Your own home is arguably the first real estate investment many people make. But is buckling down and making extra repayments on your mortgage the best way to get ahead financially – or should you invest sooner and make bigger gains? Nina Cuturic reports

As a borrower, your perception of debt plays a large role in determining how you will manage your loan and time your entry into real estate as an investment.

Generally, for the debt- or risk-averse, keeping ahead of your home loan repayments where possible, before even considering going down the investment route, harbours a degree of comfort and certainty – and it’s a wave that they would prefer to ride out until they own their home outright.

But while submitting the final monthly repayment slip is indeed a momentous victory, understanding the fuller potential of your personal place of residence (PPOR) – even while you pay it down – could see you taking greater financial steps forward, says Michael Beresford, director of investment services at OpenCorp.

“Investing is necessary to improve your financial situation, and if you take a long-term approach with whatever you invest in, you will do very well at it,” Beresford says.

“Your mindset needs to be adjusted, and that’s where a [financial] coach and a mentor can assist you and hold your hand on that journey and empower you to understand what the options are and what’s going to work for you.”

“It’s all about being able to create your own capital growth, as opposed to potentially purchasing somebody else’s capital growth”

Beresford adds that the effectiveness of a strategy that catapults off the equity in your PPOR will depend on the location of the property, the equity and where it comes from, the skill set of the investor, and their borrowing capacity.

That said, leveraging what you’ve already got is a great way to get started as a property investor – and one that you may want to consider sooner rather than later.

Invest first or pay off your own home?

When asked why some borrowers are more inclined to pay off their home loan first before they consider investing, Drew Evans, director of Caifu Property, suggests it comes down to their personal attitude towards debt.“

When asked why some borrowers are more inclined to pay off their home loan first before they consider investing, Drew Evans, director of Caifu Property, suggests it comes down to their personal attitude towards debt.“

A lot of clients have that mentality where they want to pay their debt quickly and then get into the next one, which they will pay down before they get the next one – but I guess for me it comes down to effectively using your money to get your money to work hard for you,” he says.

“If you can put a plan in place where you can strategise between having your own home and then also controlling investments that produce cash flow and huge chunks of equity, then you realise that you can actually do both at the same time and get a much, much better result a whole lot quicker.”

So what are the options available?

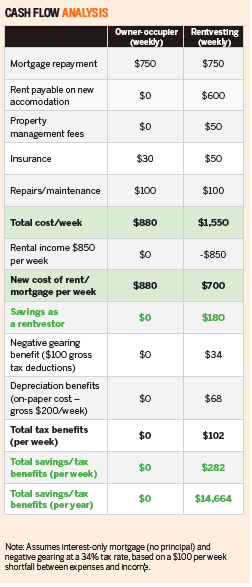

One of the more popular recent strategies is to move out of your PPOR, put it up for rent, and rent out a property yourself (also known as ‘rentvesting’). This is at the extreme end of making your money work harder for you. It might sound like you’re about to take a step backwards when moving out of your prized home to rejoin the rental pool, but over the long term it can put you in a far better financial position.

By converting your PPOR into an investment property, you can generate a steady flow of rental income and access depreciation and tax benefits, which give you additional cash flow – even more so if you choose to rent in an affordable suburb.

This type of strategy could see you pocket hundreds of dollars, or perhaps even thousands, per month.

It was this strategy that allowed Evans to live in a suburb that he wasn’t able to afford to buy in but could afford to rent in. It also set the tone for his future buying capacity.

“I was very fortunate in those five years of renting because I was able to invest in real estate and generate huge amounts of equity as well as positive cash flow, while living in a suburb that I couldn’t afford to buy in,” Evans says.

“So now I’ve actually purchased my dream home on the border [of Sydney] – and fast-forward probably to the end of next year I am aiming to be completely debt-free [on my PPOR mortgage] at the age of 33 – by using that exact strategy.”

Striking the right balance

Building an investment portfolio that includes renting out your PPOR can be “really powerful”, says Beresford, who took up ‘rentvesting’ himself until his mid-30s.

“It’s the best way to be able to hold more properties and build a greater asset base with greater asset value and as little cash flow out of your pocket as possible,” he explains.

“You would want to make sure that selling your PPOR is done for the right financial or lifestyle reasons, as opposed to just selling it for cash deposits”

“You have complete choice around what you do [with the extra cash flow] – whether you spend a little bit, maybe on a holiday or on something lifestyle-related, or put it in an offset account and reduce the interest that you are paying on your mortgage and grow your cash buffer towards future deposits for investments as well.”

However, Beresford says the success of this strategy boils down to “the amount of assets that you can hold for the cash flow”.

The investor also needs to be comfortable with losing the flexibility they once had as an owner-occupier, and although they open themselves up to the scenario of needing to vacate a rental if the owner decides to sell, this can be managed by signing into longer lease terms.

“The main thing that you need to consider, though, is what the holding costs are in each different scenario,” Beresford says.

“Depending on how much your mortgage is, and obviously with low interest rates right now, what your mortgage repayment is compared to the amount of rent that you would be paying is key. You want to make sure that the rent you are paying and the holding costs of an investment portfolio are not putting a strain on your cash flow.”

If rentvesting is not for you, you may consider selling your PPOR and using the profits from the sale to purchase an investment property while you rent out a property yourself.

