Financing a property is one of the biggest challenges for a buyer. However, providing finance also comes at a risk for lenders, as they could come out on the losing side if a borrower goes MIA or is unable to make their mortgage repayments.

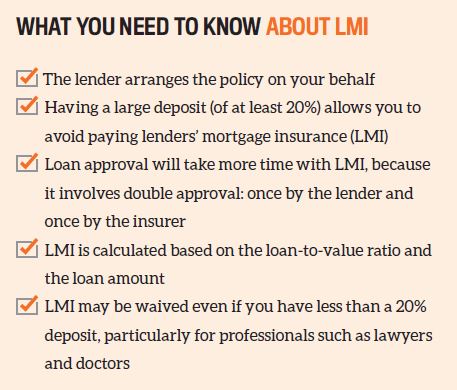

For this reason, lenders ensure they are covered by lenders’ mortgage insurance (LMI) when a loan is taken out, typically if the amount being borrowed is more than 80% of the property’s value.

While LMI protects the lender alone, it is an expense many investors are willing to take on as it also gives them an advantage

LMI also helps ensure that the borrower is able to take on the financial responsibility, as LMI insurers will check for eligibility based on whether a borrower is capable of making the monthly repayments.

While LMI protects the lender alone, it is an expense many investors are willing to take on as it also gives them an advantage. The usual deposit on a home loan that a buyer needs to make is 20% of the purchase price, but with LMI some lenders are more willing to take lower deposits, thanks to the safety net it provides. As a result, buyers are able to purchase properties more quickly.

Before taking out LMI, these are some things investors need to take note of:

1. In the event of loss, this insurance only protects the lender

It provides coverage for your mortgage repayments, which will be paid to the bank in the event that you default on your loan. If this happens, the insurer will then chase you up for the funds.

2. It is tax deductible on an investment property

Section 25.25 of the Income Tax Assessment Act 1997 indicates that the full LMI premium, including stamp duty and GST, is tax deductible as a borrowing cost. If LMI is incurred halfway through the year, the deductible portion corresponds to the period of days that the property was available on the rental market.

3. It can’t be claimed right away

Instead, LMI must be claimed over a period of five years, starting from the date of settlement. Borrowing costs can only be claimed in the same year they were incurred if the expense was less than $100.

When the property is sold, the LMI can also be claimed against capital gains tax, if there’s any.

4. Adding LMI to your loan is not advisable

Why? Because it costs you a lot in the long run. On the surface, incorporating LMI into the loan amount seems less painful as you don’t have to find the funds right away, and the premium remains a deductible expense. However, you may then be paying interest on that LMI premium for 30 years. A $10,000 LMI premium at 4% will cost you $400 per year in interest alone. Multiply this by 30 years and your premium suddenly gets very expensive.

5. If you convert your PPOR to an investment, you can claim LMI

However, note that you can only claim LMI for the period the property is rented out. For instance, if you rented out your principal place of residence six months after purchasing it, you could only claim the LMI for 4.5 years.