same economists were late to the party and only after our property markets turned the corner almost 6 months earlier, they realised what was really happening on the ground and forecast strong price growth for 2021.

However, once again they underestimated the strength of our housing markets and the strong price growth that ensued.

But if price rises house prices fall by the amounts predicted this time around, which will make it the biggest housing downturn in modern history.

While we have seen various segments of the housing market suffer significant price falls, we haven’t seen the overall Australian housing market crash like these economists are predicting.

Dr. Wilson, chief economist of My Housing Market explains:

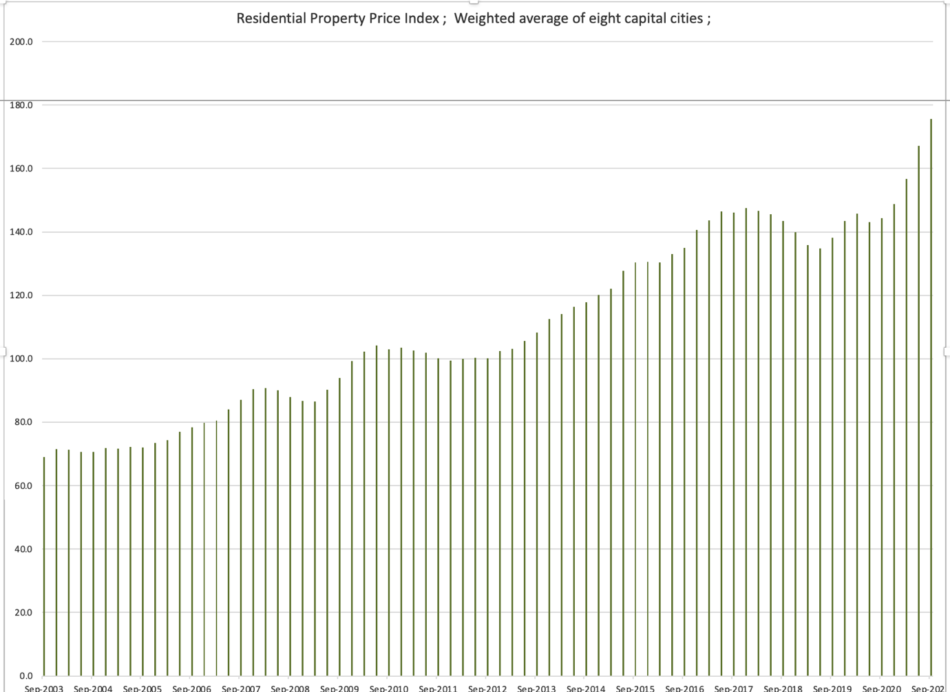

“The last time property took a downward turn was in 2018, when Australian house prices plunged by about 5 per cent overall.

It drove headlines like: “Prices fall at the fastest rate in 30 years”.

Prices also fell 4.8 per cent in 2011 after a period of post-global financial crisis rate rises from the Reserve Bank.

Those falls pale in comparison to what banks now predict.

They are quite remarkable forecasts.

Historically we’ve only had three years of falling prices since 1987.

Why would house prices fall?

Let’s be clear… the Reserve Bank doesn’t want the housing markets to crash.

It wants that about as much as it wants another strain of coronavirus.

Currently, Reserve Bank interest rates are low in order to bolster the economy and stimulate inflation and wages growth.

Once the Reserve Bank believes inflation is comfortably and consistently within its desired band of 2 -3% and unemployment is low enough to cause significant wages growth, then the RBA will slowly raise its interest rates for stimulatory levels to neutral levels.

Of course, there is some conjecture as to how high a neutral interest rate is, but considering the general level of Australian household debt, is unlikely to require a big rise in rates.

There is no reason for the Reserve Bank to raise rates sufficiently high to create a recession or a housing market crash.

While falling interest rates increase borrowing power and stimulate higher house prices, historical data shows it takes time for the rising interest rates to drive lower price growth.

Dr. Wilson explains:

“When we see house price reductions it only comes after a sustained period of higher rates.

The falls tend to be quite moderate.

Prices usually rise faster with lower rates than they fall with higher rates.”

Why home prices won’t crash

While falling interest rates create extra borrowing capacity and therefore increase housing affordability, rising interest rates do not necessarily cause house prices to fall.

While some commentators are concerned rising rates will cause mortgage defaults there are a number of reasons why this is unlikely to occur:

-

In general, Australian households are richer than they ever have been and have more equity in their homes because of our property boom.

