Let’s dive into Part II now of Structuring Investment Property Finance by looking at a case study.

Laura is a single mother living in an inner city terrace worth $950k with her teenaged son. She has a mortgage of $550k and an income 0f $90k pa. She bought an investment unit 2 years ago for $450k with an interest only loan of $475k and she currently receives $400 per week in rent.

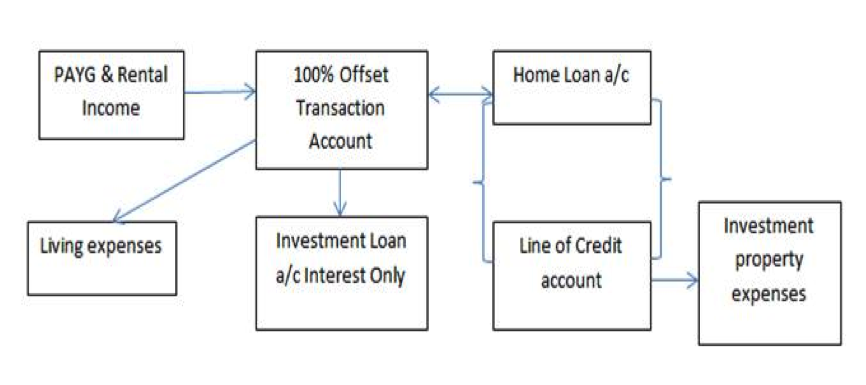

Laura’s current overall gearing of 73% would allow her to establish a Line of Credit of $98k and still remain below 80% LVR. In the event, the valuation of her owner occupied home came it $935k, so the credit limit offered her by her lender was reduced to $83,000. As part of her restructure, she also arranged for the establishment of a 100% offset account against her owner occupied home loan account.

Note that the Home Loan and Line of Credit accounts are bracketed together because the balance of the LOC should only increase by the same amount as the net balance of the Home Loan account (ie. less the Offset Account balance) actually decreases.

Laura’s finance structure has every dollar she earns working to its best advantage for her every day. If she uses a credit card for all her living expenses and has it “swept” automatically every month by the Offset Account so that she incurs no interest, she will have an optimal finance structure.

The real beauty of the structure is that it is self-maintaining; it just looks after itself. All Laura has to remember to do is to pay expenses related to her investment property from the LOC account. Her list of expenses looks like this:

- Quarterly strata fees: $1100

- Quarterly Council rates: $240

- Quarterly Water rates: $80

- Monthly management fee: $120

- Monthly Insurance premium: $140

- Annual fee for tax return: $660

- Total annual expenses: $9460

So the effect of the structure is to convert non-deductible debt to deductible debt. The greater your expenses, the faster you can do it.

Note that Laura will have to apply to her lender to have the credit on her LOC account increased several times over the 16 year period, but that should not be an issue as she can simultaneously reduce the home loan limit by the same amount. Let’s also not forget that all of Laura’s properties would have grown considerably in value over that 16 year period. Quite possibly that property could have quadrupled in value so that, despite her dipping into her equity bit by bit, her loan to valuation ratio would have reduced considerably.

But what about going the whole hog and capitalizing interest on the deductible loan by paying it from the LOC account? This is not something you should consider doing without discussing and taking advice from your tax adviser. It is something that is very much “in the crosshairs” of the ATO at present and, whilst there are individual circumstances where it might be very justifiable, to pursue this strategy aggressively and across the board could be asking for trouble.

Stay tuned for Part III where I’m going to give a brief history on the structuring of finance!

In the meantime, if you’d like to connect with us here at W Financial, we have a special offer on for Your Investment Property Readers. Visit us here, fill out your details and we’ll gift you a free Finance Blueprint Consultation normally sold for $550. On this consult we’ll explore how you can start or grow your property portfolio on the most strategic path possible for you to hit success as a property investor. Why talk to us? At W Financial our entire team are established property investors, myself included. We have millions of dollars in portfolios between us and have secured over half a billion dollars in loans for our investor clients.

Michelle Coleman is a first-rate mortgage strategist and mum, and she heads up the team at W Financial. She is without a doubt, a legend of the Australian mortgage broking industry, having achieved over $500M of settlements in her 12+ year career to date, and won numerous industry awards, including #3 MPA Top Broker. Michelle is also a highly experienced property investor. www.wfinancial.com.au

To see the rest of this series and to read more Expert Advice articles by Michelle, click here

Disclaimer: while due care is taken, the viewpoints expressed by contributors do not necessarily reflect the opinions of Your Investment Property.