There are not many things as nerve-wracking and stressful as when the ATO demands to see your books. David Shaw lists his top tips for staying out of trouble.

Investment properties

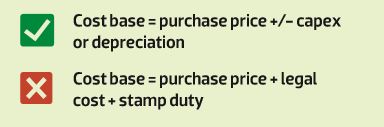

1. Reduction of the cost base of the assets by the amount of depreciation claimed

The CGT legislation allows for the depreciation that is claimed over the life of the property to be deducted from the cost base of the asset when calculating capital gain.

The cost base is the purchase price plus or minus additional capital expenditure or depreciation claimed.

More specifically, for properties built after March 1997 there is detailed legislation that requires building depreciation to be deducted from the cost base of the asset.

The mistake that is regularly identified is that the cost base used is the actual purchase price plus legal costs and stamp duty. The issue in this scenario is that there has been no reduction of the cost base due to depreciation in making the CGT calculation. Property investors need to be aware of this as the longer the property is owned the larger the mistakes that can be made.

2. Apportioning land and building value

In the event of a sale, not only must the depreciation be adjusted but the taxpayer (property owner) is required to commission a valuation to determine the land and building components of the sale. As the building content of the property is often depreciated beyond its market value, owners can face a situation in which the written-down value of the building is less than the market value of the building. This portion of the capital gain is not on the capital account and therefore becomes fully assessable. The capital gain on the land is still subject to the 50% discount but may not form the largest portion of the gain.

Principal place of residence

3. Moving into the property after purchase

It is important that the purchaser move into their principal place of residence (PPOR) as soon as possible after purchase, in order to qualify for the CGT exemption on a PPOR. If there is a current tenant at the time of purchase it may be better to release the tenant from the lease prior to settlement.

FACT: There have been court decisions in which owners of properties have been liable for some CGT because the properties were rented for only a few weeks prior to the owners moving in, as the courts declared that they did not move into their properties as soon as practicable after settlement.

4. Six-year absence rule

This can only be exercised when the taxpayer can demonstrate that the property was initially their PPOR. If the property owner satisfies the requirements of this rule, they may be able to rent their property out for up to six years with no CGT consequences.

If the property is sold within that six years and the property owner has not nominated another PPOR during this time, they can exercise this exemption. In fact, if a taxpayer moves back into the property within that six-year period, then the six-year period can be restarted if they move back out again at a later date. Therefore living in the property initially may produce a vastly superior result in the event of a capital gain.

5. Market value rule

This method can only be used if the property owner (taxpayer) can demonstrate that their property was initially a PPOR. This method allows the property owner to value their PPOR when the property ceases to be their PPOR, and this value will form the cost base of the asset rather than the cost base being based on the initial purchase price.

The rule can also be applied when the property is sold, if both new and old PPORs are involved. There is an opportunity to defer capital gains to a future point in time if the old PPOR is elected as the main residence. However, this will result in more CGT to pay once the new PPOR is sold, but that could be many years down the track.

6. Daily apportionment method

If a taxpayer does not live in the property initially, there will be no entitlement to use the six-year absence rule or the market value rule. Property owners will, however, be entitled to use the daily apportionment rule, which will entitle them to apportion a capital gain based on the number of days the property was their PPOR and the number of days the property was not their PPOR. For example, if a property was only a PPOR for half of the ownership period, this would entitle the taxpayer to reduce the capital gain by 50% before any additional discounts are applied.

7. Two-hectare rule

The two-hectare rule allows a taxpayer to have their entire plot of land covered by the PPOR exemption – but be aware that if the land your PPOR is constructed on is more than two hectares you will not be entitled to the PPOR exemption for the whole property.

The portion of the land value over two hectares will need to be excluded from the PPOR exemption in the event of a sale. The portion of land between the house and the first two hectares will be exempt from CGT. For example, on a four-hectare lot a capital gain of up to 50% may be taxable. The portion of the gain related to the two hectares on which the house is situated can be deducted from the capital gain, and then the 50% discount can still be applied if the asset is held for more than 12 months.

