We keep hearing that Australia is experiencing “record household debt” and there are regular warnings of impending disaster from the Doom ’n’ Gloom brigade.

These experts chasing a headline love using words like “debt bubble” citing the fact that household debt has been steadily rising in Australia for the past 30 years.

They point out that even after the GFC, when debt was falling in other developed economies, household debt kept rising in Australia.

Australian households now hold debt on average of around 190% of household income – one of the highest levels in the developed world.

So to better understand what’s going let’s do a Q&A with Dr. Andrew Wilson chief economist of MyHousingMarket.com.au

What is household debt?

We can divide our economy up into three parts — households, government and business.

Government and business debt are not especially high at the moment, in fact the government is almost in surplus.

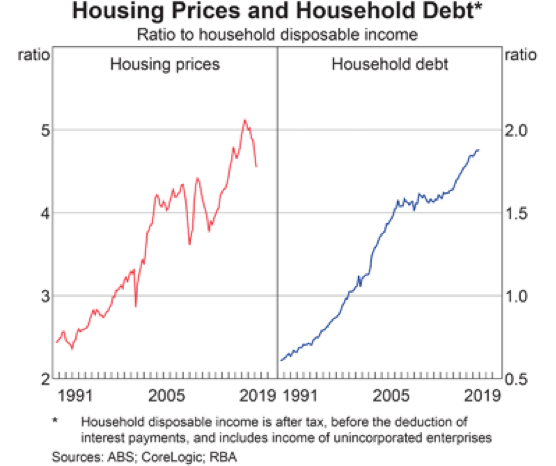

On the other hand, household debt levels have hit record highs as the following chart from the RBA.

Household debt can be defined in several ways but usually includes mortgages, personal loans, credit cards etc

Household debt can also be measured across an economy, to measure how indebted households are relative to various measures of income.

We suggest the best measure of household debt is against affordability, yet many measure it against pre-tax income or relative to the size of the economy (GDP).

Q: Is rising household debt a concern?

Let’s put some perspective to this.

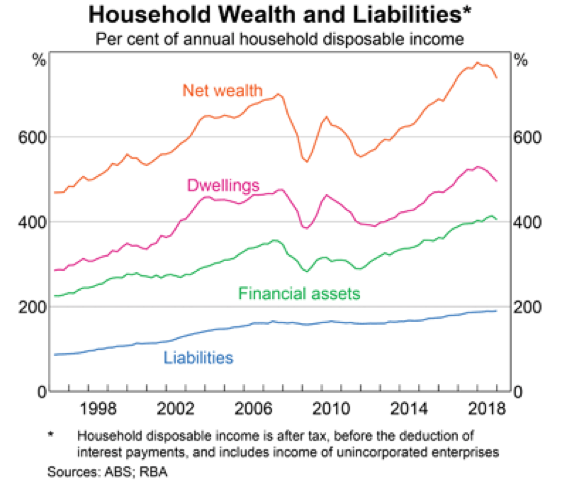

On the other side of the equation are assets - in general real estate – our homes and investment properties.

Owner-occupied mortgages make up around 56% of personal debt with investor debt (much of it against housing) make up another 36%.

As you can see from the RBA graph below, while household liabilities have risen over the last 30 years, so have our assets – in particular the value our homes and our financial assets (mainly superannuation.)

And now that we are at, or near, the bottom of the slump phase of the property cycles the assets that are supporting the bulk of our household debt will keep increasing in value.

Q: As I understand it the concern is that increasing household debt is one of the factors that led to the economic crises overseas – and the worry is that the same could happen in Australia. How risky is it?

Sure household debt has risen as our living standards rose and easy credit encouraged a shift from saving to spending.

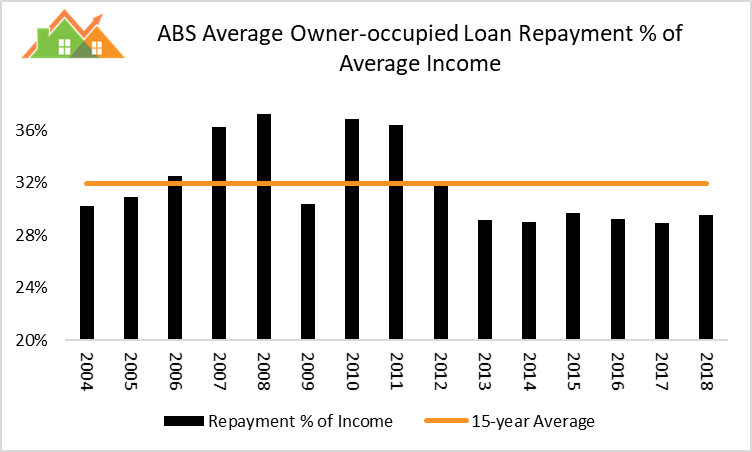

But to assess the level of risk that household debt poses we need to be looking at the levels of serviceability rather than a debt to income ratio.

