Firstly, I should clarify how to calculate the vacancy rate. Step 1 is to get a count of all the properties listed for rent, i.e. a count of vacancies. But some properties may mention they’re not available for rent until some future date. Those are excluded since technically they’re not vacant yet.

The number of “landlord-owned” properties in the market is then divided by the count of vacancies. That figure is then converted to a percentage. Note that not every property in a suburb is landlord owned (a.k.a. rentals).

Insight 1 – current average

The average vacancy rate Australia wide was over 2% as at the end of April 2021. But the average can be skewed higher by a handful of extremely high vacancy rates. This is where we would use the median instead – the middle vacancy rate. And the median was only 0.9% for the same month.

The following infographic is the Vacancy Rate context ruler for Docklands units in Melbourne’s CBD at the end of April 2021.

The vacancy rate is very high here at 5.31%.

In the top right you can see there were over 6,000 suburbs around Australia that had a measurable vacancy rate for April 2021.

Bottom right shows the maximum vacancy rate was 25%. Ouch!

In the middle top of the ruler, you can see the average at 2.07%.

The median vacancy rate is the middle property market when all are placed in order. You can see the median at the bottom of the chart at 0.9%.

From this infographic you can see that most property markets had a vacancy rate well under 3%. In fact, 75% had a vacancy rate less than about 2%. So, straight away we can say this was either a peculiar time of tight vacancy rates country-wide or 3% is not a good standard.

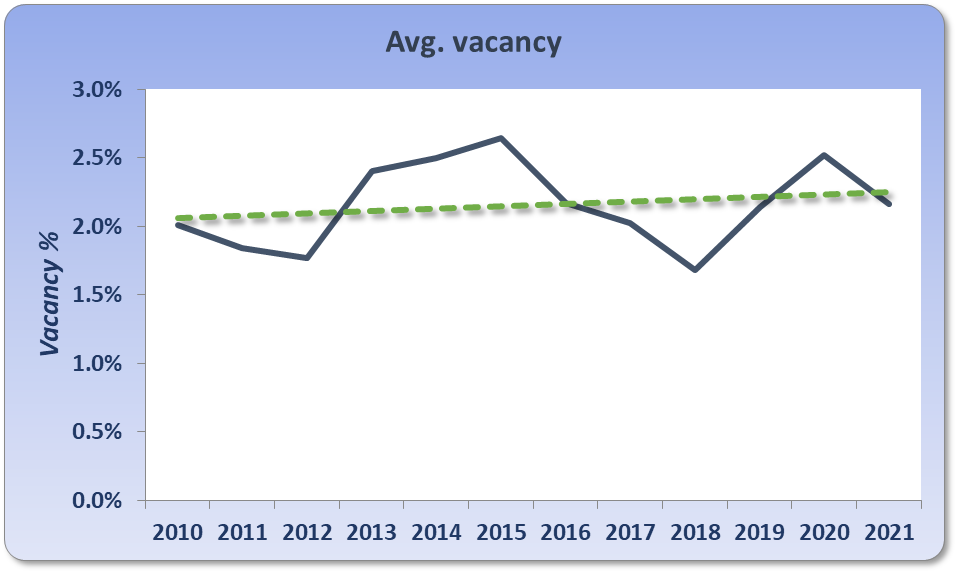

Insight 2 – historical average

Past vacancy rates…

This chart shows the change in the national vacancy rate since January 2010. It does move up and down a bit, but it’s only been above 2.5% once. It’s never really got close to 3% for any time in over a decade. And the trend line is closer to 2% than it is to 2.5%.

Insight 3 – houses vs units

The long-term average didn’t differ much between houses and units:

-

Houses 2.1%

-

Units 2.4%

You can see that the long-term average vacancy rate has been closer to 2% than to 3%.

Insight 4 – state vs. state

Different states have different real estate laws and may have different habits regarding listing properties for rent, so what about a break-down by state?

-

ACT 1.4

-

NSW 2.3

-

NT 1.8

-

QLD 2.5

-

SA 1.9

-

TAS 2.3

-

VIC 2.3

-

WA 2.1

Long-term there is some significant difference in each state’s vacancy rate. However, those figures for ACT and NT should be swallowed with a grain of salt. They’re very small markets so the figures could be a little less reliable than the larger states like NSW, VIC and QLD. The most populous states all have long-term averages around the low to mid 2% range.

Note that there wasn’t a single state with a long-term average vacancy rate of 3%.

