Possibly the most important story for Australian real estate in 2021 will be an all-time record high increase in household rents and a dire shortage of accommodation for people to live in.

Propertyology’s claim is in complete contrast to the cast of thousands who still think that the housing demand consequences of 220,000 overseas migrants [net 10-year annual average] not arriving in Australia will cause a downturn to property markets.

The reality is that Australia does not have enough housing supply for its existing 25.6 million population. Propertyology is predicting that these next couple of years will produce the biggest increase in rents that Australia has seen in living memory!

To secure a standard rental property over the next couple of years, it will not be uncommon for households to need to find an extra $2,000 to $5,000 per annum.

Depending on which side of the fence you sit, this represents a big challenge or an extremely exciting opportunity.

Most of Australia had an under-supply of housing (for sale and for rent) prior to COVID-19. While this germ has managed to cause quite a bit of inconvenience for Australian lifestyles, no germ has the ability to dump thousands of extra dwellings out of the sky. In other words, Australia is still under-supplied!

One really should not be surprised be this announcement. For more than a year, Propertyology has produced quite a bit of evidence alerting people to Australia’s widespread under-supply.

30 October 2019: Rental trends point towards changing market cycle

25 November 2019: $5000 annual rent increase not out of the question

16 March 2020: Rising rents to draw investors out of hibernation

4 June 2020: Foot traffic points to capital city exodus

23 July 2020: 75 percent of Australia is under supplied

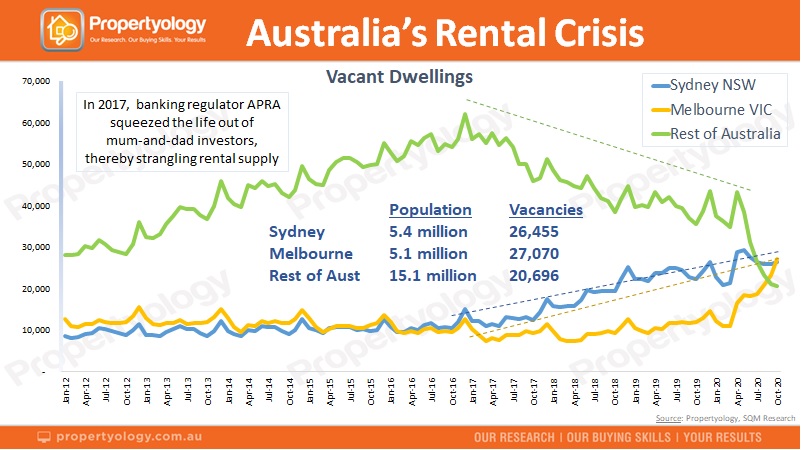

While Australia’s two biggest cities currently have a surplus of rental stock and falling rents, it is a very different story for pretty much every other location in Australia.

As at the end of October 2020, there was a combined 53,525 dwellings advertised for rent for Sydney and Melbourne’s combined population of 10.5 million people. The remaining 15.1 million Australians are competing in bidding wars for just 20,696 dwellings in the other six capital cities and the increasingly popular regional wonders.

COVID-19 cannot be blamed for everything. A health pandemic is not responsible for a lack of housing.

If anything, the societal reaction to lifestyle restrictions caused by this germ has merely transferred housing demand from locations like Sydney and Melbourne to others. But the pressure on Australian rents (exc Sydney and Melbourne) was building well before COVID-19!

Fact: it is becoming standard practice for property managers in every corner of the country to frequently receive numerous applications to rent a standard house. The intense pressure affords property managers the luxury of being particularly fussy when assessing the quality of tenant applications.

Propertyology’s buyer’s agents have seen firsthand proof of multi-offer tenant applications and the successful tenant paying $50 to $70 per week above the market’s median rent. It’s a frenzy!

5 out of 8 capital cities currently have a vacancy rate below 1 percent. The pressure is intense!

From Maitland NSW, to Margaret River WA, Mount Gambier SA, Mackay QLD, and Mildura VIC, Propertyology is tracking an additional 50 individual towns across Australia with vacancy rates below 1 percent. It is the tightest rental conditions that Australia has ever seen. Anyone who forecast a downturn clearly has no clue what ‘housing demand’ truly means!

There are reports of families living in tents and caravans because there’s nothing available for them to rent.

The potentially significant increase to rental income is great news for those Australians who have chosen to be proactive and invest in their future financial independence.

For a lot of locations, the rent increases that are now expected is long overdue.

