There are a number of factors investors need to consider when working out which investment strategy best suits their situation, based on the amount of tax they pay each year.

Your income level is a key issue initially, says Nick Khachatryan, CEO of NewRealEstate properties.

“An individual earning $52,000, with dependent children and a monthly mortgage, pays approximately $8,000 in income tax annually. Once you minus their mortgage repayments and living expenses, it leaves very little room for a comfortable lifestyle,” Khachatryan explains.

“This is where cash flow property becomes very attractive, because the property pays for itself and can deliver anywhere between $4,000 and $10,000 in passive income annually.”

If you can avoid using that passive income to cover living costs, you could reinvest your cash flow returns into actively paying down your mortgage. Set your portfolio up with five of these cash flow properties and pay them all off over a decade or two, and you could enjoy a profitable portfolio that sustains your income in retirement.

The goal for most Australians is to pay as little tax as possible, which is why negative gearing is such a popular investment tool – particularly for those earning in the highest income bracket.

Those who earn over $180,000 are currently gifting the government almost half of every dollar they earn over and above this amount, which is a considerable stack of cash.

Those who earn over $180,000 are currently gifting the government almost half of every dollar they earn over and above this amount, which is a considerable stack of cash.

For this reason, high-income earners who invest in real estate are generally better off chasing capital growth while parking their dollars into homes that can be negatively geared.

Under negative gearing regulations, every dollar your income-producing investment property costs can be claimed at tax time, after your rental income has been accounted for.

“Most of the time, capital growth properties tend to be negatively geared, because of their higher purchase price. These types of properties are usually most suitable for high-income earners, such as doctors and lawyers, as it allows them to reduce their tax liability,” explains Sonali Rodrigo, financial planner at Tomorrow Financial Solutions.

“A lot of the time, we tend to recommend they go for newer properties, as this lets them take maximum advantage of the depreciation allowances as well.”

Depreciation can often transform a negatively geared property into an asset that actually costs you next to nothing to hold, adds Cam McLellan, director of Open Corp.

“I’ve purchased many established properties in my time, but for the last decade or so, I’ve only purchased new properties,” he says.

“Buying new property is a must to maximise taxation benefits, namely depreciation, as it means that your growth property costs you very little, if anything, to hold.”

Let’s see how a depreciated capital growth property strategy could work in practice for a high-income earner.

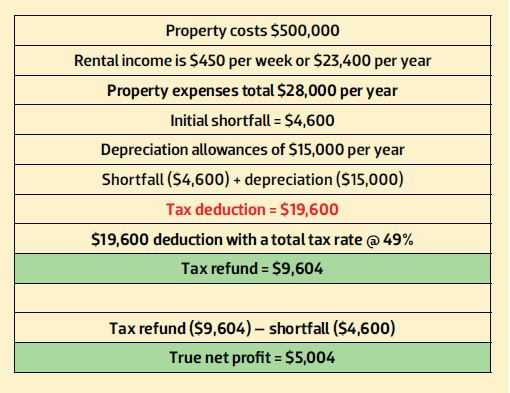

• Daniel earns $250,000 annually.

• He purchases an investment property in a growth suburb of Brisbane for $500,000

• The property is expected to grow in value by 5-6% annually.

For Daniel, purchasing a negatively geared capital growth property and depreciating the asset gives him an annual tax deduction worth around $20,000, while the underlying asset continues to grow in value at a rate of around $30,000 per year.

For Daniel, purchasing a negatively geared capital growth property and depreciating the asset gives him an annual tax deduction worth around $20,000, while the underlying asset continues to grow in value at a rate of around $30,000 per year.

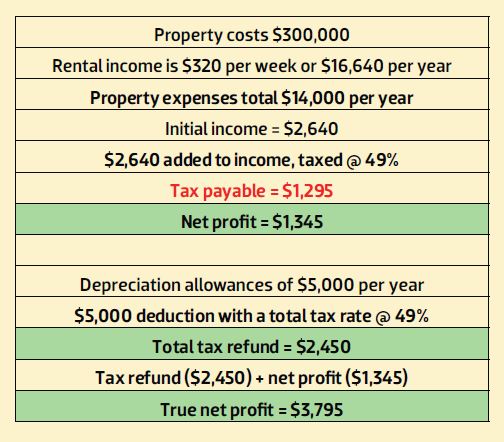

If Daniel purchased a positively geared investment, on the other hand, his return would be far lower.

In this instance:

• Daniel earns $250,000 annually.

• He purchases an investment property in a high cash flow regional suburb of Queensland for 330,000

• The property is expected to grow in value by 1-2% annually.

• At face value, it will also return $120 per week, or $6200, in positive cash flow.

By investing in a positive cash flow property, Daniel ends up pocketing around $3,800 per year, while the underlying asset is expected to grow in value at a rate of $3,000–$6,000 annually. Clearly, for someone in Daniel’s position, a capital growth property can deliver far better returns and makes much more financial sense than a cash flow investment.

By investing in a positive cash flow property, Daniel ends up pocketing around $3,800 per year, while the underlying asset is expected to grow in value at a rate of $3,000–$6,000 annually. Clearly, for someone in Daniel’s position, a capital growth property can deliver far better returns and makes much more financial sense than a cash flow investment.

That said, there are many lifestyle factors you need to consider, Rodrigo advises.

“You may be high-income earners and a negatively geared investment may make sense for you, but if you’re putting your discretionary cash into that and you want to send your kids to private school in a few years’ time, that could have an impact,” she says.

