You’ve no doubt been taught to buy property with a high land component. The argument being, land appreciates while buildings depreciate. Nothing wrong with that concept, but then what should you buy?

- Houses instead of units?

- Houses on bigger blocks?

What’s important?

It’s got nothing to do with square metres, it’s to do with dollars.

“What are your dollars allocated to, land or liability?”

What you’re really after is the highest possible land to asset ratio or LAR for short.

Valuations

Let me just back up a bit. If you’ve ever seen a professional valuation report from a qualified valuer, you might have noticed that the value of a property is often broken up into land value and “improvements”. “Improvements” is the word they use for buildings that have been plonked on the land, improving the overall value of that address.

So, for example you might have a property valued at $500,000. The land might be valued at $200,000 and the improvements valued at $300,000.

The Land Asset Ratio in this example would be 40% since $200,000 is 40% of the total asset’s value of $500,000. This is an extremely low LAR.

Why do we look at it this way?

We want the highest proportion of our asset appreciating and the least amount depreciating. We want as much of our money going towards acquiring an asset and as little as possible going towards paying for a liability.

“An asset appreciates, e.g. land. A liability depreciates, e.g. a building.”

An example

Imagine property A is like the one I described: it’s worth $500,000 and has $200,000 worth of land so it has a 40% LAR.

-

Property A

- Year 0: $500k

- $200k land

- $300k building

- LAR = 40%

- Year 0: $500k

Now imagine property B is also worth $500,000 but the breakdown of land value to building value is different.

-

Property B

- Year 0: $500k

- $300k land

- $200k building

- LAR = 60%

- Year 0: $500k

In the case of property B, the land is worth $300,000. This means the LAR is 60%.

Two properties of the same total value, but property B has a higher Land Asset Ratio than property A. How is this possible? Well, property B might have a smaller house on it, or it might be an old house. Or it might have a bigger block or the block might be in a better location.

What happens?

Let’s see what happens to the values of these two properties over the next year assuming the following for both:

- Land appreciation = 10%

- Building depreciation = 2%

Imagine that land appreciates for both properties at the exact same rate and assume the buildings depreciate at the same rate too.

-

Property A

- Year 0: $500k

- $200k land

- $300k building

- LAR = 40%

- Year 1: $514k

- $220k land

- $294k building

- Total growth = 2.8% ($14k)

- New LAR = 42%

- Year 0: $500k

-

Property B

- Year 0: $500k

- $300k land

- $200k building

- Year 1: $526k

- $330k land

- $196k building

- Total growth = 5.2% ($26k)

- New LAR = 63%

- Year 0: $500k

After a year, property A’s land has grown by 10% from $200,000 to $220,000. The $300,000 building however, has depreciated by 2% from $300,000 to $294,000. So, a year later, the combined value of house and land for property A is $514,000.

Over the same timeframe, property B’s land also appreciated by 10%. It went from $300,000 to $330,000. And the building depreciated at the same rate of 2% to go from $200,000 to $196,000. The combined land and building value for property B is $526,000 after one year.

Property A has grown by 2.8% while property B has grown by 5.2%. Both started at the same value, both had the same land appreciation rate and the same building depreciation rate. The reason property B’s growth almost doubled property A’s growth is because B had a higher LAR than A.

Typical high LAR properties

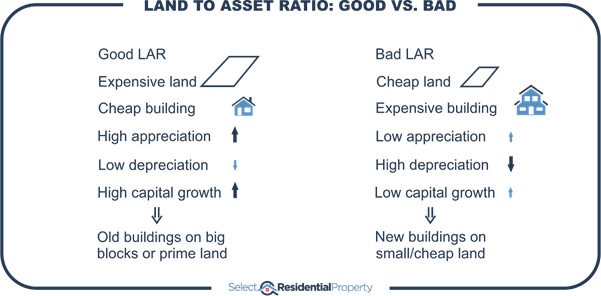

Older dwellings usually have higher LARs since they’ve already depreciated and lost much of their value. All that time they were depreciating, the land was appreciating. So, over time the LAR gets higher and higher. Older properties have typically higher LARs.

It makes sense therefore that newer properties typically have lower LARs. This is because much of the expense related to the property is in the building of it. Developers want to buy the cheapest land and add the most value to maximise profits. But this strategy minimises profits for investors. That’s why investors should never buy new if they’re after growth.

Oddly, some old units in exclusive areas actually have high LARs. Remember, it’s not the square metres that count, but the value of that tiny bit of land under the building compared to the overall value of the asset. That’s what matters.

Summary

....................................................................................

Jeremy Sheppard is head of research at DSRdata.com.au.

Jeremy Sheppard is head of research at DSRdata.com.au.

DSR data can be found on the YIP Top suburbs page.

Click Here to read more Expert Advice articles by Jeremy Sheppard

Disclaimer: while due care is taken, the viewpoints expressed by contributors do not necessarily reflect the opinions of Your Investment Property.