Greater Brisbane is in the middle of a rental crisis, the likes of which we have not seen for a long time.

With a record year of internal migration to the Sunshine State, the last year has seen fierce competition for housing.

Many sick of COVID and lockdowns moved to greener, or rather sunnier pastures.

We all know that property prices have skyrocketed but rents have also increased more than 20% during the same period.

With a national property management arm here at Metropole, I am seeing this firsthand on a daily basis.

The media has also reported regularly on the rental crisis and the sad effects of those left without a place to live.

So, what is the state of play and what are we seeing at ground level.

https://www.youtube.com/watch?v=ZpdSDk0LDBA

Sharp Falls in Supply

While there is no doubt, we have seen a sharp rise in demand bought on by interstate migrants, an astonishing lack of supply has really ignited the issue.

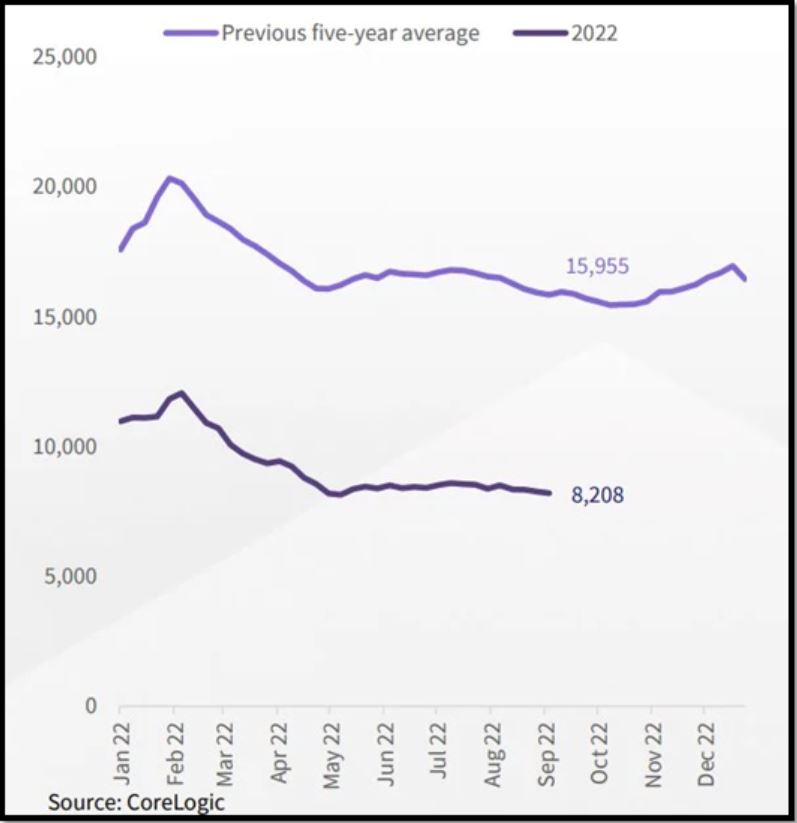

Data released from CoreLogic highlights that rental listings (the number of properties available to rent) are just under 50% lower than the previous 5-year average.

September this year saw 8,208 properties advertised for lease, sharply down when compared to the 5-year average of 15,995 properties.

The rising demand and lack of available stock has been a recipe for disaster for many looking for rental accommodation.

Investors Cash In

While there are a range of factors that had contributed to this shortage, there is no doubt the fact that Investors were selling up to cash in on record house prices was a key issue.

A recent statement from PIPA chair Nicola McDougall suggested 45% of investors in Queensland sold at least one property during the last 2 years.

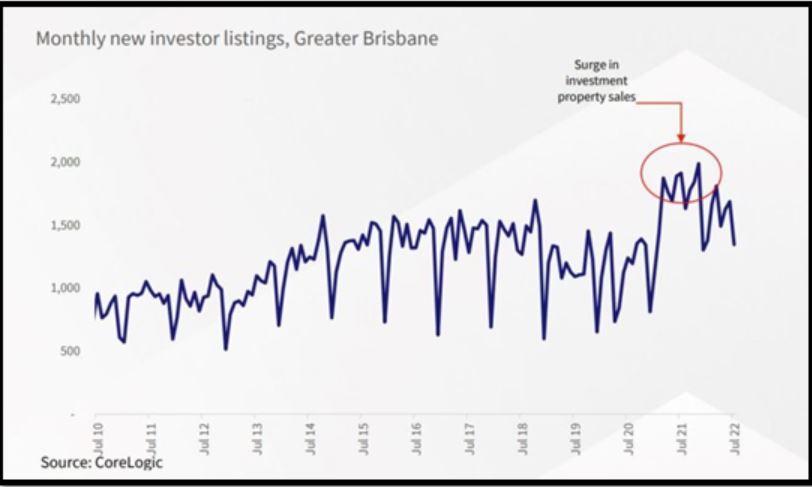

Further data released below by CoreLogic shows the surge in investors selling their investment properties through the July 21 – July 22 period.

This would not be as much of an issue if these properties are sold to other investors and re-entered the rental market.

Unfortunately though, this did not happen and in the majority of cases properties were instead sold to home buyers.

This slashed supply for renal accommodation by potentially 160,000 homes.

Taking a slice out of the market at such a crucial time is far from ideal.

Vacancy Rates

With vacancy rates at uncomfortable highs over the last decade, we are now faced with the opposite.

July saw a record rental vacancy rate of 0.9%, only easing of slightly to just 1% in August.

Again, well below the five-year average for Greater Brisbane of 2.8% coming down from a bigger high.

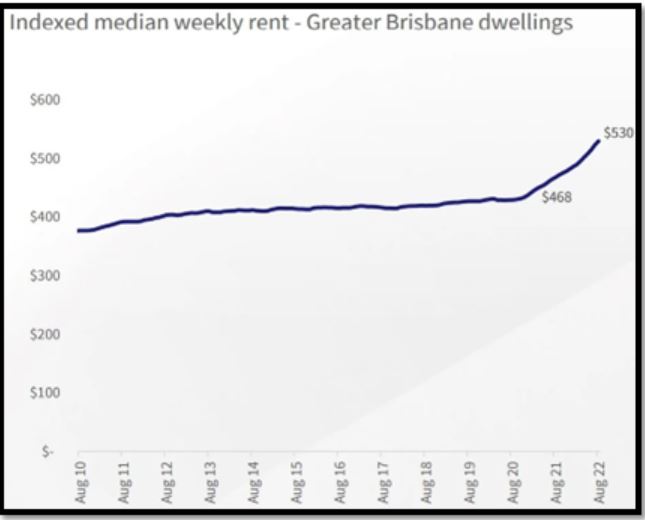

This has seen the median weekly rent climb from $468 to $530, an increase of more than 13% over the past 12 months and another record.

A Glimmer of Hope?

With a proposed Land Tax changes on the horizon, it was fast becoming a tenant’s nightmare and beyond a “common sense” test.

PIPA had revealed that 19% of investors were considering selling up in the next 12 months, with the top reason being the Land Tax changes.

This could have stripped even more housing from the rental pool, resulting in more hardship for potential tenants.

Thankfully that was put to bed recently with news the Land Tax Proposals had been shelved by the Queensland Government.

Source: Australian Financial Review

While far from being a game changer, any positive news is welcomed by desperate tenants.

But any long-term structural solutions to our rental crisis seem to be non-existent.

The issue remains with supply and put simply, no side of Government is proposing anything resembling a circuit breaker.

Investors, often chastised as greedy and selfish, are playing a critical role in filling the void for accommodation.

But there simply must be more productive and proactive conversations being discussed to find a long term solution.