Developing a duplex is a far more complex endeavour than popping some tenants into a run-of-the-mill property. But as you’ll see, preparation and risk management will make the process far less daunting.

And for all that hard work, the rewards can be significant.

Here, we’ll take you step by step through a duplex development process, from a budding idea to the day you hold the keys in your hands.

STEP 1: Why should you develop?

Initially, you should stay on the starting block until you decide whether it’s feasible for you to undertake a development at all.

Ask yourself what you will do with your duplex once it’s complete. This is a foundation step that will determine your borrowing power and the feasibility of the project.

Your options are as follows:

• Rent out both units

• Sell both

• Sell one; rent the other

• Sell or rent one; live in the other

“Duplexes are a sophisticated way of building growth into the property, rather than waiting years to see it,” says Lloyd Edge, director of Aus Property Professionals.

“On completion of the build, whether it’s six, eight or 12 months, you can then take some equity out of that property and go and buy another property immediately.”

If you’re after cash flow, a duplex provides a dual income for the cost of a single piece of land.

As an example, a three-bedroom home in Palm Beach on Queensland’s Gold Coast currently rents for $650 per week. Four streets away, a three-bedroom duplex earns $550 per unit. That’s $1,100 per week combined – $450 more than the standalone home.

STEP 2: Is it financially safe?

Once you’ve settled on a strategy, you need to know if you can afford to do it.

According to Andrew Fawell, CEO of Beller Group, finances can be an area where would-be developers can easily come unstuck.

“The financing arrangement for developing is completely different to buying a standard investment property. There’s a lot more risk, and a lot of extra costs and potential problems,” he says.

Fawell says an experienced financier who deals with development loans every day will be able to provide a worst-case scenario to minimise your risk.

“The financing arrangement for developing is completely different… There’s a lot more risk”

“A lot can happen while you’re waiting for approval,” says Fawell. “Prices can change, rents can change, banks can change their criteria. You need to have realistic expectations of the feasibility of the project.”

A qualified development mortgage broker will be able to determine the best structure for your loan to maximise your tax benefits, calculate any GST payable and account for associated costs.

And there are plenty of those. Beyond land and construction costs, there are also legal fees, council fees, architects’ and town planner fees; headworks costs, soil reports, permits, and interest payments – to name just a few.

Fawell explains that lenders are wary of development loans and will need to know you can make a 20% profit on the deal before they’ll sign you up. Lenders will also factor in a buffer to protect themselves – and you’d be wise to add your own contingency plan into your finances as well.

If your finances are looking promising, it’s time to start hunting for a location that fits your borrowing budget.

STEP 3: Lock in a location

Finding a good spot on the map for your development is familiar territory in lots of ways. Essentially you’re looking for the pillars of growth that underpin any great investment property. These include proximity to major employment hubs and cities, strong infrastructure, population growth, rental demand, and local schools, shopping centres and entertainment facilities.

But there’s an added layer of complexity, Edge says. He suggests looking for flat blocks to keep costs down, and diligently checking the zoning of the lots. That includes any future rezoning plans as well. Council regulations vary, so it’s important to check each and every time – even if two lots are only a couple of streets apart.

STEP 4: Do a feasibility study

A feasibility study might seem tedious, but it’s the crucial step that determines whether you’ll earn big bucks or end up in hot water.

It takes into account all the costs involved, from land purchase through to completion of the build, and selling fees and taxes. When calculated against the expected sale price, you’ll see if the project is feasible, and worth doing for the profit.

“To plug in all the figures, you’ll need to get quotes from builders, who can give you an estimate of the build based on a survey plan, and then contact the local council for all the associated costs like rates and water,” Edge says.

Your finance broker will be able to help you with professional service costs like those of lawyers and quantity surveyors.

If the numbers prove that:

• the area meets your strategy in terms of expected capital growth or yield;

• the land meets development zoning regulations;

• duplexes are selling and renting well in the suburb;

• it’s within your borrowing power, including contingency funds;

• the market is unlikely to experience a significant downward change during the course of the build; then it’s time to go back to your broker and finalise your development loan.

