When I was a novice property investor, I was told by experts to buy and never sell. I’ve made many memorable mistakes - “never sell” was one of the biggest. Since then, I’ve sold a dozen of my properties and I’m open to selling more if the numbers stack up.

Why selling is bad

There are huge costs involved in selling. And what are you supposed to do with the sale proceeds? There are even more costs if you want to buy again elsewhere. Moving equity around by “trading” property eats into profits.

But it’s not the only thing that eats into profits. Sometimes the other thing is worse.

Considerations

Each property needs to be examined case-by-case using these 2 costs:

Recycling cost

Recycling cost is the cost of firstly selling your property to release funds, and secondly, putting those funds elsewhere:

- Exit costs

- Re-entry costs

“Exit” costs are the costs to sell your property. They consist of:

- Capital gains tax

- Selling agent’s commission

- Legal fees

- Maybe clean-up costs or marketing too

After paying back the mortgage, you’re left with sale proceeds that can be re-invested elsewhere.

Using the sale proceeds to buy elsewhere comes with more costs. These are called “re-entry” costs. These consist of:

- Stamp duty

- Legal fees

- Inspection costs such as building, pest & strata

The combination of exit costs and re-entry costs total up to the recycling costs.

Opportunity cost

Opportunity cost is the difference between what an alternative investment could earn you and what your current investment could earn you.

For example, if your current investment property earned you $100,000 in capital gain over the next 3 years and an alternative grew by $150,000 then the opportunity cost would be $50,000. That’s assuming income and expenses were the same for both.

When should we sell?

The trigger to sell is when the forecast opportunity cost comfortably exceeds the estimated recycling cost. The concept is simple enough, but coming up with accurate figures is the tricky part.

Market cycles

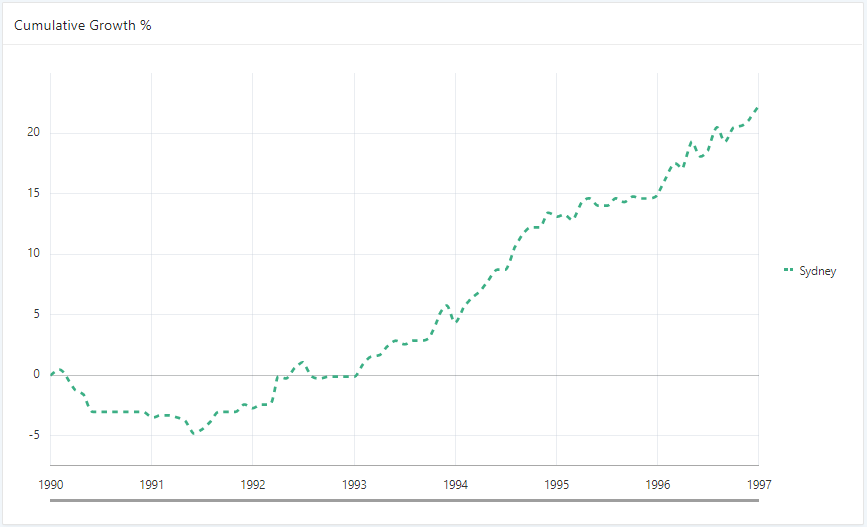

Yes, if you wait long enough, eventually more growth will come – next cycle. But some markets can remain depressed for a decade. Check this chart out for example.

The chart looks like there’s good growth, but it’s cumulative growth, not a growth rate. The growth rate was actually less than 3% per annum – not much more than inflation.

And it wasn’t a one-off for Sydney. There was an even bigger stretch of low single digit growth.

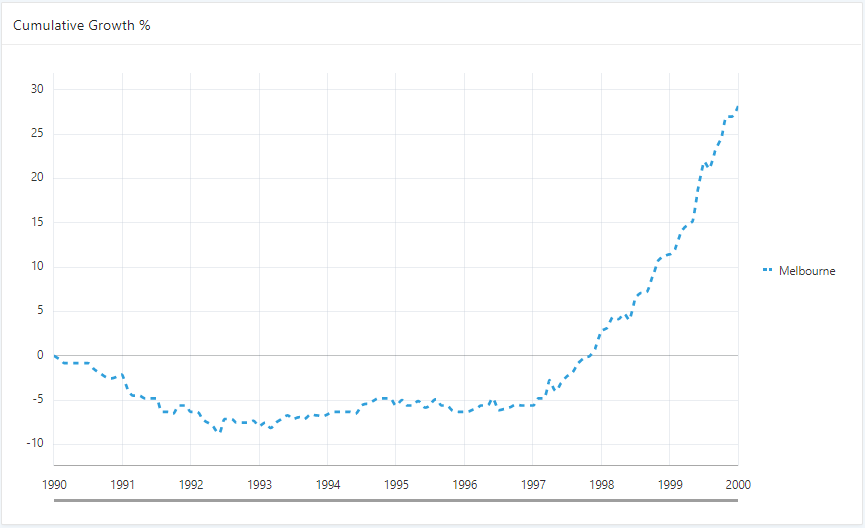

Here’s a stretch of 10 years of only 3% growth per annum. It started in 2004 and went to 2014.

