“During high school and uni, my dad would always encourage me to go out and get a job to forge the idea that investing your time and energy day in, day out for a pay cheque is hard, and not something you want to be doing all the way up to retirement age,” Michael says.

“Since starting high school, all of my casual jobs were in some way highly labour-intensive – cleaning the local chemist, being a butcher’s assistant at the deli, and tagging along with my dad to work six days a week at his rubber factory during university semester breaks.”

These physical jobs were hard work, but Michael appreciates the huge gift they gave him: the resolve and drive to create financial freedom so that he wouldn’t be bound by these types of jobs for the rest of his life.

“My first job out of uni was to sell ad space at a financial services industry newspaper,” he adds.

“I didn’t do an amazing job closing advertising leads, but I was exposed to a vast range of expertise and opinions from professionals across funds management, financial planning and superannuation. They were happy to impart their advice to a newly graduated ‘young un’ who was happy to listen and take notes furiously!”

Profiting from the GFC

Profiting from the GFC

During those days of learning and absorbing everything he could from those with more experience, Michael says he came to an important conclusion.

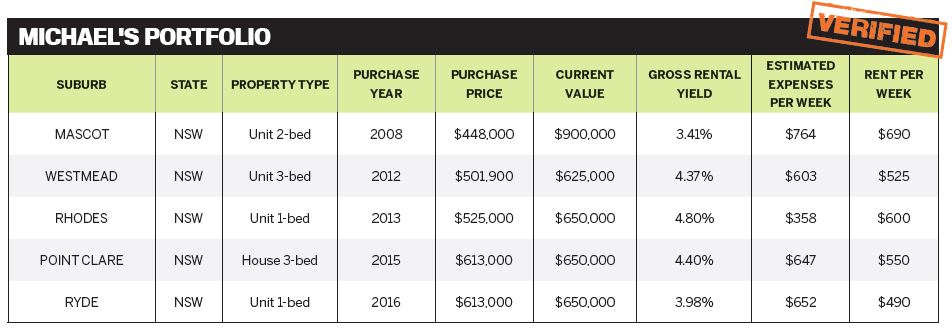

“I realised that 2008 presented a once-in-a-lifetime opportunity to get into the property market while prices were depressed. My first property was purchased right after Christmas 2008, when I was 23; it was a two-bedroom unit in Mascot, Sydney, and I paid just under $450,000,” he says.

“I had about $15,000 saved up from odd jobs in high school and university plus my first year of full-time work, and my parents helped contribute to the remainder of the 20% deposit and offered to be guarantors. The First Home Owner Grant of $7,000 and the stamp duty exemption offered at the time helped as well.”

“For my first three properties I allowed them to be cross-collateralised … Had I defaulted on any of the loans, I’d be at risk of losing all three!”

Michael opted to move into the property to benefit from the grant, and then he focused on building a deposit for his next property purchase.

Buying into Mascot in 2009 was “the best move I believe I made”, he says.

“Back then the area was largely commercial, with warehouses and truck rental companies. Now the suburb is transformed into a modern maze of apartments, with plenty of spots to shop and eat and a Woolworths literally around the corner,” he says.

“I bought in at $448,000. If I were to sell today, the price would’ve doubled to around $900,000.”

His second and third properties were both off-the-plan apartments, which he signed on for in 2010; they settled in the same three-month period in late 2012 and early 2013.

“Fortunately the valuations and rental estimates came back favourable over the two-year construction period,” Michael says.

However, around this time he realised that he was making one of his first major property mistakes: all three properties were financed with the same bank, and all three loans were cross-collateralised.

To make matters worse, they had highly uncompetitive interest rates.

“For my first three properties I allowed them to be cross-collateralised with the same bank, due to my family’s brand loyalty with that particular local bank branch and manager. Had I defaulted on any of the loans, I’d have been at risk of losing all three properties to the bank!” Michael says.