STEP 5: Find a reliable builder

Paul Bieg, company director of Duplex Invest, says it pays to shop around and look beyond the major builders.

“The bigger builders have their fancy display homes and generally have a very good reputation, but you might pay 10–20% extra for that safety net,” says Bieg.

“There are other builders that you might not have heard of, who actually often work as subcontractors for the big companies, who don’t have all the bells and whistles but will come in better for your budget.”

Bieg says the best way to gauge a good builder is to ask to see some of their current projects.

“If they come back and say they don't have any clients that are prepared to talk to you, don’t touch them,” he says.

He also suggests using property forums and online searches for reviews.

Building companies generally have their own in-house architect or drafts person who can draw up a design for your block, or you can source your own architect.

Have your architect double-check the zoning laws, setback allowances and any other block-specific factors like retaining walls with the local council or town planner before they draw up the plans.

“Never assume that your builder or drafts person knows the details of what’s permitted on your particular block. It changes all the time,” Bieg says.

Building companies can also take care of the demolition of an existing property, as well as all the landscaping, so that you get a turnkey-ready duplex on the one contract.

Bieg suggests having a professional go over your construction contract before you sign it, even though it will cost a little extra. “Even a fixed-price contract can have some fine print saying that it’s subject to finding rock, or adequate facilities being connected.”

He also recommends ensuring a completion date is included in the contract and that the builders have accounted for potential delays, like weather or employee shortages.

STEP 6: Submit a development application

Once you have your finances sorted, your builder locked in and your floor plans in hand, you can submit your development application to the local council for approval.

At this point, vigilance is key. If the council discovers a problem with your application, they’ll send it back immediately. The more issues you have, the longer your approval will take, which can be costly.

“Never let things go on, because you need to make sure it stays on track so it’s completed on time”

To stay out of trouble, Bieg suggests using a planner or certifier to put the development application together.

“It might add an extra $2,000–$5,000 to the project, but it could save you time and money by avoiding all the delays,” he explains.

Even if all goes well with the application, councils can take several months to give their stamp of approval.

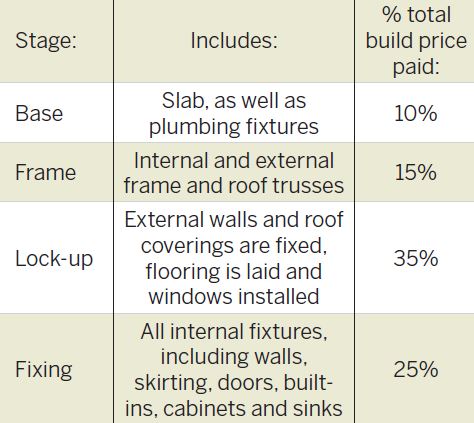

STEP 7: Begin construction

The day the builder breaks ground is an exciting one. Buildings are constructed in stages, with payment occurring after completion and approval of each stage.

As a guide, Consumer Affairs Victoria says building phases follow this outline:

A straightforward build like a duplex probably doesn’t warrant a project manager, Bieg says. “Your average investor can manage it themselves simply by going out there once a week and having a look around and keeping an eye on the contract.”

However, if the timeframe for completion of the next stage is blowing out, he says it’s time to ask some questions. “Never let things go on, because you need to make sure it stays on track so it’s completed on time.”

STEP 8: Handover and defect checks

Even more exciting than the first day of construction is the day the keys are handed over. But the work doesn’t end there.

A building inspector must carry out a full inspection and identify any issues or potential problems. The builder must resolve all the defects before the final payment is made.

Once the build is finished to your satisfaction and meets the terms of the contract, a building inspector will draw up a certificate of completion or occupancy permit.

Builders offer a maintenance period after handover – generally around four months – to fix any further problems that pop up.

