Australia's housing markets rebound continued over the last month, led by strong price growth in our two biggest cities, Melbourne and Sydney.

Since bottoming out in June earlier this year, the national dwelling value index has recovered strongly.

Home buyers are back, sellers are putting their properties up for sale, first home buyers are getting a foot on the property ladder and investors are slowly returning.

They are all buoyed by falling interest rates, the prospect of another rate cut early next year, less stringent lending criteria and a generally positive media.

This now marks the fifth consecutive month of price gains in Melbourne and Sydney, which was where the downturn hit the hardest over the last couple of years.

As a result, auction clearance rates are up, asking prices are up, property values are increasing and some property commentators are even forecasting double digit capital growth next year.

However our property markets are very fragmented - not all markets are performing the same.

Same, same for the world economy.

The US – China trade tensions and the uncertainty about Brexit continue to take their toll and these are contributing to a weakness in trade and production.

Economic activity in the United States has decelerated as the year progressed, prompting a third interest rate cut at the October meeting of the Federal Open Market Committee

Recently the International Monetary Fund reduced its global growth forecast for 2019 from 3.2 per cent to 3 per cent, suggesting we’re in a synchronised global economic slowdown. A slowdown – NOT a recession.

Another interesting month for the Australian economy

The latest economic data must be a concern to the RBA with no bounce evident from three recent cuts to official rates and tax cuts.

The jobless rate is rising, employment is falling, and wages growth is declining.

And it seems that economic growth is likely to remain lower for longer keeping the economy away from full employment and the inflation target for even longer than the RBA is forecasting. This means another interest rate cut or 2 is on the cards – perhaps as early as February next year.

The RBA has clearly indicated its preparedness to continue to cut rates and has also flagged the possibility of initiating quantitative easing policies if rates move to 0.25% with no effect on the economy.

Having said that, in the absence of meaningful tax reforms or micro-economic reforms, another rate cut probably won’t help much, but it’s the only response that the RBA can offer.

This should also lead the RBA to questioning the efficacy of quantitative easing, which they’ve been publicly contemplating.

The RBA will be looking for the government to assist with fiscal policy next year possibly bringing their tax cuts forward.

It has become clear over the past year that increased government spending has been vital to keeping our economy afloat. The contribution of government spending and investment to GDP growth is now nearing the levels that occurred during the Global Financial Crisis.

Interest rates remain at historic lows.

In a widely expected decision, the Reserve Bank of Australia decided to keep the official interest rate at its record low of 0.75 per cent last month, after pulling the trigger for the third time this year in October.

The bank has cut rates three times since June, causing house prices to rise in Sydney and Melbourne at the fastest growth rate we've seen in 10 years.

The Reserve Bank keeps reminding us it wants the unemployment rate, which sits at 5.2 per cent, to drop to 4.5 per cent. This is the point where the RBA believes wage pressures should would get inflation moving again.

But this seems an unrealistic target in the short term with more job losses likely in the construction and retail sector

The downside of these consecutive interest rate cuts is that Australian households and businesses are getting nervous. They’re becoming less confident about their job security, their household finances and the outlook for the economy, which is offsetting some of the stimulatory benefits of historically low interest rates.

At the same time many Australians are stashing their cash and paying down debt rather than spending while businesses seem hesitant to invest due to the uncertain global economic outlook.

However there is no doubt the lowest mortgage rates since the 1950’s and improved access to credit following APRA’s decision to loosen lending criteria are contributing to a rebound in housing market conditions.

Just like households, businesses are reluctant to spend. Business investment as a share of GDP is below 12 per cent - its lowest since the early 1990s.

