Introduction

If you chase after bargains you run away from capital growth. And capital growth is the fly’s eyes of property investing – nothing is more important.

If you make buying under market value a priority, you’ll be making capital growth harder to obtain. These strategies are polar opposites. I’ll explain why soon. But firstly:

Define terms

Cheap is just that – a low price. Just because it’s cheap doesn’t mean it’s under market value.

A discounted property is any property sold below the original asking price, which is most of them.

“It’s possible to buy at a discount and still pay above market value”

What investors think they should be pursuing, is a property under market value. e.g., paying $380k for a property believed to be worth $400k.

Valuing

The true value for a property is the price someone is willing to pay for it – it’s as simple as that. But that someone could be a poor negotiator, or the opposite, they could suffer from hepa-tight-arse.

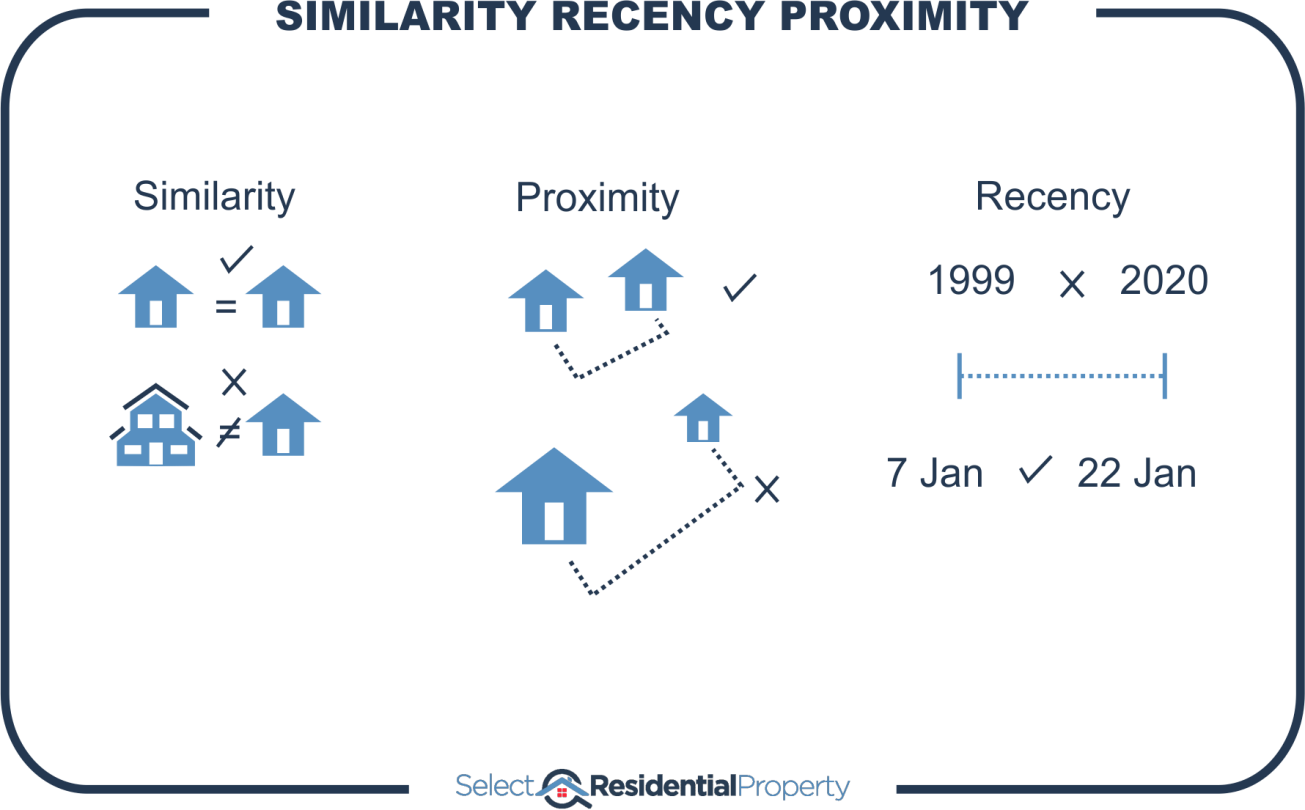

How does a professional property valuer do it?

Valuers compare recently sold properties in close proximity of similar nature and condition. Real estate agents will do the same thing. Potential buyers will do the same thing. However, everyone has a different opinion despite using the same technique because everyone is biased.

Who’s right?

You will never really know the true value. That brings us to the 1st problem with the approach of buying under market value, nobody really knows what market value is until the property has sold - and then we know precisely.

New value – what you paid for it

The new value of the property is what you just paid for it – not what you think it’s worth.

There’s no such thing as the under-market-value-flip or the discount-flip. You can’t buy a property for under market value and then sell it for market value in the next couple of months. The record of your purchase will be available to valuers, real estate agents, buyers and buyer’s advocates. Its new value is the price you just paid for it.

And you can’t refinance on the “new” value either. Your bank will probably refuse to get a valuation done on your newly purchased property. They’ll usually only entertain a new valuation at least 6 months after purchase and probably only if you tell them you’ve renovated.

