The buzzing activity at open homes and auctions currently observed at the coalface is little more than a couple of misleading metrics which act as a smokescreen for Melbourne’s fragile property market fundamentals, according to Propertyology.

Those with an interest in Melbourne’s property market would be wise to stand back from today’s metrics-of-the-moment and objectively assess the fundamentals.

“Melbourne’s weak economy, declining population, record high rental supply, and the ratchetting up of new housing construction are a collective group of fundamentals that are as weak as what Darwin and Perth saw throughout the last decade,” said Propertyology Head of Research, Simon Pressley.

The national property market research firm and buyer’s agency anticipates that resale listing volumes will continue to trend higher from Q2 2021 onwards and the current upward pressure on asset values will ease with it.

The Victorian state government’s new property taxes certainly wont help the cocktail of concerning leading indicators which will shape the medium-term outlook for Melbourne real estate.

“We cannot rule out the possibility of declines in Melbourne house prices over the coming two years, particularly if APRA intervened and tightened credit policy (although we are vehemently opposed to any such action).”

And the prospect of any meaningful capital growth on apartments is “totally buggered!”

“From a financial perspective, there is undeniable proof that this asset class was already extremely problematic well before the arrival of the germ - now it is stuffed!”

Housing supply excess

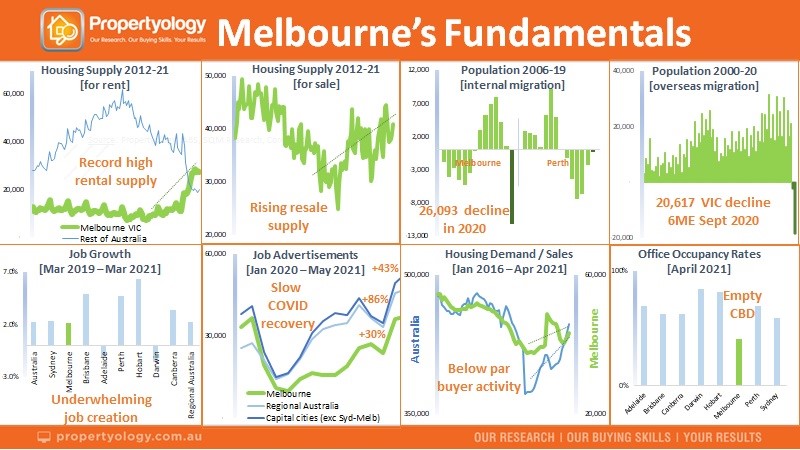

Research by Propertyology confirms the volume of dwellings advertised for rent in Melbourne has increased from 11,091 in March 2020 to a record high 25,050.

“That is enough housing supply for an entire city the size of Launceston or Shepparton.”

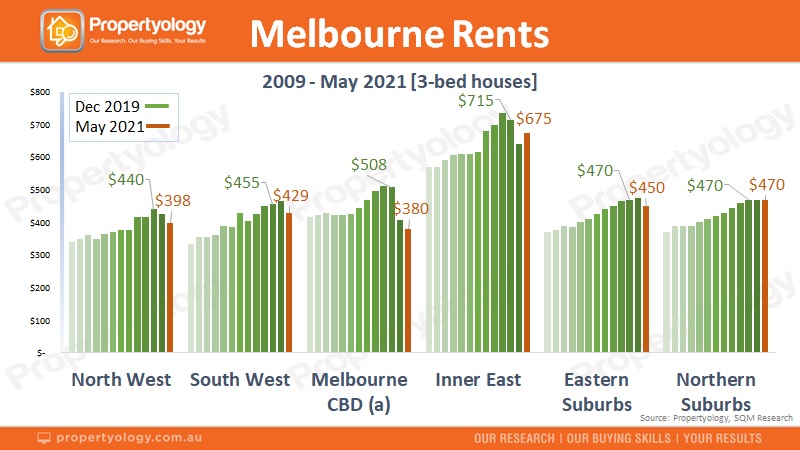

Mr Pressley said that in addition to the plethora of empty CBD apartments, there has also been a softening in suburban rents, particularly in Melbourne’s inner-east and north-west (in both cases, advertised rents for 3-bedroom houses have declined by $40 per week, or $2,000 annually).