“You would want to make sure that selling your PPOR is done for the right financial or lifestyle reasons, as opposed to just selling it for cash deposits,” Beresford warns.

He also considers this option to be not quite as “powerful” as rentvesting, whereby the equity in your PPOR leverages you into investments.

“The only reason that you would sell your own home is based on market cycles: the location of that property has just been through a major boom and you can maximise your sale price, and it doesn’t make sense to hold that asset long term,” Beresford explains.

“Selling your PPOR in that instance would allow you to get better exposure to assets that would grow in value, if your own home is not in a location that you think will be growing in time, or will not be growing by as much.”

Taking on a renovation

Selling your PPOR and using the profits to purchase an affordable property that is in need of a facelift could see you pocketing a profit once you renovate it and sell it on.

There’s also the option to live in the property being renovated, in order to pull back on the rental costs of living elsewhere. This would give you additional funds you could use to add more value to the renovation itself.

But depending on the scale of the project, a renovation can also require you to become familiar with the margins and fundamentals of constructing and developing.

“It’s all about being able to create your own capital growth, as opposed to potentially purchasing somebody else’s capital growth,” Evans says.

“Think big and then start small. It’s about looking for somebody who’s already done what you want to do and taking them on as a mentor. It’s about making sure you don’t bite off more than you can chew, because, let’s face it, developing is not an exact science no matter how experienced you are – things pop up.”

The borrower could potentially add more value to the renovated property than what their PPOR would grow by in the same space of time, Beresford says. However, considering that a lot of effort, time and money goes into achieving that outcome, as well as the additional costs that need to be covered by the sale, Beresford says “it’s not [an option] that I would recommend for the majority of people”.

“Understanding the market, doing a detailed feasibility to understand the opportunity, and ensuring that you get your timing right is fundamental, because there are a lot of moving parts here that can impact the profit you make,” he explains.

“Then you need to understand how you are going to utilise the renovated property to further grow your portfolio after that.”

If you’re planning to sell the renovated property in order to buy another one that you can renovate and thus continue the profi t-making process, Beresford says this will mean further selling costs and potentially capital gains tax.

In the case of revaluing the property post-renovation to draw the equity out, he adds, “What you need to understand is: what is the optimal amount of money to spend on the renovation to maximise the valuation based on the other properties in the area and what’s selling?

“You also need to consider what the market will be doing after the renovation [period],” he says. “If the market is not as strong, then that’s going to erode your profi t, and your risk would increase dramatically.”

Checking in on your home loan

Ensuring that the home loan on your PPOR is working in your favour is as essential as considering the strategies that could allow your home to propel you into investing.

"In a constantly changing lending environment, one of the risks is that people take their eye off the ball and get comfortable with what they’ve got in terms of their loan. They don’t review it regularly,” Beresford says.

“We have had stories of clients who have a couple of properties and their own home and we’ve saved them $20k a year through a refinance just by helping keep their finger on the pulse in regard to what’s available.”

For borrowers who may be reluctant to service more than one loan, Beresford adds that it’s important to understand the difference between good debt and bad debt.

“The debt on the investment property, for example, brings a significant amount of rent and ideally a significant amount of tax benefit back into the investor’s pocket, which is money that can be used to service the debt,” Beresford explains.

However, with each individual’s situation being different, he advises that borrowers seek professional advice on the options available to them.

According to Evans, investors should also spend some time working out how much they can realistically afford to put towards investing in a way that sets them up financially.

“I think that’s the big shift in psychology. A lot of people, when they first start up, see having both PPOR and investment debt as a negative, and they don’t actually see what it’s going to do for them in the long term,” Evans says.

“Don’t borrow more money than you can afford; make sure you focus on your cash flow commitments in relation to your outgoings; and put both personal and property buffers in place to make sure that if the ‘what if’ happens, you’re going to be fully protected.”

‘HOW I PAY JUST $300 PER MONTH ON MY MORTGAGE'

In 2012, Dean Zarif purchased a three-bedroom, one-bathroom house in Currumbin Waters on the Gold Coast that was infested with termites.

“I lived in it for almost a year whilst completely stripping it out and converting it to four bedrooms and three bathrooms with two en suites, during the rebuild,” Dean says.

He purchased the original house for $280,000, and the total renovation costs amounted to $80,000. The newly renovated property was sold for a handsome $480,000 a year after the initial purchase.

Prior to starting the renovation, Dean gained the expert advice of local agents in the area and scoured countless open homes to become familiar with the local competition and how other properties had approached an upscaling.

“We finally set a realistic budget, with a 15% contingency for unforeseen expenses, and made sure we focused on key areas so as to not overcapitalise,” Dean says.

“Speaking to local agents gave us a good idea of what needed to be done to achieve the best possible sale price.”

Dean says living in the property during the renovation meant that there were no rental expenses, which allowed him to focus on the mortgage and renovation costs. There was also no travel time spent going to and from the work site each day, which made for a quicker build, but the challenges included having to manage the constant dust and debris. He worked on the project for around 20 weeks in total, treating it as his full-time job.

In addition to taking on similar renovation projects, Dean has also converted part of his PPOR in Hamilton, Queensland, into a two-bedroom unit with separate electricity and gas, which allows him to rent out the upstairs section while he continues to live downstairs.

“I get $395 per week for the top level of my PPOR, and my mortgage is a little over $2,000 a month, so the majority is covered by my upstairs tenant,” he says.