The fastest housing rebound in 16 years

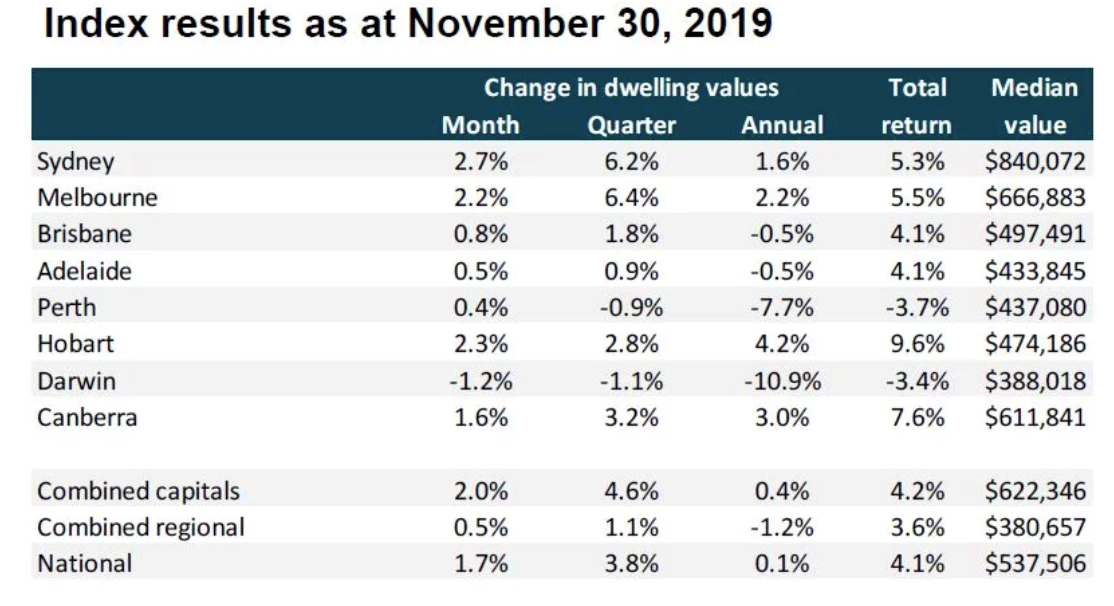

CoreLogic’s national Home Value Index surged 1.7% higher over the month and delivered the fifth consecutive monthly increase, coupled with the largest monthly gain in the national index since 2003, with our two big capital cities, Sydney and Melbourne leading the way.

