Saying “I told you so” isn’t my style.

So, I’m not about to start saying it now.

But, I am going to revisit a topic I have touched on many, many times in the past.

In my opinion, Off the Plan apartments have never represented a good investment, even during the rosiest of boom times – and least of all during a once-in-100-years global health event.

Apartments in our inner cities, and particularly those in high and medium rise towers, are likely to see their appeal dimmed in the immediate future, with the pandemic revealing that living in close proximity to other potential germ-carriers can be risky, and that being cooped up in a tiny flat during a lockdown is no fun.

But in particular, those investors who’ve bought an apartment off-the-plan are about to realise that I wasn’t joking around when I repeatedly warned that it was a bad idea.

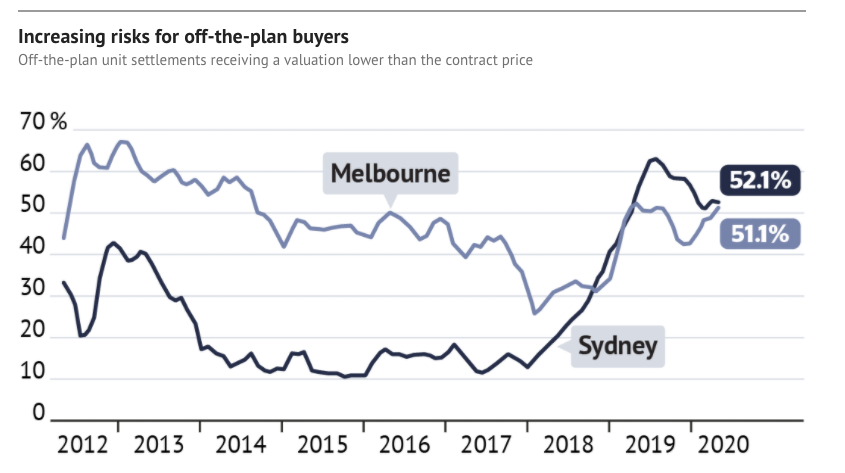

As you can see from the chart below, around half the off the plan properties currently being completed value in at less than the original contract price, with many showing current values being more than 10% below the original contract price.

Source: CoreLogic

Here’s where the big problems are going to arise

For some buyers who have lost their job or had their hours cut as a result of the pandemic, meeting the original settlement dates will become a huge challenge.

If they’re lucky, they might be able to negotiate an extension with the developer – but what happens if their financial circumstances don’t improve?

We are heading into a recession after all, and that comes with no guarantees.

The other thing to remember is that your lender will value the property upon completion, and in the current market, there’s a good chance this valuation will come in at a price that is considerably lower than the contract price.

This is always a risk of buying off the plan but in the current market, this risk is heightened.

Banks are being more conservative than ever with their valuations.

As a result, buyers who have committed to an off the plan property could see their loan applications knocked back, or they may be forced to scramble for a larger deposit to cover the shortfall.

For instance, let’s say the apartment you committed to for $500,000 might only value up at $450,000 – and the bank might be willing to lend you a maximum of 80 percent of that value.

So, you’ll have access to $360,000 but you need to hand over $140,000 – which is a sum of money that many just won’t be able to find.

I don’t want to be too “doom and gloom” about this…

But given the state of our economy right now, I can see a lot of borrowers finding themselves trapped in this predicament right now.

Purchasers may have stumped up a 10 percent deposit, only to find the property is valued at less that 90 percent of the original price once completed.

They stand to lose their deposit and walk away much worse off than they were before they signed that dreaded off-the-plan contract.

In fact, it's possible the developer will sue them for any shortfall they experience when on selling this property.

According to BIS Oxford Economics, two thirds of new Melbourne apartments (many of which were bought off the plan) either made no price gains or lost value over the last decade, in spite of the fact we’ve had record levels of immigration during that time.

Of course the large part of this was because the initial purchase price of these apartments was inflated to cover developers margin, marketing costs advertising etc.

Now this is very different to established low rise apartments - the types that used to be called flats - which have tended to perform much better.

While these and other types property types experienced significant jumps in price throughout the property boom, the new apartments remained relatively stagnant, and it’s been a similar story in Brisbane and Sydney.

And let’s keep in mind that the stats I’ve just quoted are from business-as-usual, non-COVID times.

As we stumble towards our first recession in 30 years, with the ever-present fear of a resurgence of the virus, even the most optimistic among us will have to admit that it’s not looking good for these properties.

Another key factor I’ve written about is the fact that apartments in medium and high density towers don’t have as much owner occupier appeal.

To maximise your resale value, your property needs to appeal to a broad range of potential buyers.

Why does this matter?

Well, owner occupiers don’t make their purchase decisions based solely on logic.

They often buy with their heart, so if you can make them fall head over heels with your property, they might overlook the flaws and pay top dollar, regardless of the market – love can make us do crazy things.

And why don’t these new apartments appeal to owner occupiers?

There are lifestyle factors of course – no garden, shared amenities, noise – along with the fact that many apartment buildings are hastily and poorly constructed from a cookie-cutter design, which doesn’t make them attractive as “forever homes”.

Just to make things clear…

Many homebuyers have changed their preferences and are trading backyards for balconies.

While they're prepared to live in apartments many prefer the more solidly built low rise established apartments in the inner suburbs rather than the new towers in and around our CBDs.

Since, owner occupiers won’t want to buy up these apartments, and at the rate the economy is going, investors will be steering clear of them too, knowing that there’s no guarantee they’ll see a rental return that fits into their strategy, unfortunately, the sad fact is that some investors who bought will be financially ruined by the combination of buying a property that was never a great investment, only to have this compounded by a global pandemic and recession just to dig the boot in a little more.

Those who manage to hang onto their properties will be the new owners of dwellings that are likely to become the slums of the future, in a market where rents are plummeting – rather than investing in growth assets that will build their wealth.

And those who are forced to walk away from their contracts?

Well, they could see their life savings squandered – right at the time when they need that safety net the most.

If you’re committed to an off the plan property and you need a strategy to help you take action and set yourself for the opportunities that will present themselves as the market moves on – rather than being stuck with a dud investment that moves you backwards – know that you’re not alone.

..........................................................

Michael Yardney is CEO of Metropole Property Strategists, which creates wealth for its clients through independent, unbiased property advice and advocacy. He is a best-selling author, one of Australia’s leading experts in wealth creation through property and writes the Property Update blog.

Michael Yardney is CEO of Metropole Property Strategists, which creates wealth for its clients through independent, unbiased property advice and advocacy. He is a best-selling author, one of Australia’s leading experts in wealth creation through property and writes the Property Update blog.

To read more articles by Michael Yardney, click here