As you can see from the following graph Australians have been very consistent in the levels of income required to repay their mortgage debt over the last 15 years.

The banks don’t allow us to overborrow and in the last couple of years responsible lending has ensured that only those who can afford to take out a mortgage have taken on new loans.

Source: Dr. Andrew Wilson – MyHousingMarket

The following chart compares home loans in Australia over the last 15 years and suggests that because of lower interest rates serviceability of our home loans has remained much the same.

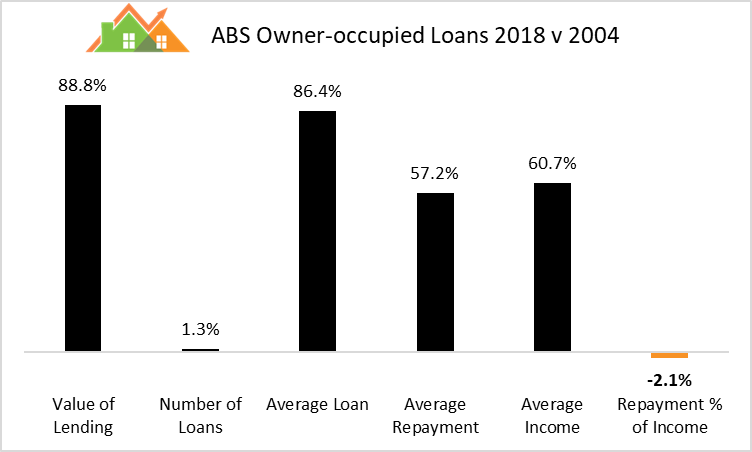

Breaking things down, over the last 15 years:

• The value of lending (in a sense – household debt) has increased 88.8% in the last 15 years

• The number of loans has increased by 1.3% in that time, meaning that…

• The size of the average loan has increased by 86.4%.

• However, the average loan repayment has only increased by 57.2% (because interest rates have fallen over the last 15 years) and at the same time…

• Average incomes have only increased by 60.7% over the last 15 years

Now I can see why some people could be concerned when they see the average debt has increased in the order of 86% while incomes have only increased by 60% in the same time frame.

What they fail to take into account is that because of lower interest rates the relationship between repayments (serviceability) and income has remained much the same (in fact dropped 2.1%.)

And in the same period of time the average property value has increased by 101%.

Q: How many people are susceptible to suffering form an overcommitment to household debt?

Many housing investors has significant mortgages, but many also offset accounts with funds in them.

This means that while the large mortgage shows up in the graph of gross debt, in the real world the borrower has a smaller amount of debt and lower real interest costs because of the funds sitting in their offset account.

Another factor boosting our headline debt figure is that Australia overwhelmingly relies on mum and dad investors (households) to provide rental accommodation.

This is very different to most other advanced countries tend to have more government or corporate landlords.

Thus, the household sector not only carries the debt of owner-occupied housing, but all those negatively and positively geared rental properties owned by investors. In other words their debt is secured by income producing appreciating assets

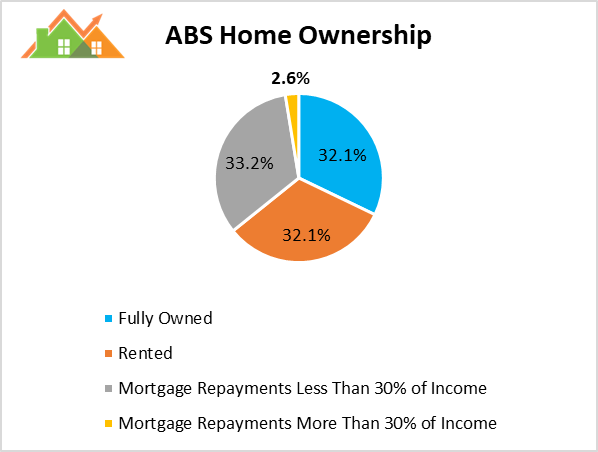

Looking more carefully at the level of home ownership ABS data shows us that:

• About one third of all the homes in Australia are owned without a mortgage.

• Another third of Australian homes have a mortgage against them (sometimes used for purchasing investment properties.)

• About a third of Australians are tenants and

• Only 2.6% of household have mortgage commitments requiring repayments at more than 30% of their household income.

This means that around 2.6% of all households (around 200,000 households) are potentially exposed to potential affordability issues.

However, moving forward affordability is likely to improve as interest rates are likely to fall again, tax cuts are coming our way and wages are slowly rising.

The Bottom Line

The thing that matters most about debt is the ability to service it – the interaction of interest rates and household income. The size of the debt per se doesn’t matter so much.

And this means that the current level of household debt is not of real concern considering we are in a period of prolonged low interest rates and the fact that the assets supporting those debts are generally in good shape.

With thanks to PropertyUpdate.com.au and MyHousingMarket.com.au