-

Banks’ stringent lending criteria have only ensured they have only been lending to borrowers who could withstand a 2 or 3% rise in interest rates.

-

Many Aussie households have taken advantage of the current low-interest-rate environment and are three or four months ahead in their mortgage payments.

-

Our economy is bounding along and unemployment levels are low and with the prospect of wages rising ahead, most households should not feel mortgage stress.

US inflation at 40-year high: Will Australia follow?

Last week the United States announced its official inflation figure jumped 7.5 per cent in the last year, the largest spike since 1982.

A rise in inflation was expected, but this was higher than most economists anticipated, and the US Federal Reserve has already flagged interest rate hikes to cool rising prices.

Of course, inflation has been rising globally, with many central banks raising rates or at least flagging future rate rises.

The Reserve Bank of Australia (RBA) is one of the few central banks brushing off inflation fears, insisting Australia’s economy is in a different position.

So, will we follow the US’s lead with a major jump in prices?

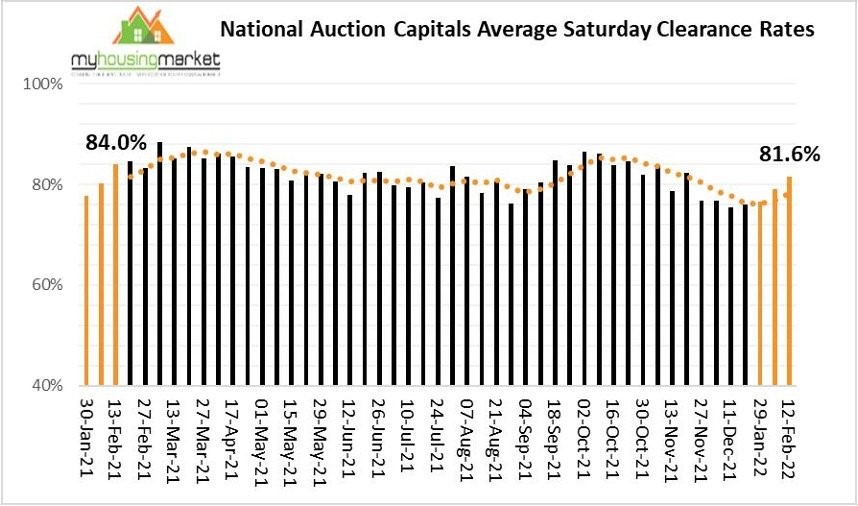

Weekend Auction results

Our national property markets produced another big weekend of early season auction activity with buyers and sellers clearly on the rise.

The Melbourne and Sydney markets consolidated the previous weekends’ strong results with both markets in revival mode with clearance rates the highest reported since last spring.

The national auction market reported a clearance rate of 81.6% at the weekend which was higher than the 79.1% reported over the previous weekend but lower than 84.0% recorded over the same weekend last year.

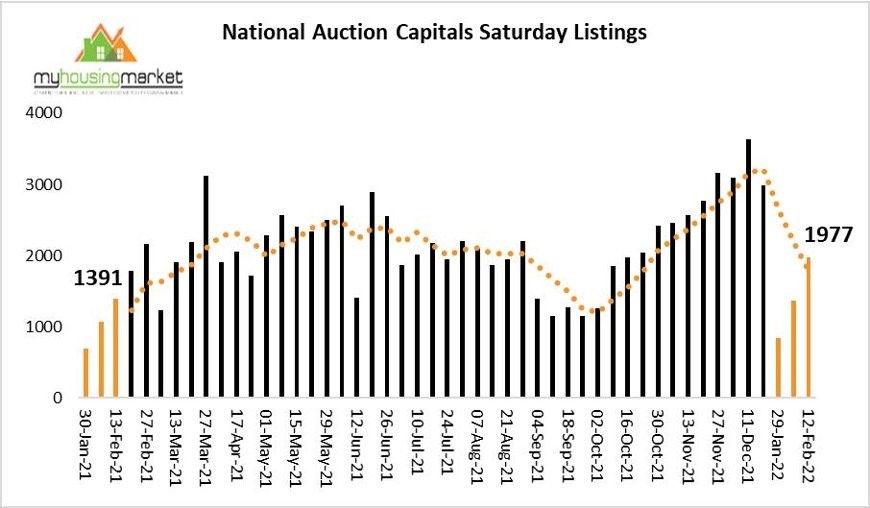

National auction numbers were significantly higher again at the weekend as the early season market gathers momentum.

1977 auctions were listed for auction compared to the previous weekend’s 1362 and well ahead of the reported 1391 the same weekend last year.

