You’ve probably heard or read that borrowing on a low deposit could put you at serious financial risk. But as Jeremy Sheppard explains, there is a strong case to adopt this strategy if you want to build your portfolio quickly

All investing comes down to two considerations: risk and return. Ideally, you want to eliminate risk and maximise return. It doesn’t matter what type of investment you’re considering – buying property, buying shares, fixed-interest deposits, small business, foreign exchange trading, you name it – these two key principles of risk and return govern how successful you’ll be.

For property investors, consideration of the loan to value ratio (LVR) plays a crucial role in determining the risk and return potential. The widely held belief is that the higher the LVR, the higher the risk. But the reverse can actually be true in some cases.

LVR

If you buy a $500,000 property and have a $400,000 mortgage, then you need a $100,000 deposit. Twenty per cent of the property’s value is the deposit and 80% is the loan. The value of the property is $500,000 and the value of the loan is $400,000. So the LVR is 400,000 / 500,000 = 0.8 or 80%.

In other words, the LVR is the ratio of the size of the loan in dollars to the value of the property in dollars. The LVR is usually expressed as a percentage.

Bad stuff happens

Imagine you bought a $500,000 property at 100% LVR, but you couldn’t make the interest payments and the lender sold the property to recoup their losses. If the property had dropped by as little as 10%, the lender would only get $450,000 of their $500,000 back. They’ve made a $50,000 loss, which no doubt they would have to chase you for and it would cost them even more to do that chasing.

Now imagine you bought that same $500,000 property but this time at 80% LVR. With a smaller loan, you would be paying less interest, but let’s assume you still couldn’t make ends meet. The lender would sell the property for $450,000 and there would be another $50,000 left over to pay the legal fees, agent’s commission and any other loss they may have incurred.

You can see that a lender wants the lowest LVR they can get to minimise their risk.

Lenders mortgage insurance

The lender stands to lose quite a bit if things don’t go as planned. Some lenders want insurance against this risk. The higher the LVR is, the higher the risk. The higher the risk, the more insurance cover the lender will want.

Mortgage insurers provide this insurance. It works the same as any other insurance: a premium is paid to the insurer, and in the event that bad stuff happens, the insurer pays the claim.

Lenders mortgage insurance (LMI) is a premium paid by the buyer to the mortgage insurer. Lenders will ask borrowers to pay this expense on their behalf as a condition of lending the borrower the money.

Typical LMI premiums

The premium you pay for LMI is a one-off fee and is based on the size of the loan and the LVR. As the size of the loan increases, the size of the premium increases. Also, as the size of the LVR increases, the size of the premium increases.

The LMI premium is based on a percentage of the loan size and can range from 0.25% for small loans and low LVRs right up to around 5% for large loans with high LVRs.

To quickly estimate your LMI premium, there’s a handy calculator on the Your Investment Property website (www.yourinvestmentpropertymag.com.au/calculators/mortgageinsurance/) where you can just plug in the amount you want to borrow and the value of the property and it calculates the premium for you.

Property value: $500,000

Loan amount: $450,000 @ 90% LVR

Estimated LMI: $6,300

How does high LVR affect future borrowing?

Not having had a high-LVR loan for quite some time, I thought it prudent to consult a professional. I asked mortgage broker Paul Holland of Mortgage Choice how high-LVR loans affect an investor’s future borrowing capacity.

Holland said combined lending with one mortgage insurer could be an issue.

“A mortgage insurer may refuse a loan if they already have too much exposure to a particular borrower,” he said. “For example, it is not unheard of for a borrower to have a loan with one lender that uses a particular mortgage insurer and then apply for another loan via another lender that happens to use the same mortgage insurer and have that second loan rejected by the mortgage insurer.

“Of course, if LMI isn’t needed, a mortgage insurer is not a problem and then there are loads of lenders to choose from. But there are only two major mortgage insurers, though some lenders self-insure, like some of the big banks. A high-LVR loan may limit your options in the future if you want to go high LVR again.

“Keep in mind that some lenders send a portion of their loans to mortgage insurers, even when the LVR is only 80%. They do this for added protection. So you’re not immune to mortgage insurers even if all your loans have an 80% LVR or lower.”

It’s a popularly held belief that the higher the LVR, the higher the risk. This is certainly the case from the lender’s perspective. But from the investors side, it is not necessarily so.

Example 1: Diversification

If you only have $100,000 available for a 20% deposit on a $500,000 property, you’re putting all your eggs in one basket buying that one property. If you’ve picked the wrong market or got the timing wrong, you may be holding it for a long time before seeing any growth.

If you instead bought two $450,000 properties with a 90% LVR, in completely different markets, then you would have reduced your investment risk by diversifying.

There’s more chance that one of those markets you picked would have been an astute choice.

Example 2: Emergency money

Let’s say you’re eyeing up a $500,000 property and you have the $100,000 deposit ready, but you don’t have much left over to cover stamp duty and legal fees. There’s enough in the account, but only just.