The 40,958 dwellings listed for sale on 30 April 2021 was already 18.9 percent higher than 12-months ago and a significantly bigger supply increase than any other capital city.

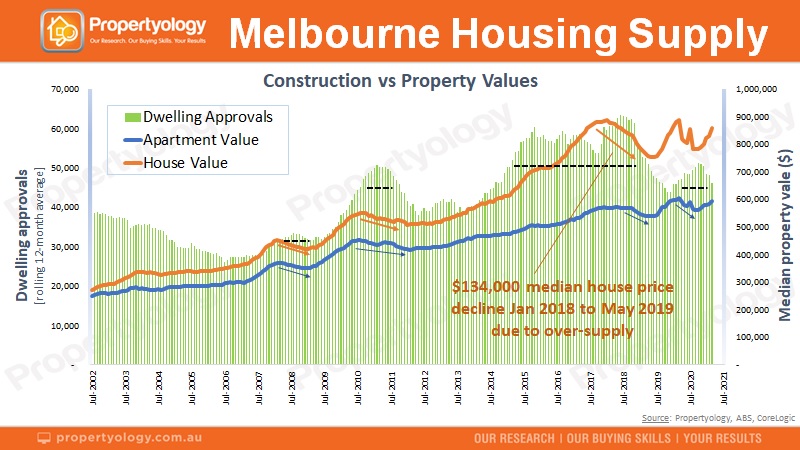

The final piece to housing supply is new construction.

“Construction has always been integral to Melbourne’s economy. Stimulating this sector at a time when the population is effectively declining, and other economic factors are fragile, is not a recipe for property price growth,” said the highly respected national property market analyst.

Melbourne’s pre-COVID housing supply pipeline was already running at circa 45,000 extra dwellings per year and the Andrew’s state government economic recovery plan is to crank things up.

“It is not that long ago that Melbourne suffered a property market downturn caused by an over-stimulated construction sector. Melbourne’s median house price declined by $134,000 between January 2018 and May 2019.”

Housing demand is dangerously delicate

The 70,000 to 80,000 overseas migrants that normally add to Melbourne’s annual housing demand ceased in March 2020.

“The latest ABS data shows that Victoria produced negative net overseas migration of 20,617 over just 6-months to September 2020, and there is still no sign of the population ‘front door’ re-opening any time soon,” said Mr Pressley.

While Melbourne was in its 4-month lockdown, Propertyology flagged the possibility of 30,000 (net) residents leaving Melbourne over 2-years via the ‘back door’. Today’s data confirms that 26,000 have already left in just 12-months.

From overseas and internal migration, Melbourne’s population has effectively declined over the last 12-months.

“The impact of Melbourne’s 4-month lockdown reminds us of what happened in Perth in 2014 when commodity prices tanked, inflicting several years of pain. Both economic events marked the beginning of a sharp reversal in migration patterns,” said Propertyology’s Head of Research.

“The diminished housing demand is one thing, but the billions of lost revenue from those who left town, going on to spend their household budget elsewhere has just as much impact on a city’s property market.”

Perth’s property market trough lasted 6-years and property values have only just returned to where they were 10-years ago.