But you can see in the chart a massive spike from 2009 to 2011 and another from about 2013. And this is crucial to the argument of why investors should sell. Markets don’t grow at a consistent rate. Instead, they have banging bursts followed by boring busts.

Melbourne had 3% growth per annum for the eleven years from 1989 to 2000.

We see the same thing again, a period of yawns followed by a period of yippie. And the yippie is short and sharp while the yawn, drags on.

Here’s Melbourne for the 5 years from 2011 to 2016.

The growth over this total time-frame was less than 3% per annum. Over 5 years, the growth totalled less than 16%. But the last year was pretty good.

And this is the same story for all these charts – very impressive growth for short periods, but over the total period shown on the chart, barely able to keep pace with inflation.

Are the reasons still there?

The 1st question everyone wants to know about a market dragging its feet, is whether it will start growing anytime soon?

Well, ask yourself this, why did you buy in that location in the first place? What were the reasons that attracted you to this location? Are those reasons still playing out or did you get it wrong?

Why hang on to a property if you’ve already discovered you got your research wrong?

Mistakes

Mistakes are the best learning experiences if we respond to them appropriately.

“It takes courage & humility to put your hand up and admit you made a mistake”

But once you do, you can take that learning into your research for the next purchase.

Perth vs Sydney example

One of the key arguments for trading properties as opposed to holding them long-term, is that growth happens in short thrusts followed by long busts.

Imagine it’s the middle of 2012 and you’re looking where to invest and you choose Perth instead of Sydney. At first it might have seemed to be a good pick with roughly 7% growth per annum for the first couple of years. But over the entire 5 years from 2012 to 2017, the difference between these two cities was a staggering 55%.

The opportunity cost of making the wrong decision in this case was quarter of a million dollars over only 5 years. This is not just a few properties in Perth versus a few in Sydney, this is the average for all properties in both cities.

What if an investor had bought in Perth a long time ago and had to pay significant capital gains tax? Surely in this case the capital gains tax would be so large that the selling costs would make recycling equity too costly.

Well, let’s assume the capital gain was equal to the entire value of the property. In other words, assume the investor bought their Perth property for 1 cent.

Perth median $460,000

Capital gain of $460,000

50% CGT discount for holding for more than 12 months = $230,000 taxable gain

There would be entry and exit costs the investor could claim to reduce that capital gain, the “cost base”, but let’s ignore those to make the case even more extreme.

Marginal tax rate of 45% = CGT payable of $103,500

Agent’s commission at 2% = $9,200

Legal fees $1,000

Total exit costs of $113,700

Assume the highest marginal tax rate of 45 cents in the dollar. Add the agent’s commission and legal fees. The total exit costs would have come to $114k. That’s enormous and we haven’t even considered re-entry costs such as stamp duty, legal fees and inspections:

Entry costs of about 5% of $575k = $28,750

Total recycling costs of $142,450

The Sydney median in mid-2012 was around $575k. Entry costs at 5% of a $575,000 property would total over $28k.

So, the total cost to recycle your equity with the highest imaginable capital gains tax liability would have been about $142k. Ouch!

Surely with such massive recycling costs, there’s no option but to hold. Well, the opportunity cost was over quarter of a million dollars.

4.6% growth in Perth median of $460k = $21,160

59.1% growth in Sydney median of $575k = $340,000

Opportunity cost = $318,840

After 5 years a Perth investor would have been better off by $176,390 if they recycled equity into Sydney.

The difference in growth between the two cities was so significant, that it’s unlikely any one of the hundreds of thousands of Perth investors wouldn’t have been better off in Sydney.

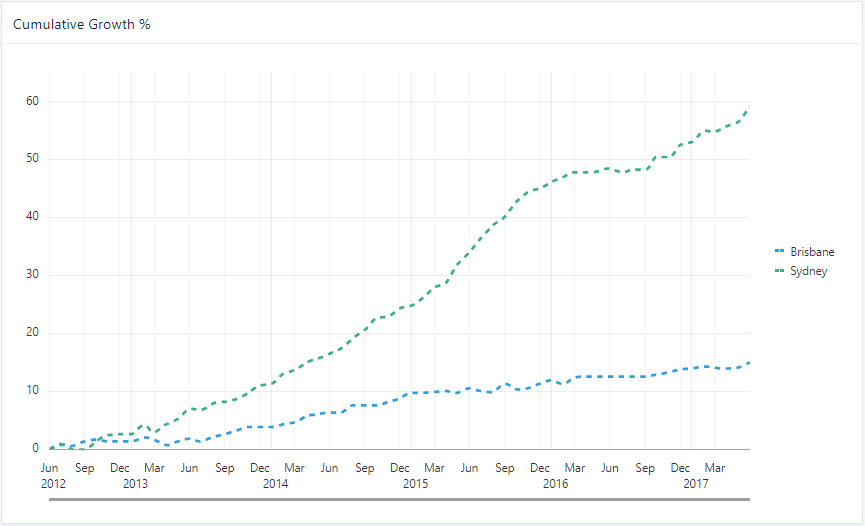

Brisbane vs Sydney example

Let’s have a look at Brisbane around the same time.