Source: Corelogic

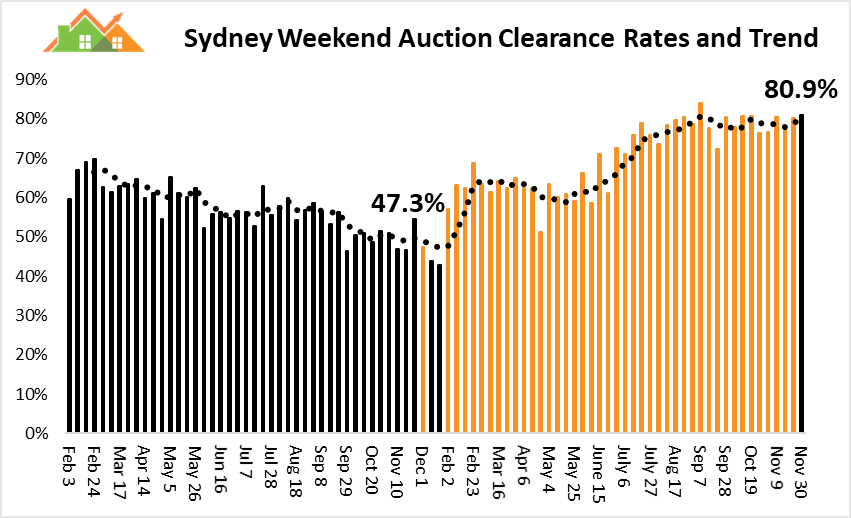

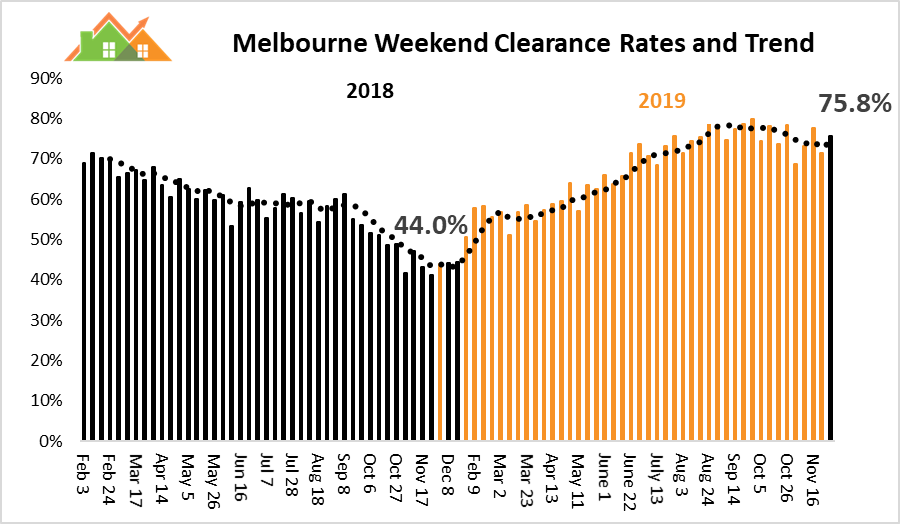

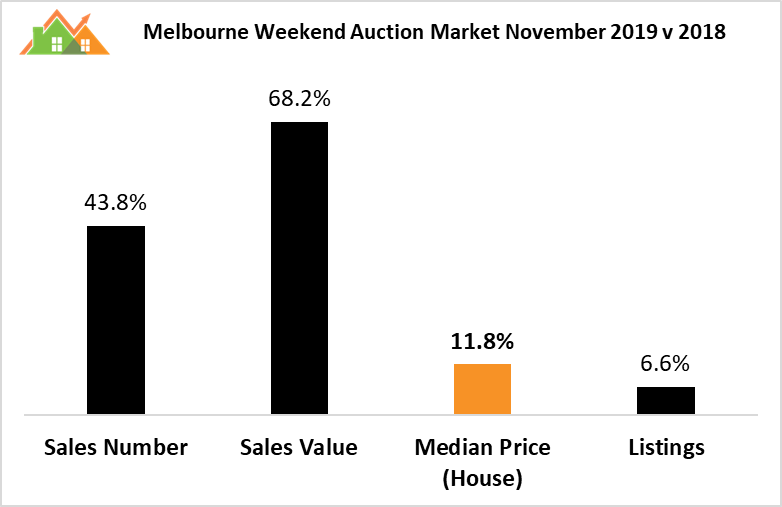

Auction clearance rates point to higher prices ahead.

Auction clearance rates in both Melbourne and Sydney remained firm over the last month continuing the post-election bounce in confidence in our property markets.

The prospect of easier access to finance, falling interest rates and a tax cut has boosted confidence, driving strong auction results across Australia.

It is unlikely that clearance rates will rise any further now especially as more stock comes onto the market for sale in the next few months.

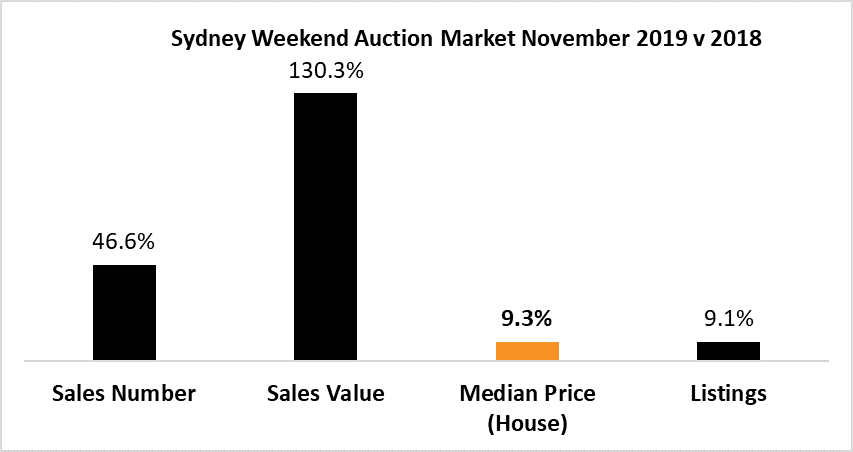

The Sydney auction market is surging reflected by an increasing number of properties offered for sale under the hammer and higher sales values.

The Melbourne auction market has also performed very strongly, particularly in the inner eastern and south eastern suburbs.

What’s ahead for property prices?

Sydney's housing market is on track to recoup the 15 per cent loss in prices suffered during the 18-month downturn early next year and reach a new record high by March.

Melbourne is on track to hit a new record high of prices in January, with property values just 3.7 per cent below their peak reached in October 2017.

Property price growth is likely to slow down once our 2 big capital cities reach new peaks with property values likely to rise more modestly to the end of 2020 growing about 5 to 6 per cent over the year.

It’s a great time to buy countercyclically in Sydney and Melbourne and ride the property next wave of the property cycle in Brisbane.

The downside for these capital city markets is minimal and there is now plenty of upside ahead over the next few years.