“After consulting a broker later on, I realised how risky that was, as defaulting on one would’ve meant losing all three. I brought on board a mortgage broker to look at the situation, and he helped me sever the cross-collaterisation set-up, and refinanced all my loans out to other banks – both major and minor – at lower rates, while also releasing equity for use towards future investments.”

Refinancing out of that mess was “the best thing I’ve done on my investment journey”, Michael adds, particularly because all of his loans were refinanced at better rates by at least 0.5% each.

“I also ended up releasing about $300k in equity, which helped immensely towards my later purchases,” he says.

Rushing towards property no. 4

This period of restructuring his finances gave Michael some time to research his next investment.

Though he had plenty of time to find what he was looking for, the resulting transaction ended up being quite a quick process.

“It was somewhat of a rushed purchase of an 800sqm house at Point Clare on the Central Coast,” Michael says. “All parties had their reasons to rush, oddly enough – the owners were retirees and wanted to sell quickly to fund a holiday and downsize; the agent wanted to rush so she could get her commission and hand in her resignation; and I wanted to get in ahead of the looming APRA lending criteria mandates, which had been on the radar for quite a while by that point.”

Thanks to his broker’s work with restructuring his financing, Michael had the funds on hand for the deposit and stamp duty, and the green light to go ahead from at least one lender.

“My research showed that the area hadn’t grown much in the past decade, and given the recent price growth in Sydney there was good potential for investors to look further out. The biggest challenge was making sure the application was approved before my lender updated their lending criteria on APRA’s recommendation.”

All went smoothly and Michael was able to add his fourth property asset to his portfolio with minimal stress. However, it was his fifth purchase that started giving him headaches.

BEST INVESTING ADVICE MICHAEL EVER RECEIVED

BEST INVESTING ADVICE MICHAEL EVER RECEIVED

“During some months when bills are due or major repairs happen, I’d take a major loss and ask myself why anyone would stay put and losing money. I’d wonder: Am I cutting back on spending and holidays just for my investments to eat into my wallet?

“My dad gave a golden piece of advice, and that was to not sweat the immediate numbers and look at the bigger picture. Sure, you’re negatively geared and making a loss each and every month, but the value of your portfolio has risen by a higher amount. It was difficult initially to get comfortable with accepting an ongoing financial hit to achieve better results in the far future.”

Lady luck plays a role

Michael’s fifth and final purchase in Sydney’s Ryde was another off-the-plan purchase. The project settled in October 2016 and Michael had committed to the purchase in 2014.

Because he had outlaid a substantial deposit on the purchase two years earlier, he felt nervous as the new lending landscape was in effect by the time he was due to settle.

Because he had outlaid a substantial deposit on the purchase two years earlier, he felt nervous as the new lending landscape was in effect by the time he was due to settle.

“There’s a general saying that the first investment is the most difficult, but for me, I think this last one has been the most testing! I’d read in the news about families [who were] losing their deposits because they couldn’t get finance for their off-the-plan properties, and it kept me awake at night,” he says.

“I overcame this by taking a step back and looking at the bigger picture. If tight lending regulations meant I couldn’t uphold my side of the contract on the off-the-plan apartment, I’d lose my $60,000 deposit, which would hurt – a lot. However, while you can recoup your financial losses, one’s mental health and wellbeing from worrying all the time isn’t something you can regain.”

To manage the situation, Michael referred to a tried and true formula for success: he reached out to his mortgage broker, who looked at his situation, compared it to the preferences and quirks of both major and minor banks, and helped him find a lender that would furnish him with the 80% needed to settle.

This wasn’t Michael’s only crisis during his investing career. Over the years there have “definitely been challenges”, he admits, including a period when he tried to self-manage an investment property, and another situation in which he had to sack an unreliable property manager and attend tribunal mediation sessions to resolve disputes with tenants.

“I’ve also weathered periods when some of my properties would be vacant for months at a time,” he says.