This is a pretty risky position to be in. If something happens to the property after settlement, like a nightmare tenant or the discovery of some structural fault, you’re not in a position to cover the costs. If you lose your job, you need time to find another. Having emergency money on hand is vital for keeping your property from being sold by the lender.

Taking the higher-LVR option actually reduces your risk because you will then have excess funds on hand for these types of emergencies.

Example 3: Value-adding

If you have some money left over after the purchase, you can perform some renovations to both add value to the property and increase its yield. This may put you in a safer position than if you put all your cash into a lower-LVR loan product.

It all comes down to how much value you can add with your renovation and how much extra rental income it will generate. If you spent $40,000, for example, on the renovation and it added a measly $60,000 in value, that would be 50% return on investment – pretty good.

And if the renovation added an extra $60 per week to the rental income, that would equate to an extra $3,000 per year. That’s a cash-on-cash ROI of 7.5%. It’s nothing flash, but it’s better than money in the bank.

If either of these two things happened, or better, then I’d say that $40,000 was better spent on the reno than on the deposit.

In this case, where mortgage insurance is paid for an 80% loan, Holland said the premium would be paid by the lender instead of the borrower having to pay it. Low-doc loans over 60% LVR could also trigger LMI, Holland said, so this is not something that just affects high-LVR borrowers. However, “some lenders will waive the LMI up to 85% or even higher for special borrowers like doctors”, he added.

Are high-LVR loans more expensive?

The short answer is it depends on the lender. “Every lender is different,” said Holland. “Recently, a few lenders had little difference between the interest rates offered for low-LVR loans and those for high-LVR loans. But more so now lenders are trying to reduce their risk, so they want more mortgages with LVRs of 80% or lower. As a result they are offering more attractive rates for the lower-LVR loans. In some instances, borrowers who take out a high-LVR loan may find their interest rate is as much as half a percent more expensive than those borrowers with a low-LVR loan.”

Questions to ask yourself when considering a low-deposit loan

Should I go high LVR?

The first question that needs to be answered is whether you can go high LVR. Once your mortgage broker has gone over your financials, ask for a range of loan products with varying LVRs. If you have no option, then the discussion is moot.

Can you sacrifice other loan features?

Note that there may be high-LVR products available but at a cost of losing some other beneficial feature. Perhaps the high-LVR products aren’t available for buying in trusts or perhaps they come with a heavier interest bill or you have to pay principal and interest instead of interest only. The strategy of the investor and their financial circumstances will determine precisely which features are worth giving up for a high LVR.

Do you have a small deposit?

If you simply don’t have the funds to put down a 20% deposit, then a high LVR may be your only option. But have you considered cheaper locations or cheaper properties within the same location?

If you’re sure you’ve found the best location and the best property in that location and you can’t afford a 20% deposit, by all means go down the high-LVR path. If you’ve found a well-priced property in a decent growth spot, then you’re better off jumping in than trying to save a bigger deposit. Once you’re in the market, you’re moving with it rather than chasing after it.

Do you have good cash flow?

Make sure your cash flow is pretty strong if you’re choosing high LVR. You don’t want to be forced to sell. The lender or mortgage insurer will look over your financials with a microscope anyway. Just don’t try to make your case appear better than it really is.

Are you sure of short-term growth?

If things do go pear-shaped and you need to liquidate in a hurry, you want the market you’ve bought into to have had some capital growth already. You need to be confident of where prices are heading in the immediate future; that is, before you start to default on loan payments.

A good tool for checking this is the DSR (Demand to Supply Ratio). Although it is not a predictor of capital growth, the DSR is a good ballpark estimator of capital growth potential. You can use it as a safety net to ensure you’re not going to buy into a dud market. If the DSR score is not that good for the market you’ve targeted, then it should trigger alarm bells. The Your Investment Property website (www.yourinvestmentpropertymag.com.au/top-suburbs/) publishes these stats. You can also get the full listing at DSRScore.com.au.

Will you fit into a high-LVR risk irony?

Can you create a case like one of the examples above on high-risk LVR ironies (see box, p30)? Will a higher LVR free up some cash you can put to good use?

You could perform a value-adding renovation soon after settlement to create some equity breathing space.

Keep in mind that you can’t claim the renovation as repairs and maintenance if it is straight after settlement, so this option is not very tax-effective.

An easier option, especially if renovations aren’t your thing, is to get instant equity at settlement by buying off the plan. This is on the assumption that capital growth occurs between contract exchange and settlement.

Even better would be to buy at cost price if you can develop, actively or passively. You get the benefits of growth prior to settlement as you would with the off-the-plan option, and instant equity from acquiring at cost price.

Remember that if you can afford a high-LVR loan, your serviceability is pretty good. That may mean you’re paying too much tax. So a new property with greater depreciation benefits like off the plan or passive development may be a better choice than renovating.

Do you want to diversify?

As I mentioned earlier, you can almost double your buying potential by halving the deposit. That means you could buy two properties at a higher LVR. So long as you choose completely different property markets to invest in, this could be a good idea.

Do you want to maximise ROI?

I’m a bit of a data nut-job. I love spreadsheet analysis too. Every property I buy, I put together a spreadsheet listing the injection of capital and the ongoing costs and income. I try to project capital growth too. The bottom line is what I’m interested in – the ROI.