“You’ve really got to look at it from a big-picture viewpoint, and that’s why we spend quite a lot of time working with people on their goals and discussing what they want to do in life.”

This is why the CEO of NewRealEstate.properties, Nick Khachatryan, says it’s essential that investors seek professional advice when they weigh up the tax implications of any potential investment prior to purchase, so they don’t end up making an unprofitable decision.

“Particularly when you’re deciding to purchase an investment property that is cash flow positive, it’s essential that you discuss the matter with a qualified and licensed accountant or a financial planner,” he says.

“You want to ensure that your rental gains won’t place you in the next taxation bracket, as this will mean that more tax is payable.”

When does cash flow investing make most sense, tax-wise?

When embracing a cash flow strategy, as an investor you will essentially end up with an asset that gives you money left over after all of your property ownership expenses are paid.

“Whatever this amount is, it’s going to get added to your taxable income, so usually we recommend this for lower-income earners,” Rodrigo says.

“If you’re earning a low income it can be hard to save a deposit anyway, so you may gravitate towards more affordable positive cash flow investments from that point of view. But when your tax bracket is lower, having that cash flow added to your income doesn’t cause too much of an issue.”

Rodrigo defines a low-income earner as someone who earns around $50,000–$60,000 or less. “A high-income earner would be receiving an annual wage above that amount, and a super-high-income earner has an income upwards of $100,000,” she says.

“That said, there’s no hard and fast rule and it’s really important that people look at it from a holistic point of view, because your situation could change.”

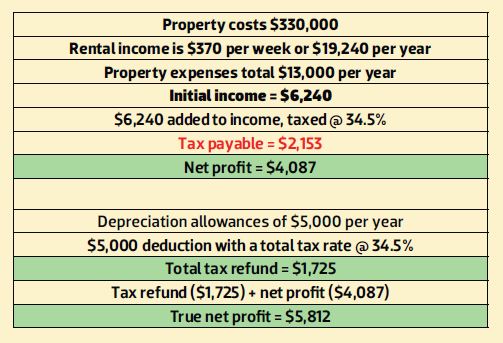

The following is an example of a situation in which a positive cash flow does make sense, from a tax perspective.

In this instance:

• Kathy earns $55,000 annually.

• She purchases an investment property in a high cash flow regional suburb of Queensland for $330,000.

• The property is expected to grow in value by 1-2% annually.

• At face value, it will also return $120 per week, or $6200, in positive cash flow.

By investing in a positive cash flow property, Kathy has increased her annual income by $5,800, while the underlying asset is expected to grow in value at a rate of $3,300–$6,600 annually.

By investing in a positive cash flow property, Kathy has increased her annual income by $5,800, while the underlying asset is expected to grow in value at a rate of $3,300–$6,600 annually.

This is a strong outcome for a person in Kathy’s position, particularly as her income likely wouldn’t be sufficient to support a heavily negatively geared investment.

Close to retirement?

Another factor that all investors must consider is how close they are to retirement, Rodrigo cautions.

“An important tax consideration is that, at the time of selling, if you’ve made a capital gain, the taxman is going to want to take a slice of it,” she says.

“Keep in mind that even with the 50% discount currently on offer, the ATO will want their share of your property’s price growth. It’s really important to be strategic about when you sell.”

She suggests that investors look for opportunities to defer selling until they’re not earning much in the way of a regular income, if possible.

“If you’re going to retire in, say, two or three years, it will be in your best interests to wait and sell your investment property then. When you’re retired and over age 60, any money you pull from super is tax-free, so if you do sell it at that time, only the profit on your capital gain is going to be taxable,” Rodrigo says.

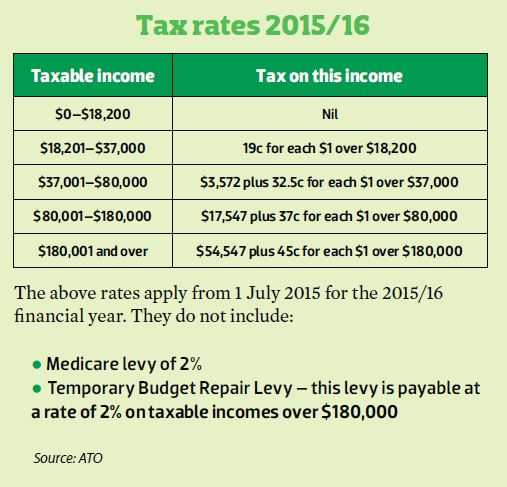

This means that if your capital gain were $100,000, you would receive a $50,000 CGT discount and only pay tax on $50,000 worth of profit. In this instance, the first $18,200 worth of capital gain would be tax-free and the total tax payable would be just $7,797, at current tax rates (refer to tax rates boxout, p30).

You then keep more than $92,000 of your profit for yourself.

HOT TIPS: Depreciation homewreckers

There's a little-known depreciation risk that many buyers aren't aware of, warns Adriana Filipowski, director of Village Finance, and it involves buying an already-depreciated home. "It's important to doubt check the contact of sale of any property you're considering buying, because if the property was owned by an investor, the chattels may have already been depreciated to zero," she explains. "You can ask the vendor to change this; however, they will then need to pay tax on the altered amount, so they may be reluctant to do so. It does mean, though, that there may not be anything for you to depreciate, which is important to know when you're calculating your returns."