Growth trumps cash-flow

Capital growth is the ant’s pants of property investing. The most successful investors are the ones who have found great growth locations, not the ones who have found great yield locations.

The equity you get from double-digit growth will make a 7% gross rental yield look virtually inconsequential. It’s not until you do the numbers and forward project that you see just how much better off you’ll be with a growth focus.

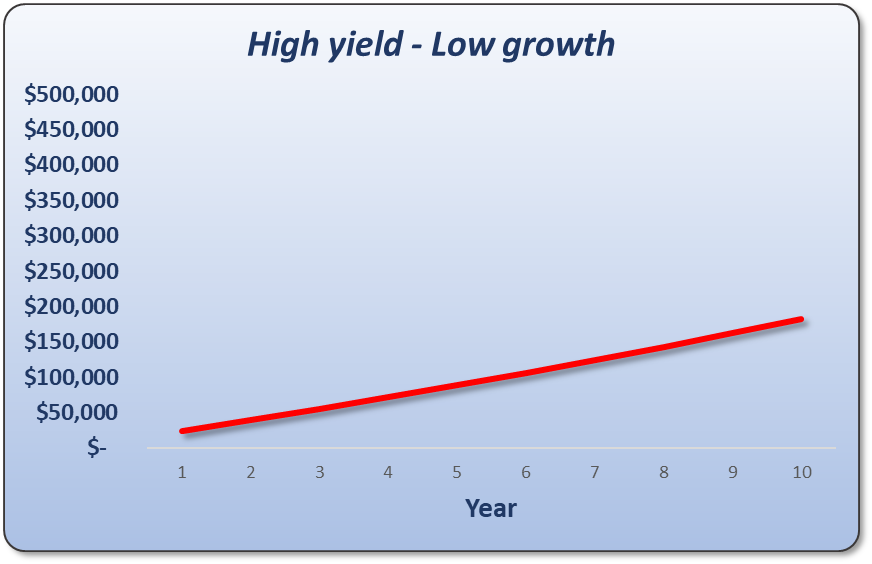

The following chart shows the total wealth created for a theoretical $500,000 property over 10 years with 7% gross rental yield and 3% capital growth per annum.

After 10 years there’s about $180,000 of equity and cash-flow combined.

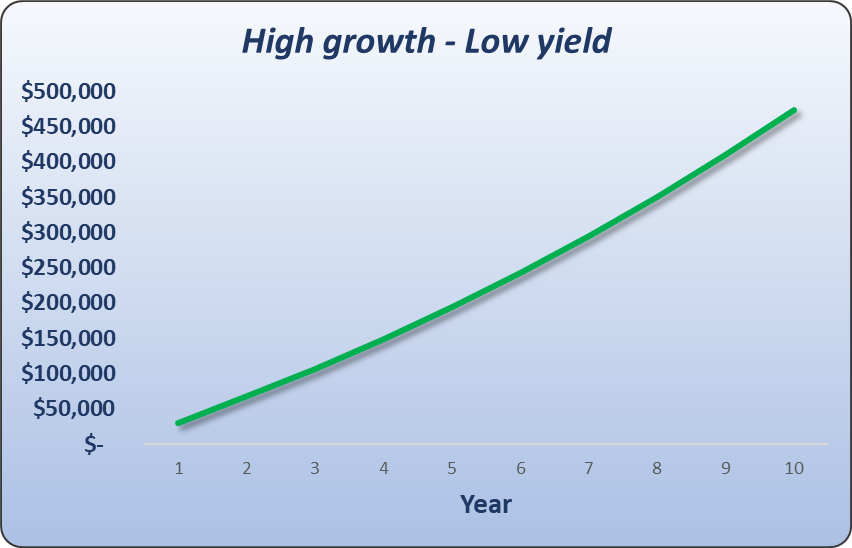

Now compare that with the following chart in which the yield is very low (3%) and the growth is much higher (7%).

The total wealth created (equity and cash-flow) is around $473,000. In just ten years there’s a staggering difference between the two properties’ performance.