The difference in growth was not as severe in this comparison, only 44%. But it was still significant enough to give the vast majority of Brisbane property investors very little reason to hold onto a property in Brisbane instead of recycling their equity to Sydney instead.

There were about 350,000 property investors in Brisbane at the time. That represents about 12% of all Australian property investors. Investors in Darwin and Adelaide would have drawn the same conclusion – sell.

Add to that the Perth investors and we’re talking about more than 20% or 1 in 5 property investors should have sold. And this is looking at only one stretch of 5 years in Australian property growth.

Melbourne example

Here’s a difference of over 40% between Melbourne at the bottom and Perth & Brisbane at the top.

While Melbourne investors were holding on to low yielding negatively geared properties, investors in Perth and Brisbane were giggling.

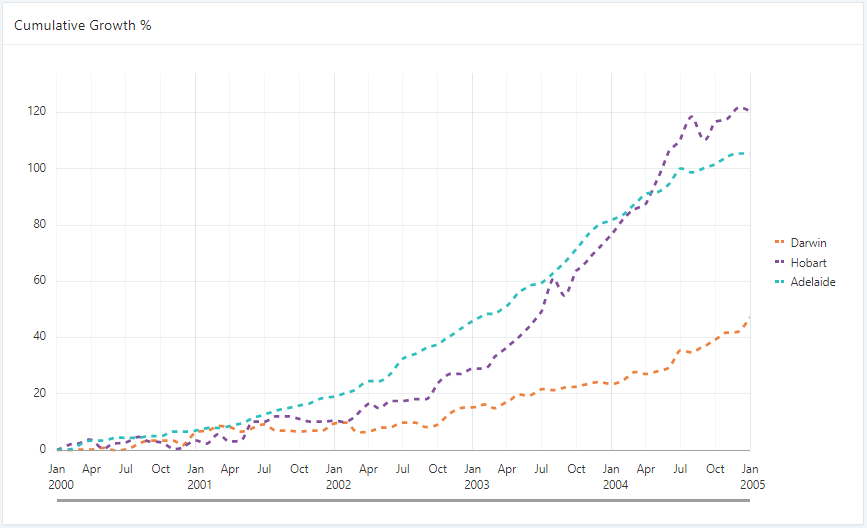

Darwin example

There’s a difference in growth of over 40% for the top markets of Hobart and Adelaide versus Darwin at the bottom.

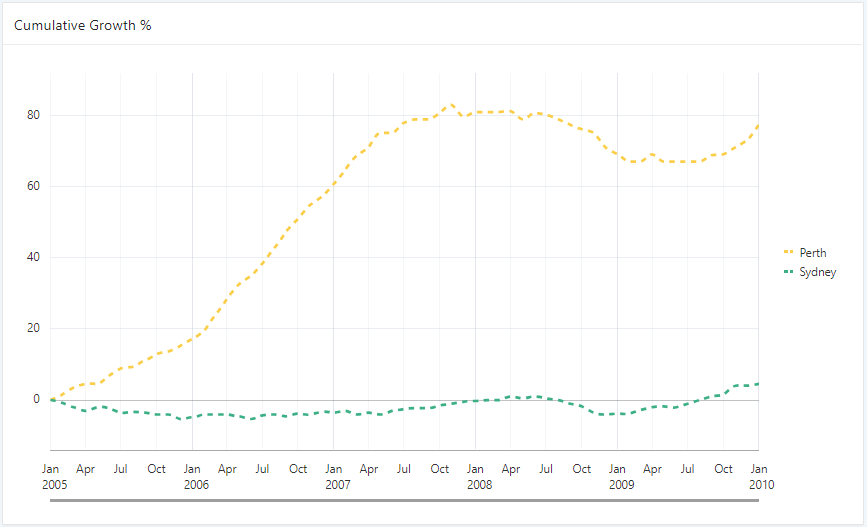

Sydney example

Here’s a 70% growth difference over 5 years between Perth and Sydney.

This was from 2005 to 2010.

It’s difficult to find a point any time in the last 25 years where there wasn’t a 5-year period where one state capital wasn’t outperforming another over that 5-year period by more than 30%.

“Investors should be looking for opportunities to recycle their equity on a regular basis”

Conclusion

There are definitely times you should sell your investment property. It’s when opportunity cost exceeds recycling cost by a comfortable margin.

And you can see from all the historical evidence, that it’s not a rare circumstance for an investor to find themselves in.

But, if you can never know where prices are heading, you can never estimate opportunity costs. In that case, it makes perfect sense to never sell.

So, make sure your advisor doesn’t say, “never sell”. It means they don’t have a good idea of where prices are heading.

....................................................................................

Jeremy Sheppard is head of research at DSRdata.com.au.

Jeremy Sheppard is head of research at DSRdata.com.au.

DSR data can be found on the YIP Top suburbs page.

Click Here to read more Expert Advice articles by Jeremy Sheppard

Disclaimer: while due care is taken, the viewpoints expressed by contributors do not necessarily reflect the opinions of Your Investment Property.