There’s no such strategy as the discount-flip:

“Under market value is a strategy for novice investors who can’t find growth”

Not impossible

Now, having said all that, I don’t believe it’s impossible to buy a property for under market value. However, relying purely on that as a strategy is unprofitable. You need something else like: capital growth or renovation potential to make it worthwhile. And this leads us to the next problem with this approach…

Bad focus

If you’re focus is to buy under market value, you’ll be drawn to more negotiable sellers. You’ll discredit markets in which sellers are arrogant and staunchly reject your hepa-tight-arse offers. You’ll be drawn to markets where agents give you time and sellers carefully consider your offer.

The thing is,

“The best property markets for capital growth have the least negotiable sellers. The markets you’ll find negotiable sellers are the ones you want to avoid.”

Ironically, a seller’s market is the best one to buy in for an investor. A seller’s market is one in which selling is easy. You plonk your property on the market and suddenly every buyer and their cus’ turns up at the 1st open inspection. There’s a flurry of visits, some ridiculous offers, and it’s gone.

A seller’s market is one in which demand exceeds supply. Those are the markets investors should be interested in.

Conversely, a “buyer’s” market is one in which it’s easy to buy. You can take your pick from a huge range of stock. Agents greet you like they’ve been ship-wrecked on a deserted island.

Falling prices

Think about this: if everyone pays below market value, prices are dropping with every sale. So, every property that sells under market value is a nail in the coffin of your hopes for capital growth.

“The easier it is to get a bargain, the lower the demand is with respect to supply”

For every buyer who pays below market value, there is a blight on that market’s supply and demand equation.

The best markets for growth

It’s not until the majority of buyers are paying above market value, that you’ve found a market experiencing some capital growth. The more buyers there are paying above market value, the more capital growth is occurring.

“The best market to invest in, is the one where it’s impossible to buy under market value”

Some data

This is all theory, but what really sticks is evidence. I’ll use the Average Vendor Discount to compare markets with more potential for bargains against those with low potential for bargains.

The Average Vendor Discount is a metric we use to measure demand in property markets. We look at the price that a property was originally advertised for sale. Then we compare that price to the eventual sale price of the same property. We measure the difference in percentage terms which is called the Discount. We then calculate an average for all properties that sold in a suburb for a month.

At the time of making calculation, the average vendor discount Australia-wide was around 3%. The vast majority of property markets around the country had a discount of less than 7%. Anything above 10% was considered quite worrying. Anything less than 2% is excellent.

The higher the discount is, the lower the demand will be, but the more likelihood of finding a negotiable vendor. Keep in mind that a discount does not equal a bargain or a saving. Also, keep in mind that using a single metric to gauge demand and supply is extremely inaccurate.

Despite this, an analysis of discounts over the 10 years from 2010 to 2020 hints at how bad it might be to chase a bargain:

- High discount cases are suburbs with at least a discount of 10%

- Average discount for all suburbs in the analysis was 11.9%

- They experienced 8.8% total capital growth on average over the next 3 years

- Low discount cases are suburbs with a maximum discount of 2%

- Average discount for these suburbs was 0.7%

- They had 22.5% total capital growth on average over the next 3 years

- Totals

- Average savings gained buying in a high discount suburb instead of a low discount suburb was 11.2% (assumed)

- Capital growth lost buying in high discount suburb instead of a low discount suburb was 13.7%

- Therefore worse off by 2.5%

Within 3 years, bargain hunters would be worse off by 2.5% of their property’s value. The discount saved was overwhelmed by the inferior capital growth.

However, this is assuming the property was advertised at fair market value. But they never are. So, the discount savings in the calculations are greatly exaggerated. Bargain buyers would have been much worse off than 2.5%.

The data clearly shows that this strategy is a poor choice for investors to focus on.

Distressed sales

Examples:

- Mortgagee repossession

- Divorce settlement

- Deceased estate

- Bought elsewhere and it’s settling soon!

You might be thinking you’ll find one of these opportunities. But there’s a few things you should be aware of. Firstly, they’re not common, but investors looking for them are. But most importantly:

“There’s no such thing as a distressed sale in a hot market”

In a hot market, if you have to sell in a hurry, you can. There’s no hold up.

It’s easy to kick someone in the teeth when they’re on their knees. Personally, I don’t want that to be the basis for my successful portfolio. It’s not something that would make my mum proud.

Conclusion

Finding properties under market value is a lot harder than you think. There are legitimate success stories. But the general strategy opposes success.

“Every under-market opportunity is actually a kick in the capital growth groin”

This was topic #2 in Jeremy’s Expert Busting Series.

....................................................................................

Jeremy Sheppard is head of research at DSRdata.com.au.

Jeremy Sheppard is head of research at DSRdata.com.au.

DSR data can be found on the YIP Top suburbs page.

Click Here to read more Expert Advice articles by Jeremy Sheppard

Disclaimer: while due care is taken, the viewpoints expressed by contributors do not necessarily reflect the opinions of Your Investment Property.