Note it’s highly unlikely that such consistent yields and growth rates will be seen over a 10-year period. But the idea is simply to compare the influence of yield and growth in isolation.

Why?

There are a couple of reasons why growth ends up being better than yield:

- More tax is paid on positively geared properties

- Growth also affects rent

Positively geared properties generate more income from rent than they deliver in expenses. That extra amount of money is taxed. The degree of positivity is diminished because of tax.

Secondly and much more importantly, rent climbs with capital growth. It might not happen at the same time, but capital growth and rent both change because of the same reasons – supply and demand. What lifts property prices, also lifts rents.

My Story

Early in my property investing I chased after yield. I bought in: QLD, Tassie, WA and South Australia. When I couldn’t find higher yields in Australia, I went to New Zealand. I bought 6 houses in NZ with yields all in the double digits. But it still wasn’t good enough, so I went to the USA.

Upon reflection I realised that yield wasn’t the key to creating wealth. In every case it was the capital growth that made the big difference. It didn’t matter how good the yield was, it was always trumped by growth. If I had high yield and low growth, the yield simply didn’t compensate enough. If I had high yield and high growth, the growth always delivered more than the yield did.

“If you’re trying to build wealth through property investing, your top priority should be capital growth”

When is yield OK?

There are occasions when you have to consider yield. If you get good at picking growth locations, you’ll quickly realise you have more equity than you can make use of because of lending serviceability constraints.

I suggest aiming for the best growth location that is neutrally geared or just positive – enough to get the next mortgage across the line.

There’s only one case in which it makes sense to go “all-out” on yield and forgo growth altogether…

Retirement

If you’re retiring, you want income and you probably don’t care about asset growth. You’re looking for something to replace your salary.

You might need to sell down part of your portfolio to make it cash-flow positive. You might even consider swapping out growth properties for a set of high yielding ones, possibly commercial. Maybe even consider some high yielding shares instead of property.

Isn’t growth speculative?

Proponents of cash-flow strategies suggest that capital growth is speculative. They believe that rent is more of a sure thing.

Don’t be fooled by a rental lease. It’s not a sure thing just because it’s the case right now. That tenant could vacate next month along with all of the other transient workers in the area if the economy goes pear-shaped.

Supply and demand affect price growth and rent. Supply and demand affect vacancy rates too. You need to understand supply & demand for the market you’re considering, regardless of the strategy you employ.

Oh, and by the way…

“If a property investment advisor says growth is speculative, they obviously have no idea how to pick growth locations”

Growth AND Yield

You can get both high yield and high growth. It doesn’t last forever, but it’s worth pursuing. And the research required is the same – high demand, low supply. A few traps though to be wary of:

- Why do you think growth will come?

- Are yields high because prices have fallen?

- Above average growth doesn’t last

- Above average yield doesn’t last

Firstly, why do you think a certain location is going to have high growth. I wouldn’t need to invest in property to make a fortune if only I had a dollar for every failed hot spot pick that I’ve heard.

Secondly, bear in mind that high yielding locations can quite often rise up from prices stepping down. You don’t want to jump onto that kind of a trend.

Thirdly, above average growth never lasts. So, be sure to keep your eye on those markets after you’ve bought in them. Have a plan to refinance or liquidate when growth starts running out of puff.

Finally, just like above average growth, above average yields won’t last forever either. High yields are frequently a symptom of a market nobody really wants to settle in. Why would residents prefer to pay more in rent than they would in mortgage interest? Simple, it’s because they don’t plan to stay long.

Conclusion

As a general rule, prioritise growth. Better still, don’t focus on yield OR growth, focus on supply and demand and you’ll probably end up with both high growth and rising rents.

....................................................................................

Jeremy Sheppard is head of research at DSRdata.com.au.

Jeremy Sheppard is head of research at DSRdata.com.au.

DSR data can be found on the YIP Top suburbs page.

Click Here to read more Expert Advice articles by Jeremy Sheppard

Disclaimer: while due care is taken, the viewpoints expressed by contributors do not necessarily reflect the opinions of Your Investment Property.