“Even if it's something small, like the grout around the bath looking a bit poor, submit it to the builder in a report,” says Bieg. “If the builder gives you hassles, go to the relevant body in your state or territory, or the Master Builders Association.”

STEP 9: Fulfil your strategy

Along the journey, employ the services of a reputable local agent to handle the marketing of your new dwellings.

They’ll be able to help presell the units if that’s part of your strategy, have them ready for sale upon completion, or have tenants lined up to move in.

And if you’re like most successful developers, you’ll be chasing the next promising project before the ink has even had a chance to dry.

PEREGIAN SPRINGS DUPLEX

PEREGIAN SPRINGS DUPLEX

Location: Peregian Springs, Sunshine Coast

Purchase price: $305,000

Build cost: $488,350

Current dwelling value: $920,000

Total rental return: $900 per week

Approx equity: $126,650

CASE STUDY 1

TWO DEVELOPMENTS GENERATE $260,000 EQUITY

Overseeing two duplex builds at the same time on the Sunshine Coast generated a healthy six-figure profit for this investor.

Property investor Milly Brigden braved two simultaneous duplex builds on the Sunshine Coast, Queensland, completing construction of both in 2016.

Milly says she chose the Sunshine Coast because of its rapidly growing infrastructure and record-low vacancy rates. “There are new roads, new schools, a new hospital and a new university,” Milly explains. “The demographic has changed from mainly retirees to younger professionals and families that work remotely, or commute.”

Her first duplex is located in a premium new estate in Peregian Springs. Milly says that while most homes in the area boast four or five bedrooms, she chose to create a more affordable alternative for the market by building a three-bedroom, double-storey home.

Similarly, Milly chose to challenge the market in Bli Bli, the location of her second development, by building a three-bedroom, low-set duplex.

Similarly, Milly chose to challenge the market in Bli Bli, the location of her second development, by building a three-bedroom, low-set duplex.

“It has a lovely position in the estate with a great aspect, and this type of dwelling again provides an alternative for the couple or families that don’t need or cannot afford the large four-bedroom homes.”

While the construction process was smooth for both developments, Milly did use other professionals to keep things on track.

“I hired a project manager who had experience in these types of DA approvals”

“I hired a project manager who had experience in these types of DA approvals,” she explains. “They know what they’re doing and can get it done a lot faster than me!”

Milly, who founded Property Investor Solutions in 2007, is currently renting the properties out. Her strategy is to manufacture quick equity and cash flow through small developments, and hold for capital growth. The developments have earned Milly an equity gain of around $130,000 each.

Based on total purchase price, they are each returning a gross rental yield of approximately 6%, which Milly is very happy with.

Based on total purchase price, they are each returning a gross rental yield of approximately 6%, which Milly is very happy with.

“I can’t wait to get my teeth into the next one!”

“I am planning on doing a small land subdivision to manufacture even more equity,” she says. “I can’t wait to get my teeth into the next one!”

BLI BLI DUPLEX

Location: Bli Bli, Sunshine Coast

Purchase price: $308,500

Build cost: $413,000

Current dwelling value: $860,000

Total rental return: $860 per week

Approx equity: $138,500

CASE STUDY 2

TRIPLEX TRIUMPHS IN SUSTAINABILITY

Experienced investor Alice Joy and her fiancé, Tibor, are on track to earn almost $600,000 in capital gain with their Newcastle triplex venture.

THE DEVELOPMENT

Location: New Lambton, Newcastle

Purchase price: $429,000 Build cost: $775,000

Current value: $600,000 per unit

Rental return: $530–$550 Approx equity: $596,000

For the six months prior to purchasing the land, the couple attended every Saturday open home in the local area, building relationships with sellers’ agents and investigating buyer demand.

“We read the council’s LEP and spoke to local planners and architects about what developments were successful in the area,” Alice says.

They settled on an R2-zoned lot in New Lambton which had an existing house. Instead of building a granny flat at the back, they checked that the frontage was wide enough for a triplex.