“I’m a strong believer that it’s all well and good for other people to pass on their advice and words of caution, but the real lessons are learnt from stumbling for real and having to push through those challenging situations. You come out the other side a little stronger, and hopefully without too many new grey hairs!”

“Looking back, I have been extraordinarily lucky to have smooth experiences with off-the-plan apartments. There’s plenty written about the dangers of investing in off-the-plan, and I have no doubt that luck certainly played a role in my success with them,” he says.

Another key to Michael’s success has been his leveraging of depreciation to generate strong tax refunds.

“I always get a depreciation report done for my investment properties, as they enable large sum deductions, especially for newly built properties,” he says.

“While the reports can cost up to $600–$700, they pay for themselves the second your tax agent opens to the page where it shows several thousands worth of depreciations that can be claimed

at tax time. They are by far the most powerful documents to maximise your tax return and cash flow.”

When the banks say no

Michael is now kicking around a few ideas about what to do next.

“I’d like to buy a place in Brisbane, but I’m afraid my cash flow situation won’t be viewed favourably through the banks’ current serviceability calculators,” he says.

“Specifically, I know major banks will apply a 7.5% or more interest rate on all loans, which makes it difficult for investors like myself to qualify for a loan.”

If he were given the magic ability to hit the ‘restart’ button and begin again as an investor with the knowledge he has today, Michael admits he may have made a few different decisions. For instance, he says he would have looked interstate in areas such as Brisbane or Wollongong for his last few purchases, rather than diving deeper into the Sydney market, where yields are very low at present.

“If I’d bought in areas with high yields and strong cash flow, this would’ve helped buffer against the negative cash flow situation I’m currently in, which is making it difficult to borrow more in the current market,” he says.

To work around the banks’ reluctance to lend, Michael is considering a few alternative routes to boosting his property portfolio.

“There are several paths I’m looking at. I’m currently bouncing around the idea of selling one of the properties and using the profit to pay down my other loans to alleviate the cash flow issue. Or I might buy in another city where yield and cash flow are more appealing, such as certain areas of Brisbane,” he says.

He’s even investigating the idea of building a granny flat on his 800sqm Point Clare house, to boost his portfolio’s cash flow.

“However, none of these are concrete plans, so my next step is to run at idle – stay up to date on the news, stay in touch with my accountant and broker on industry changes, and play the waiting game.”

The last year was “quite testing” as Michael waited to see how his most recent off-the-plan purchase would pan out, but the experience has taught him “not to not worry about things outside of my control”.

Aged in his early 30s and with a net worth of around $1.1m, Michael also says he hasn’t planned too far ahead to retirement, although it’s “something I should look deeper into”.

“Apart from supplementing my retirement nest egg with passive income from property, I’d also like

to ensure my family, including my teenage sister, is well off enough to not have to worry about money for essential living,” he says.

“It’s comforting to know that, if needed, there are assets under my name that I can sell off in the worst-case scenario.”

• Look at your own finances

Review your income versus expenses each month. The numbers will never be fun to look at, but doing this initial check is essential to being able to put together a realistic savings plan to go towards the deposit for your first property.

• Buy interstate

When looking at places to invest in, consider cities and regions outside of where you live. Local property advice is only a phone call or email away to a property agent, and visiting a new city for the weekend can be turned into a mini getaway.

• Trust yourself in making decisions

If you feel like you’ve done the due diligence and the decision is in line with your overall plan, then go for it. It’s so easy to be overwhelmed by data, or horror investment stories from ‘friends of friends’. Do some research, talk to people who have more experience in investing, and if an opportunity comes up, make a decision to grab it or not. Either way, be committed to that choice.

• Qualify your experts

There are plenty of consultants who want your business – lending managers, financial planners, sales agents, mortgage brokers. Try to use those who actually have a property portfolio and experience to share with you. There are online forums, eg at yourinvestmentpropertymag. com.au, where here you can get sound advice.