8. Part usage rules

Taxpayers often overlook the fact that if they run a business from their property they will not be able to use the PPOR exemption for the whole property. If eligible, they can, however, utilise the CGT and small business exemptions to reduce the capital gain.

Holiday house

9. Adding costs not deducted to the cost base of the asset

Taxpayers should note that if deductions are not claimed either in part or in full, these can be added to the capital cost of the asset in calculating a future capital gain. It is therefore important that all relevant documentation is kept so the cost base of the asset can be easily calculated.

Examples of such costs include council rates, water rates and insurance policies.

Property renovations

10. A profit-making sche,e is not always capital

Often property owners (taxpayers) have the mistaken belief that if they purchase a property, renovate this property and then hold the property for just over a year, any sale will then be on the capital account and the taxpayer will be entitled to a 50% discount.

The ATO, however, views these transactions very differently as they look at the intention of the transaction. That is, if the property is purchased with an intention to sell, the ATO will be of the view that when this property is sold the gain on the sale will be on the revenue account and hence will be fully assessable in the taxpayer’s income.

To clarify, the taxpayer will not be entitled to the 50% CGT discount; however, they will only be assessed on the profit when the property settles as opposed to the exchange date, which is the case in the event of a capital gain.

Taxpayers who are also builders employed in the building industry, or have a history of regular transactions in the development or refurbishment of properties, may be less likely to qualify for having the transaction on the capital account. The ATO has the benefit of history and access to property sale records, so if you are in a risk category, get the right advice to make sure the property transaction is structured on the capital account.

Properties used in the family business

11. Extra CGT benefits

Since the CGT small-business exemptions were introduced in 1999, properties used in a taxpayer’s business can have concessions in addition to the 50% CGT discount. The taxpayer (property owner) may be entitled to an additional 50% discount on the remaining capital gain (active asset discount), effectively resulting in a 75% discount.

The remaining capital gain is eligible for the retirement exemption (lifetime limit of $500,000), where the capital gain can be deposited into superannuation if the taxpayer is over 55. Afterwards, the taxpayer can receive this portion of the CGT free.

There may also be an opportunity to roll over the last 25% of the capital gain into another business, providing this is done within two years of the capital gain being incurred. Be careful, however, to get the correct advice as to the eligibility of the active asset discount as the property must be used in the business for at least half of the ownership period or at least seven and a half years if the property is owned for more than 15 years in total.

These exemptions are generous, but compliance is strict, so seek professional advice when applying these discounts.

Inheritance of properties

12. Issues with the family home as opposed to the investment property

Property owners should be aware of the history of the property inherited, as the tax consequences in the event of a sale could have a huge impact on future finances. In short, a PPOR, or a pre-CGT property (purchased before September 1985), will be inherited at market value as of the date of death, and family members have two years from the date of death to sell the property with no CGT consequences.

With an investment property, this is an entirely different story. The investment property is inherited by the beneficiaries at the same cost base as the cost paid by the deceased for the property. If the property has been depreciated over many years, the cost base could be very low, and hence a huge capital gain will accrue in the event of a sale, even if the sale is between family members as a full or partial sale.

Remember Capital gain is always generated on the date of exchange. Therefore a property owner who is selling their property should consider timing the sale to avoid it adding to other significant assessable income for that period.

Tips for reducing CGT

-Make sure you keep accurate records of all costs in relation to the purchase and sale of your asset

-Make sure you carefully make note of any time that you have lived in an investment property as this may further reduce your capital gain

-Where an asset, such as a holiday house, is not rented out, make sure that all holding costs such as interest, council rates and insurances, for example, are recorded, with back-up documentation kept, as this can reduce the capital gain

-Since CGT is based on contract exchange dates, make sure you exchange contracts, wherever possible, in a later financial year (eg July of a given year) to give you maximum time to work out how other deductions can be apportioned.

David Shaw

is CEO of WSC Group and has over 25 years’ business experience and extensive knowledge of commerce, industry and public practice accounting.

While due care is taken, the viewpoints expressed by contributors do not necessarily reflect the opinions of Your Investment Property.