07/06/2018

Property is an excellent source of passive income, which is why so many people get into this type of investment. However, it’s not as easy as just buying a house and leaving it there to appreciate – the typical goal is to lease it out and profit from there. Thus, keeping a well maintained, safe home is vital to your investment journey and to your reputation in the property industry.

As a landlord, you want to be able to offer prospective tenants a dwelling that is comfortable and secure. You also want to safeguard your investment, especially since it is largely at the mercy of others. The possible issues for investors are generally related to upkeep, damage and tenants. All these things can be costly, so it’s best to be proactive and take preventive measures before they take a chunk out of your savings.

Many of the big risks of property ownership can be easily rectified, reducing significant liability risks for landlords. Let’s look at a few of the biggest potential pitfalls and how to minimise the chances of a negative outcome.

RISK: DETERIORATION AND BREAKAGE

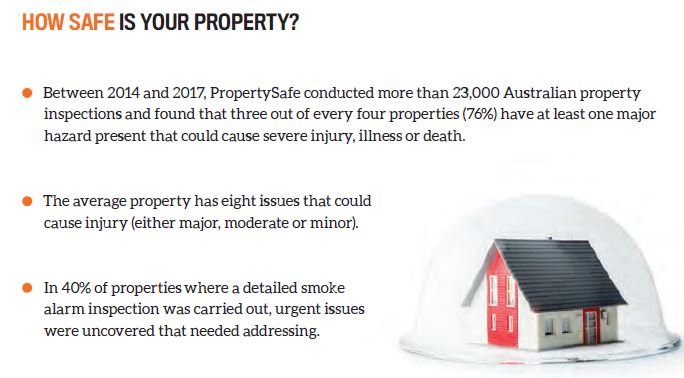

Over time, a property slowly deteriorates – that’s why the government compensates investors for depreciation. As a property owner, it’s important that you stay on top of repairs and conduct routine inspections to make sure everything is in good condition, especially as it relates to the structure and foundation of the property.

Mitigation strategy: Regular maintenance and prompt repairs

Scheduling maintenance checks definitely will take time and money, but at least you can dictate the schedule, as opposed to having your day disrupted because you need to deal with an emergency repair. Parts of the home you want to monitor include the plumbing, electrical works, the building materials and the appliances.

If you discover problems, always look to fix them as soon as possible. The longer you leave a problem, the more it will impact the value of the home.

RISK: FIRE DAMAGE

This is a major problem, especially if tenants cook or light candles, as fire can affect more than just your property – if it gets out of hand, lives are at risk. So it’s crucial to have fire safety procedures in place and to ensure that tenants are conscientious about keeping to regulations like making sure the gas is properly turned off.

Mitigation strategy: Up-to-date smoke alarms

Smoke alarms have a typical lifespan of eight to 10 years, but the battery does need to be replaced once a year. It’s a good practice to regularly make sure your property’s smoke detector is working effectively, especially if a tenant has just departed. You can do so by lighting a candle under the sensor can detect it.

If there’s a problem with the sensor, it’s best to buy a new smoke alarm since they’re not too expensive, and the small outlay is well worth the potential of risk of having a faulty alarm.

RISK: TENANCY DRAMA

Every landlord hopes to get great tenants who are respectful, neat, quiet and pay rent on time. However, that’s not always the case, and more often than not, you get tenants who give you major headaches. So you definitely want to be ready for pet problems, roommate disagreements and, at worst, the possibility of eviction.

Mitigation strategy: Landlord insurance

Tenant-related issues can be expensive, especially if legal expenses are necessary, so landlord insurance is a must-have. This insurance generally covers theft or burglary by tenants or their guests, malicious damage or vandalism, loss on rent profits due to defaulted payment, and the legal expenses related to eviction. This insurance is tax-deductible because it is considered an investment expense.

When getting landlord insurance, it’s important to check not just the price, but also the provisions included. You’ll also want to determine if you’ll need special conditions related to the weather or to pets.

Landlord insurance is not just limited to long leases – policies have also been developed to cater to short-term rental properties like those on Airbnb and Stayz.

Every landlord hopes to get great tenants who are respectful,

neat, quiet and pay rent on time. However, that’s not always the case.

RISK: LACK OF PLANT MAINTENANCE

If your property has a lawn or a garden, there’s a good chance you could come back to dead or overgrown landscaping, which could be troublesome if it lures in insects or other pests. It can also be disheartening, especially if you’ve put a lot of effort into the upkeep.

Mitigation strategy: Know what you're responsible for

Tenants are generally only required to maintain plants to the standard in which the landlord left them, but this is not a hard rule, so you’ll want to make sure that the need for plant maintenance is specified in the tenancy agreement. Moreover, tenants have no responsibility if the area has restrictions on the use of water. Finally, plants requiring special maintenance – such as tree removal – are definitely out of the tenant’s hands.

RISK: PEST DAMAGE

Pest-related problems are common and should never be taken lightly because of the potential for significant damage. Termites are capable of destroying a property all the way down to the foundation, and an ant invasion can cause structural damage as well. In addition, infestations of cockroaches, rats and fleas can bring disease to the household.

Mitigation strategy: Regular inspections by pest control

When looking for a pest control company, the main factor is to know exactly what kind of services Mitigation strategy: Regular inspections by pest control When looking for a pest control company, the main factor is to know exactly what kind of services you'll be getting. For instance, some firms might focus exclusively on wood destroyers like termites while you're looking for a thorough inspection that covers all kinds of pests.

Fleas and ticks can often breed in carpeting, especially if an occupant has dogs or cats. The property could also be harbouring spiders, especially if you live near bushland or cultivate plants. Rats and cockroaches typically go where there’s food, so you want to nip these infestations in the bud before they bring harm to tenants or drive potential ones away.

RISK: POOR PROPERTY MANAGEMENT

As with every profession, property management is not immune from ‘dud’ operators. Many property managers are experienced, professional and passionate about customer service, towards both the landlord as the client and the tenant as the paying customer. But some simply do the bare minimum, meaning they collect they rent and that’s about it. They don’t perform regular inspections or communicate efficiently – some may even fail to follow the legal guidelines when it comes to bond lodgement and tenancy breaches, which is a huge no-no.

Whether their client book is too large, their resources stretched or they just don’t have their heart in it, these are the types of property managers you want to avoid at all costs.

Mitigation strategy: Manage your managers

Ideally, once you have A-grade property managers in place, they should manage your investment without too much input from you. However, initially, you may need to invest some time into the relationship to ensure they’re delivering the service you expect.

To do this, arrange a meeting or phone call to run through their service and your expectations. How often do they conduct rental inspections? Will they provide you with regular (at least annual) rental appraisals? Do they take photos on your behalf, and can they manage payment of council rates and insurance for you?

You can also do things like diarise the dates of six-monthly routine inspections; if your PM hasn’t arranged an inspection, ask them why. They should also contact you two months before your tenant’s lease is due to expire, so make a note of these dates.

Professional experts: A good property manager, an accountant with property management experience and a mortgage broker are all essential team members.

Savings: All property investors should have a small buffer account of at least $5,000 per property to manage emergency expenses.