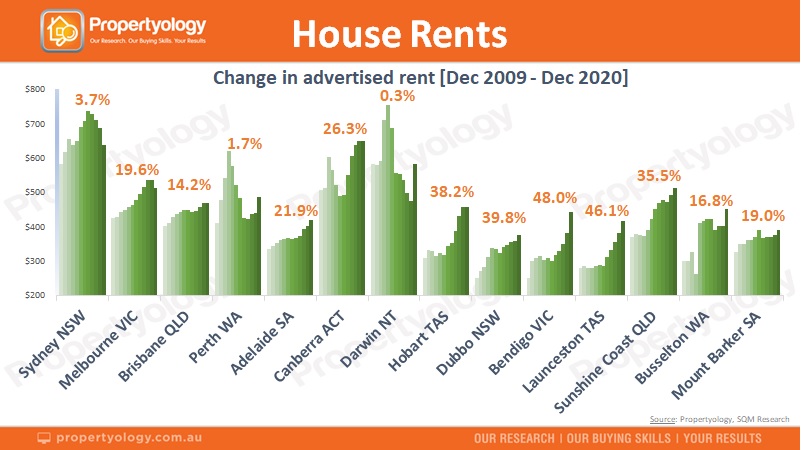

According to data by SQM Research, Canberra ($648 per week), Sydney ($638) and Darwin ($580) have the highest capital city advertised medians rents for houses.

Hobart rents have increased the most over the last decade, although they are still relatively affordable at $456 per week.

The biggest rent increases over the last decade are in locations outside of capital cities. The above chart contains just a few samples.

With employment and lifestyle opportunities driving accelerated demand, these locations are likely to continue to produce the highest rent increases.

The two biggest influences on rental demand are local economic conditions and affordability.

The supply side is 98 percent determined by the behaviour of mum-and-dad property investors. The federal and state governments find it difficult enough to fund infrastructure let alone rental accommodation.

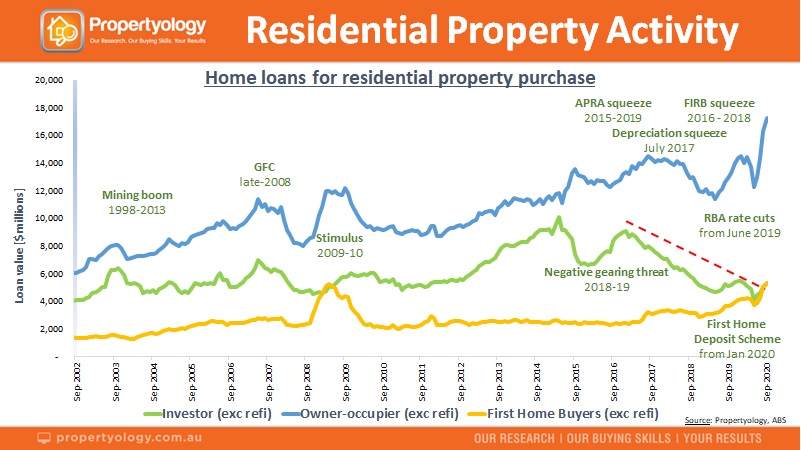

The primary reason for Australia’s current rental supply crisis is traced back to a series of decisions between 2015 and 2019 by the banking regulator to restrain the activity mum-and-dad investors.

Property investors were active participants during Sydney and Melbourne’s last boom, ending in 2017. But APRA’s credit tightening policies were applied with a broad brush that, instead of two cities, affected all of Australia.

Propertyology was unapologetically critical of the policies at the time, stating that there would be unintended consequences to be felt for years to come.

Significant upward pressure on household rents due to insufficient mum-and-dad investors being able to add to the rental supply pool is ‘Exhibit A’. The trend lines in Chart 1 (above) and Chart 3 (below) proves or point.

A lack of rental supply has caused this problem.

The only viable solution are the everyday Aussie mum-and-dads whom have a desire to not be reliant upon a miserly taxpayer-funded aged pension in retirement.

This problem will get worse before it gets better.

The only way to address it is to support those who generate 98 percent of Australia’s rental supply:

- APRA must treat adults as adults and introduce a credit policy which supports responsible borrowers. Moreover, they must be proactive in helping to improve loan application efficiencies. With modern technology and so much information at bank’s fingertips, it beggers belief that something which could be approved within a couple of days 30-years ago today takes a few weeks.

- Banks must stop charging investors a premium interest rate.

- State governments must stop charging investors higher stamp duty and placing a wad of moratoriums and restrictions on what an owner can do with their asset.

- City councils must stop charging investors a premium on council rates.

- The federal government must conduct a serious investigation into the conduct of insurance companies. From charging excessive insurance premiums to hiding behind fine print when a policyholder makes a claim, rorting of real estate products is a national problem.

......................................................................

Simon Pressley is Head of Property Market Research and Managing Director at Propertyology.

Simon Pressley is Head of Property Market Research and Managing Director at Propertyology.

Propertyology is a national property market researcher and buyer’s agency, helping everyday people to invest in strategically-chosen locations all over Australia. The multi-award-winning firm’s success includes being a finalist in the 2017 Telstra Business Awards and 2018 winner of Buyer’s Agency of the Year in REIQ Awards For Excellence.

Disclaimer: while due care is taken, the viewpoints expressed by contributors do not necessarily reflect the opinions of Your Investment Property.