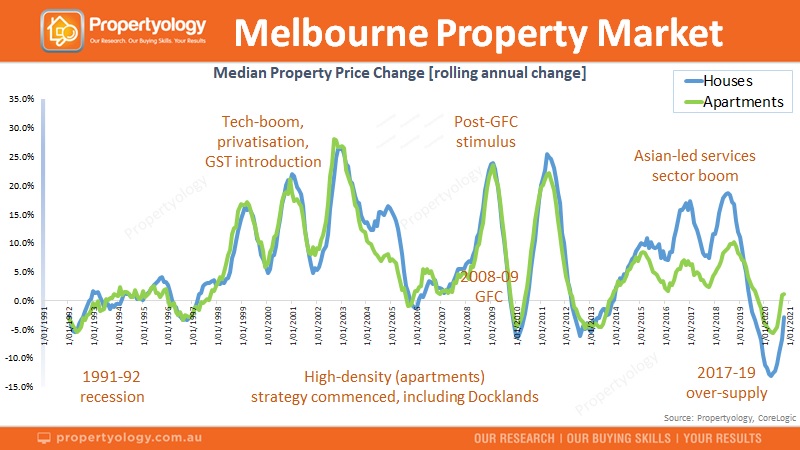

Pressley says “…at an individual city level, the two biggest influences on a property market have always been the performance of its economy and the volume of new housing construction.”

“Let us not forget that it was Melbourne’s soft economy that produced a 7.5 percent decline in its median house price over the 2-years ending August 2012.”

Propertyology describes Melbourne’s economic outlook as “shaky as any location in Australia”.

- Between domestic and overseas visitors, Melbourne’s economy used to play host to 11 million visitors that spent $10 billion annually. Unfortunately, the international border closure, combined with domestic concern associated with travelling to densely populated cities, will create pain for the economy of this great global city for some years yet.

- Pre-COVID-19, 200,000 international students were living in Victoria, each of them requiring long-term rental accommodation and spending circa $50,000 per annum in the local economy - not now!

- Melbourne CBD’s office occupancy rate of 40 percent is miles lower than every other capital city.

- Without the tourists, students and office workers frequenting Melbourne’s inner-city for months on end, there are thousands of retail and service industry businesses battling to survive.

- Relative to the rest of Australia, official data confirms that the total volume of jobs in Melbourne in March 2021 compared to 2-years earlier is underwhelming. And the change in the volume of new jobs advertised in April 2021 (a leading economic indicator) is well down on the rest of Australia.

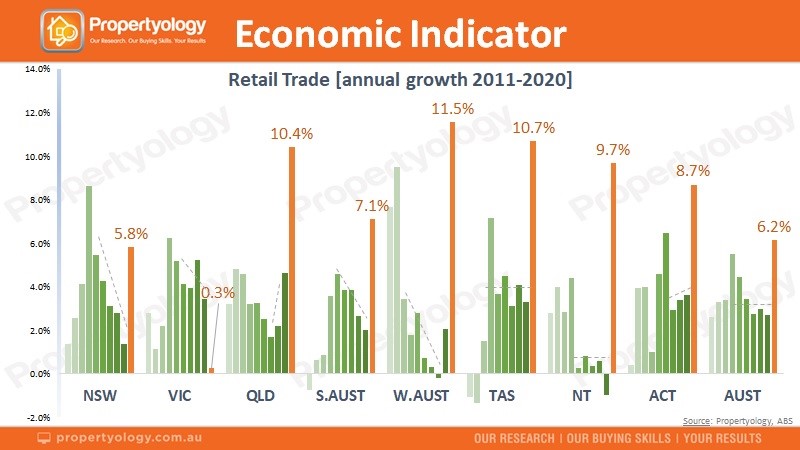

- The comparison of Victoria’s retail trade revenue to other states in the below graphic is stark.

Pressley said “the tax increases in this month’s State Budget is a sign of what lies ahead for Victoria. Sky-high state government debt places long-term restrictions on funding for infrastructure and industry support, thereby suppressing economic growth and property markets with it. Just look at Queensland’s performance over the last decade.”

......................................................................

Simon Pressley is Head of Property Market Research and Managing Director at Propertyology.

Simon Pressley is Head of Property Market Research and Managing Director at Propertyology.

Propertyology is a national property market researcher and buyer’s agency, helping everyday people to invest in strategically-chosen locations all over Australia. The multi-award-winning firm’s success includes being a finalist in the 2017 Telstra Business Awards and 2018 winner of Buyer’s Agency of the Year in REIQ Awards For Excellence.

Disclaimer: while due care is taken, the viewpoints expressed by contributors do not necessarily reflect the opinions of Your Investment Property.