03/12/2018

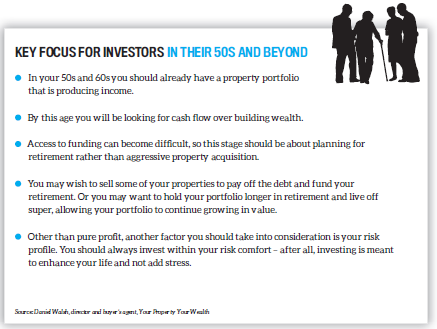

This is it: make or break time. Without being too dramatic about it, once you’ve blown out more than 50 candles on your birthday cake, your timeline for successful property investing is shrinking.

Drew Evans, director at Caifu Property, reiterates that this is “your last chance” – so making the right investing decisions is vital.

“Borrowing is getting tough in your 50s, so you don’t have time to waste, and you can’t afford to make a mistake,” he says.

“Consider: have you hit your goals or is it time to put the accelerator down? You need to do deals that generate equity right now, rather than buy and hold, because you’ll be over 60 by the time you discover if it was a good buy or not.”

In other words, this is not a time to go defensive and play it safe.

“By this stage you’re experienced and should know how to create equity. This is the time to get those last few deals under your belt and capitalise on your experience and knowledge,” Evans says.

“Doing just two or three highly profitable deals in your 50s can pay for an overseas holiday every year throughout your retirement – they could completely change the game for you.”

Your investing purpose

To create fast wealth, some investors at this stage will be considering more aggressive approaches to investing. But if you already own properties and they’ve appreciated in value, this is the point when you should start to become more conservative as you weigh up whether to consolidate or accumulate.

“Many investors place a foot in each camp – one in the ‘consolidate’ camp, where they focus on protecting the wealth they have built to date, and another in the ‘accumulate’ camp, where they ensure that they are still optimising their wealth creation capacity through ongoing and often-diversified investing,” explains Paul Wilson from We Find Houses.

“They may now have more disposable income after paying off their own home and their kids have become financially independent. At some stage during this time, you will most likely experience a reduction in your regular income as you reduce your hours of work or retire from the workforce. This will also impact on how the banks assess your ability to borrow money for future investing.”

Additional investment strategies will generally be focused on shorter-term and often more liquid styles of investing the capital you have access to, rather than using borrowed funds, Wilson says.

“There is a balance between being too safe, and acting impulsively. You might syphon off some capital to be held in a safe cash account, with another portion to be used for ongoing investment opportunities so you can still continue to grow your capital,” he says.

“Ultimately, if you started investing in your 30s, you would have between 20 and 30 years of investing behind you, and you can consolidate by selling the properties you don’t want to keep. You can then use these funds to pay down any debt remaining on the properties you want to hold, for the purpose of generating ongoing income in retirement.”

It’s never too late

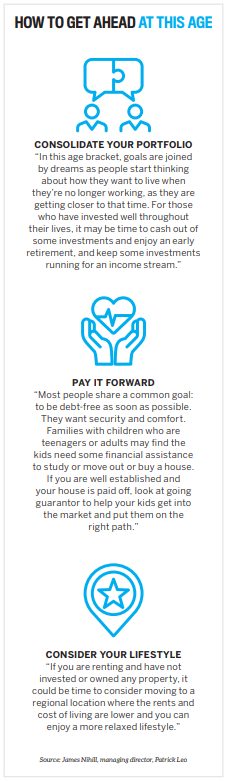

While you may have reached your ‘last chance’ to invest, it’s not all over for you just yet. Crucially, you need to have a plan for what you want to achieve, explains property educator and mortgage broker Jane Slack-Smith.

“During my time in the property industry I’ve noticed some pretty clear differences between the people who achieve remarkable success and those who achieve mediocre results, and there are some key differences across the age brackets,” she says.

“By the time they reach their 50s and 60s, traditionally this age group is looking forward to a quieter time of life just around the corner: the kids are off their hands, their income is stable, they are content. However, more and more I see people casting their eyes ahead only a few years and seeing the prospect of retiring on a $35,000 couple’s pension as not an attractive option.”

With an increasing number of people in their 50s becoming first-time investors, Slack-Smith says it’s possible to build a healthy portfolio of two or more investment properties later in life, which can “well and truly set you up in a relatively short time frame”.

“The funny thing is, this age group actually has a real fear of running out of time, and they take on even riskier investment strategies. For instance, I often hear people in this age group wanting to make some fast money by flipping houses or jumping straight into a property development,” she says.

“Speed is their focus, and often they do this without any knowledge and guidance, and they do lose money or at best just break even. I don’t believe people need to have a bad property investing experience to learn from, to then make the right investment. You can shortcut the mistakes others have made by taking some time to plan the way ahead, and building a highperforming, low-risk portfolio.”

Keep in mind that lenders may not look too favourably on handing over funds to a 65-year-old borrower, because they will have the view that retirement is looming and your income is about to dry up.

“Many lenders have started reducing loan terms or even insisting on principal and interest repayments for those over 50, but with life expectancies growing to 80, 90 and beyond, we will HOW TO GET AHEAD AT THIS AGE see people working longer, and lenders will have to accept this new reality,” Slack-Smith says.

“In the meantime, there will be emerging financing sources that will cater to this age group, so keep your eyes peeled. They also have the opportunity to start making their superannuation work harder, and to explore buying property in their self-managed super funds.”

Buying in his 50s: Philippe Brach

Buying in his 50s: Philippe Brach

Some would suggest that at this stage of life it’s not too late to invest in property – and that’s true! It is possible to invest in your 50s and 60s.

However, you have to adopt a different strategy, says property advisor and mortgage broker Philippe Brach – and you must be prepared to take on a lot more risk.

“Luckily for most people, they have some superannuation, so property investing becomes a top-up to their super. You are effectively playing catch-up, so in order to really push your profits you need to have an aggressive attitude to risk,” he says.

“It’s a more dicey proposition, but if you already have a few properties under your belt, then nothing will keep you from continuing to invest. I’m 57 and I just recently added two properties to my portfolio. It can be done!”

With the current lending landscape so conservative, Philippe says this is “also a time when there is a tendency for banks to look at people in their 50s and consider: when are you going to retire?”

“They’re asking: if I give you a 30-year loan, that takes you to 80 – will you still be working and earning an income by then? What the banks want is to see an exit strategy. They want to know how you are going to get rid of the loan, and how you’re going to meet your financial obligations.”

For instance, if you borrow against your home to invest in property, they want to know what your plan is for that loan and investment property. You might explain that your plan is to sell the property in 10 to 12 years to eliminate the loan and use the profits to supplement your income.

“Lenders are forcing you to think about your future plans, which is not a bad thing. They’ve realised they need a more prudent attitude to lending,” Philippe says.

“Whatever your age, it’s a good idea to start with your end plan in mind. Your strategy will change over time, but no matter how old you are, you need to invest as safely as possible: have a plan, and answer the three fundamental questions: How much do you need to get in? How much will it cost to hold? And what is your exit strategy?”

Aged 57, Philippe added

two properties to his

portfolio this year

Related stories:

How to invest in property at any age

Investing in your teens or 20s