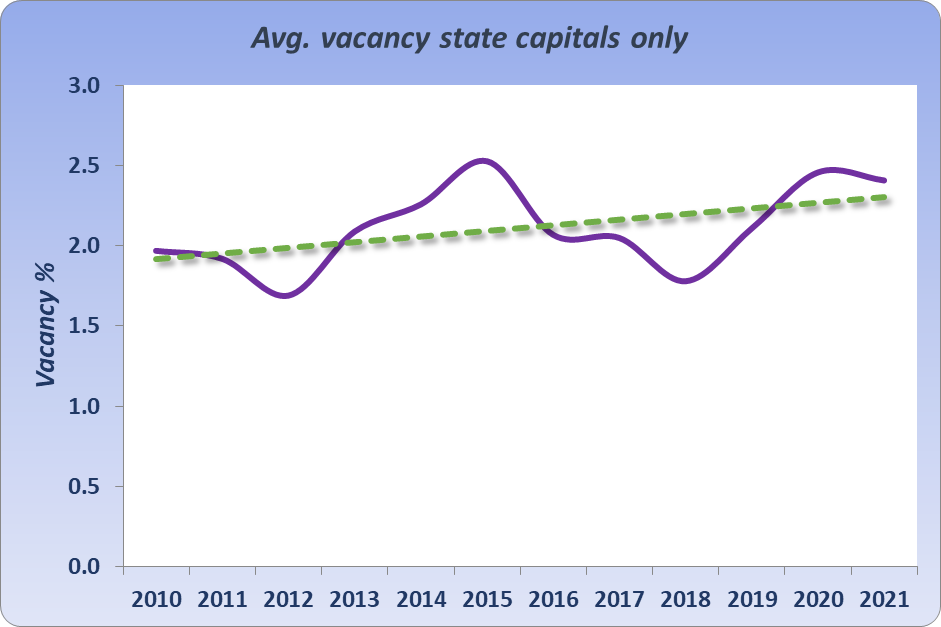

Insight 5 – capital cities

What if we eliminate all those weird markets in regional locations and focus on state capitals only?

There’s very little difference and the average still looks like around 2%.

Insight 6 – reliability

Sometimes the vacancy rate can get a little unreliable especially in small or thinly traded markets. Let’s eliminate all but the most reliable property market figures for vacancy. I removed suburbs from consideration if the volume of rentals was too low to be reliable.

The average vacancy rate didn’t change much. And it’s closer to 2% than ever.

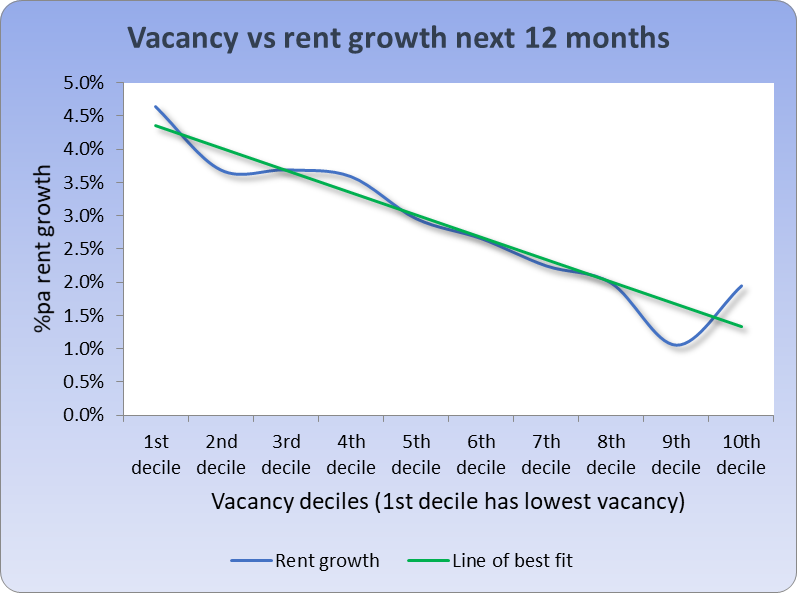

Insight 7 – rent growth

Perhaps this is an over-simplistic way of looking at what constitutes a “balanced” market. Perhaps our markets have been unbalanced for a long time. How else can we judge whether a market is balanced or not?

One thing I’ve noticed is that if vacancy rates are really low, there is pressure on tenants to get into properties. The property managers are aware of this and may mention a rental increase is possible to their landlords. As a result, the yields in the area start rising – especially if property prices are static.

So, how about examining cases where low vacancy rates start causing rents to rise? Rents will rise anyway though due to inflation. So, we need to assume that rental growth above 2.5% is a market in which vacancy rates are tight and therefore out of balance.

We can also assume that if rents are not growing by at least the rate of inflation, then vacancy rates are too high. The balance point will be where rents are growing at the same rate of inflation.

This chart shows the relationship between vacancy rates and the following 12 months of rent growth. I’ve split the vacancy rates into deciles. Each decile is a group containing 10% of all property markets. But the group each 10% fit in is determined by their vacancy rate.

The 1st decile to the left of the chart contains all markets that had a vacancy rate in the lowest 10% of all vacancy rates. The highest decile to the right is the nasty end with the highest vacancy rates in the country.

The first thing you notice is how high vacancy rates diminish your chances of getting any rental growth. And low vacancy rates increase the chance of rental growth. Nothing tremendously insightful there.

The green line is the line of best fit. It shows the relationship between vacancy rate and the following 12 months of rent growth is pretty close.

You can see that the green line passes through 2.5% rent growth at about the 7th decile. This means that rent is growing in line with inflation around the 7th decile. The 7th decile therefore represents a vacancy rate in balance.

The vacancy rate at the middle of the 7th decile is around 2%. It actually works out to be 1.98%.

Conclusion

There you have it, enough data insights to suggest that the true benchmark of a balanced vacancy rate should be 2%, not 3%. Property investors should be aiming at buying in markets where the vacancy rate is at most 2% and preferably as low as possible.

....................................................................................

Jeremy Sheppard is head of research at DSRdata.com.au.

Jeremy Sheppard is head of research at DSRdata.com.au.

DSR data can be found on the YIP Top suburbs page.

Click Here to read more Expert Advice articles by Jeremy Sheppard

Disclaimer: while due care is taken, the viewpoints expressed by contributors do not necessarily reflect the opinions of Your Investment Property.