The national weekend auction market produced another strong February result despite a wave of listings challenging sellers.

Higher buyer and seller activity is set to continue for the rest of the month with housing markets clearly strengthening overall.

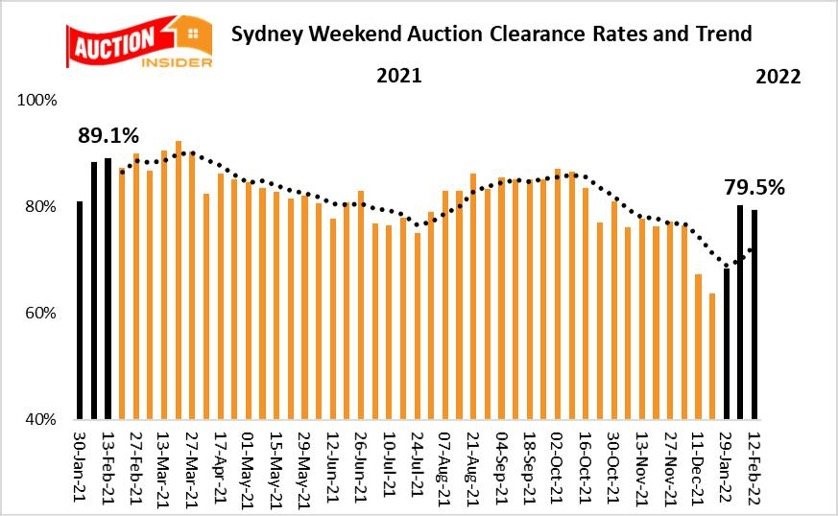

The Sydney auction market

Sydney has reported another strong result following last weekend’s boomtime clearance rate.

The local market continues to track at its highest levels since last October despite a wave of early season listings.

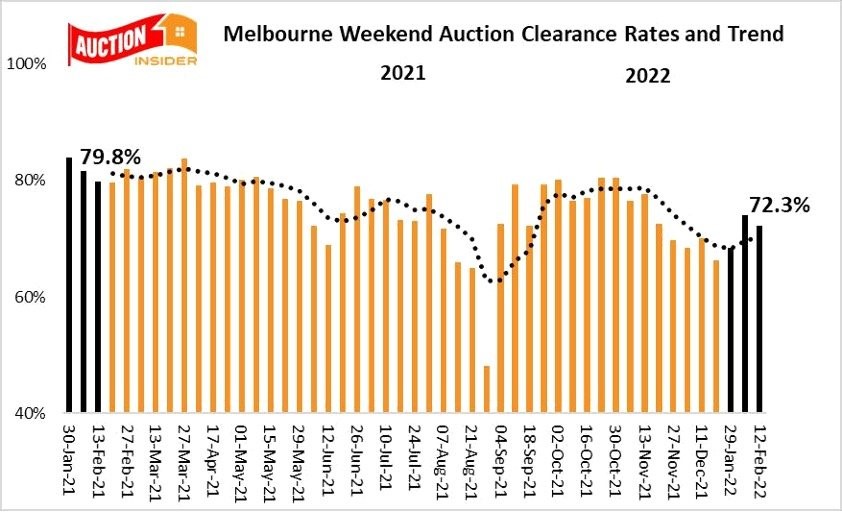

Solid Melbourne Market Steady Despite Listings Rise

The Melbourne weekend home auction market continues to produce encouraging results for early season sellers with buyers engaging the market in solid numbers despite covid distractions

Melbourne reported a clearance rate of 72.3% on Saturday which was lower than last weekend’s 74.0% and below the 79.8% recorded over the same weekend last year.

888 homes were reported listed for auction at the weekend which was predictably well above last weekend’s 491 but also significantly higher than the 698 auctioned over the same weekend last year.

Melbourne recorded a median price of $1,090,000 for houses sold at auction at the weekend which was higher than last weekend’s $914,500 and 9.8% higher than the $992,000 recorded over the same weekend last year.

..........................................................

Michael Yardney is a director of Metropole Property Strategists, which creates wealth for its clients through independent, unbiased property advice and advocacy. He is a best-selling author, one of Australia’s leading experts in wealth creation through property and writes the Property Update blog and hosts the popular Michael Yardney Podcast.

Michael Yardney is a director of Metropole Property Strategists, which creates wealth for its clients through independent, unbiased property advice and advocacy. He is a best-selling author, one of Australia’s leading experts in wealth creation through property and writes the Property Update blog and hosts the popular Michael Yardney Podcast.

To read more articles by Michael Yardney, click here