“Duplex resales weren’t significantly higher, so we decided to maximise the site and build a triplex,” Alice says. “We had just enough space.”

Big believers in sustainability, Alice and Tibor decided not to demolish the original house. Instead, they bought and subdivided a large block in the Hunter Valley with a 1900s cottage, which is the New Lambton building’s new home.

“We cut the house in half, and moved them into the backyard in the middle of the night”

“We cut the house in half, and moved them into the backyard in the middle of the night”

We cut the house in half, and moved them into the backyard in the middle of the night. It was a tense half-hour trying to reverse the house down the driveway!” she laughs.

Alice, who started Living Joy Property Development in 2012, says they designed the units to integrate natural elements and promote energy efficiency. They included raked ceilings to maximise the feeling of space, kept the beautiful trees in the front and diligently worked the plans so that the living areas and courtyards faced north.

To deal with construction issues quickly, Alice and her build team held regular on-site meetings. She also had to negotiate with the local council to allow a visitor parking space on the land.

“It took a while, but with our logic and a report from a traffic engineer that our ‘gun-barrel’ park solution complied with the rules, it was approved,” says Alice.

“Don’t be afraid to workshop solutions with your builder and consultant team, even if you’re not an expert,” she adds. “It’s your project, and nobody will ever care as much as you!”

The units produce a gross rental yield of approximately 4.8% and a whopping $596,000 in equity.

ALICE’S TOP 5 TIPS FOR SUCCESS

1. Remember that no project is perfect, and that you’ll need to be flexible and adaptable during the course of the development.

1. Remember that no project is perfect, and that you’ll need to be flexible and adaptable during the course of the development.

2. Have regular site meetings to discuss the build progress and be part of the decision-making process.

3. It can be stressful at times, so make sure you use the expertise of your builder and professional team.

4. Use a reputable builder, even if they’re not the cheapest.

5. As a developer, you are literally shaping the future. Build ethically and make a profit in a way that you can be proud of.

BUILDING YOUR A-TEAM

An experienced team of professionals can keep you safe (and sane) during a development deal. You’ll need:

- A mortgage broker

- A property lawyer/solicitor

- An architect/draftsperson

- A quantity surveyor

- A reputable builder

THE BIG RISKS AND THEIR SOLUTIONS

Developments can be full of uncertainty, and very few go without a hitch. So what should you do if things don’t go as planned?

• Development application rejected. Depending on the issue, go back to the architect or town planner to find a workable solution. Limit errors by hiring a planner or certifier to compile your application for you.

• A blowout of building costs. Select a turnkey-ready, fixed-price contract so you know exactly what you’re paying for the whole build. Before you sign, check that the contract covers events like the removal of underground rock, so you’re not footing an unexpected bill.

• The builder goes belly-up. Your builder will have taken out domestic building insurance that will cover you if they go bust. Make sure to only choose reputable builders who can show you examples of their completed work, and have a solicitor check the contract.

• The market changes before the build is complete. If the value of the dwellings drops during construction, you’ll have to consult your mortgage broker and financial advisor to work out a solution. It might mean changing your strategy, such as renting out the property rather than selling. Due diligence and a contingency plan can avoid such circumstances.

HOW TO KNOW IF THE LOCATION IS RIGHT

• Look for flat blocks. “Sloping blocks are a lot more expensive because there's more site works, retaining walls and things like that, that cost money and take a lot of time,” says Lloyd Edge of Aus Property Professionals.

• Check zoning. “I’ve seen people buy a block of land and think they'll build a duplex on there, and then find out after the fact that it isn’t zoned for development,” says Edge.

“You’ve got to do your due diligence; check with council, check with the vendor, and

ask real estate agents a lot of questions.”

• Is it the right size? “Council requirements differ. Some may have to be a minimum of 600sqm to build a duplex, and in the next council area it’s only 500sqm,” Edge explains. “If you’re unsure, seek advice from a development company.”

• Is it the right price? If the lot doesn’t fit within your budget, move on. The more you spend, the higher your financial risk.