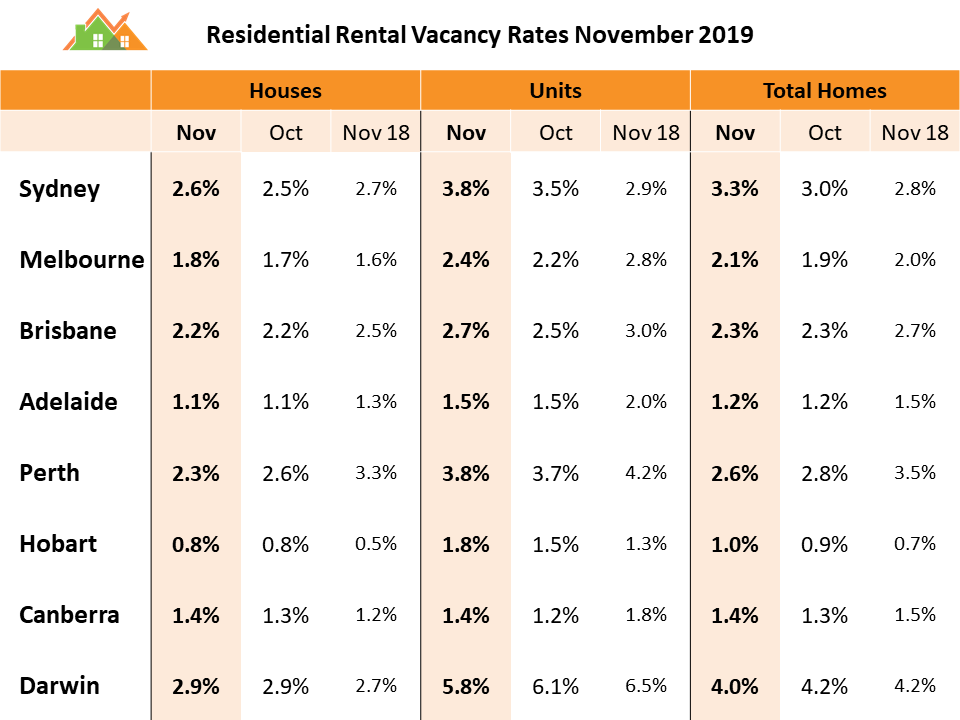

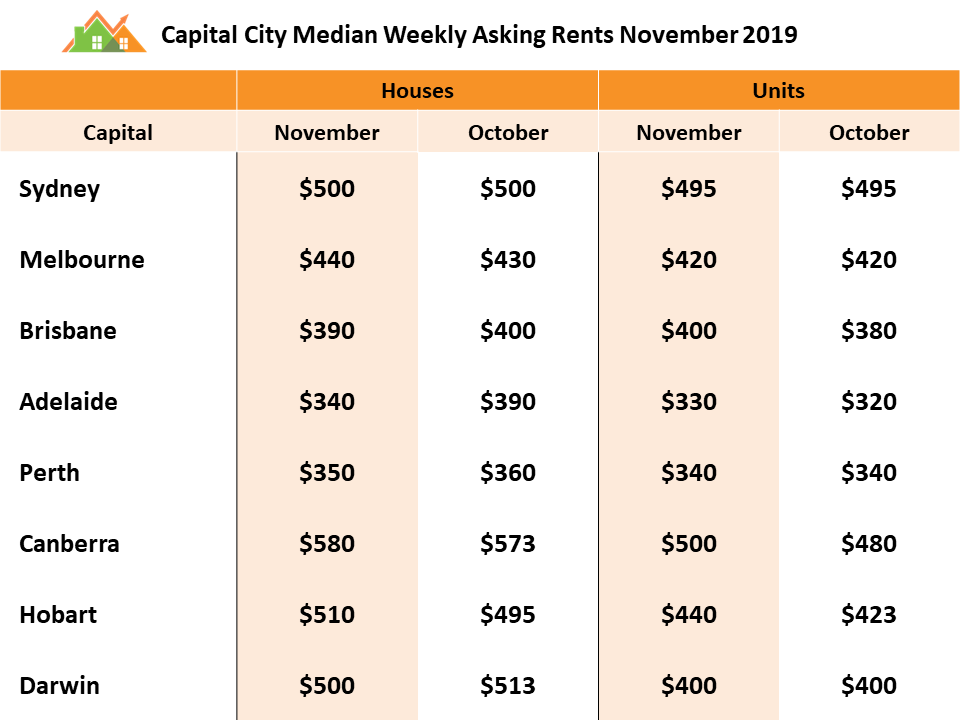

The rental markets

Our rental markets are still relatively flat, and vacancy rates have crept up a little over the last month for Sydney apartments.

The Bottom Line

The Sydney and Melbourne housing markets are leading the Australian market rebound after falling for almost two years.

Home prices are now likely to keep rising for the rest of this year and keep growing steadily in 2020 and 2021.

Sydney's housing market is on track to recoup the 15 per cent loss in prices suffered during the 18-month downturn early next year and reach a new record high by March.

Melbourne is on track to hit a new record high of prices in January, with property values just 3.7 per cent below their peak reached in October 2017.

With thanks to PropertyUpdate.com.au and MyHousingMarket.com.au