If I pay stamp duty, legal fees and a deposit of $100,000, then I want a good return on that investment. If all goes according to plan, invariably this ROI figure is much larger with high-LVR loans than with low-LVR loans.

In fact, my number one goal when I first started buying property was to find the loan with the highest LVR. Even when interest rates got up to 9%, the ROI was still better with a high LVR than with a low one.

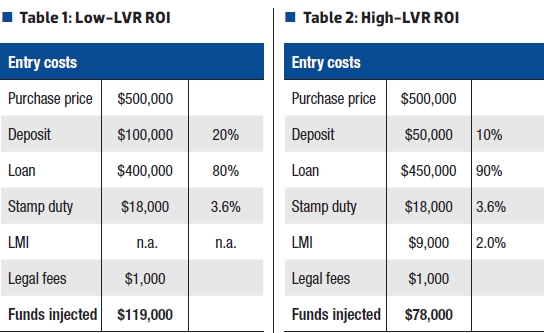

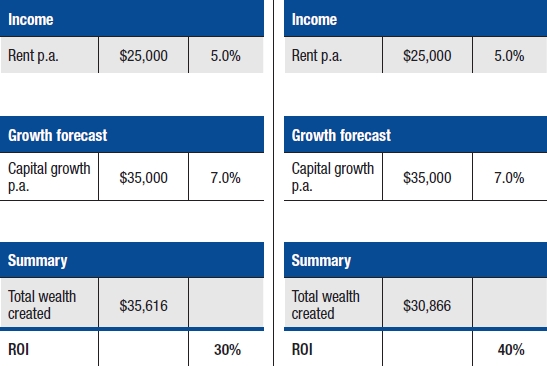

The simple spreadsheet in Table 1 shows the ROI for an imaginary property with an LVR of 80%. Table 2 shows the ROI for the same property with a 90% LVR.

High vs Low ROI (Click to enlarge)

In the ROI spreadsheets I’ve left out consideration of depreciation since this will be the same in both high- and low-LVR cases, and it keeps the spreadsheets simple. Have a look at which option gives the best return on your investment. It’s the high-LVR option, despite paying more interest and the extra cost of LMI.

Note that there is not much point in choosing a high-LVR product simply to make a spreadsheet look good and to say you have a high ROI. If you aren’t going to use the excess funds a high LVR frees up, then you may as well go for the low-LVR option.

Note that there is about $40,000 in excess funds left over with the high-LVR option in Table 2. You can save some of that for emergencies and spend some of it on renovations. Or you could perhaps buy another cheaper property.

Suitable strategies

A high-LVR loan suits most investment strategies. However, the ability to source such loans is a little more difficult for some strategies than for others.

Many lenders will not be interested in offering high-LVR loans for developments or the purchase of regional property or property in locations where there may be oversupply or significant exposure for that lender already. Remember that a high LVR spells trouble for a lender, so they want the lowest-risk property as security.

Depreciation of the LMI payable for a high-LVR loan can be claimed over five years. If your strategy is for a shorter term, it may be considered a waste to pay the premium. Check with your accountant concerning your specific plan for the property. You may be able to write off the full amount for short-term projects.

There may also be a chance you can claim back the LMI premium from the insurer if you sell the property soon after purchase, for example with a renovation flip. Check with your mortgage broker or ask the mortgage insurer directly.

It is probably safer to use a low-LVR loan rather than a high-LVR product for short-term projects.

Can I keep going with high LVR?

No. Eventually, you’re going to have to drop your LVR requirements. There are a few reasons:

- The extra debt increases the interest cost, and you’ll have trouble servicing the debt.

- The high degree of leverage makes you a high risk to lenders.

- You will run out of mortgage insurers.

- Eventually you’ll want to retire on your portfolio and this won’t be positively geared at such a high LVR.

Should I go low LVR?

Assuming you have the deposit funds to do so, a low LVR gives you a few positives:

- Lower debt means more sleep at night.

- Lower debt means lower interest payments.

- Lower debt means you’re more attractive to future lenders.

- Lower debt means you’re closer to an LVR suitable for retirement.

Suitable strategies

Any unusual or higher-risk investment strategy would suit a low-LVR loan. The standard 80% LVR suits most property investment strategies. Large developments may require an even lower LVR. The lower the LVR, the more lenders you’ll find and the more flexible they’ll be. So if there is anything unorthodox about your strategy, low LVR is for you.

No choice

Depending on your serviceability, you may have no choice but to go for a low- LVR loan. That doesn’t mean you’re not going to make as much of a profit; it just means the injection of funds you will need in order to get that profit is larger.

More important than LVR choice is the choice of location and the type of property you purchase – and maybe what you plan to do with it too. Don’t let the lack of choice of loan products stop you from making great investments. Getting into the market early any way you can is better than getting in late with the perfect loan.

Jeremy Sheppard is an active property investor and the creator of DSRscore.com.au

This article is from the December issue of Your Investment Property Magazine. Purchase the issue to read more.