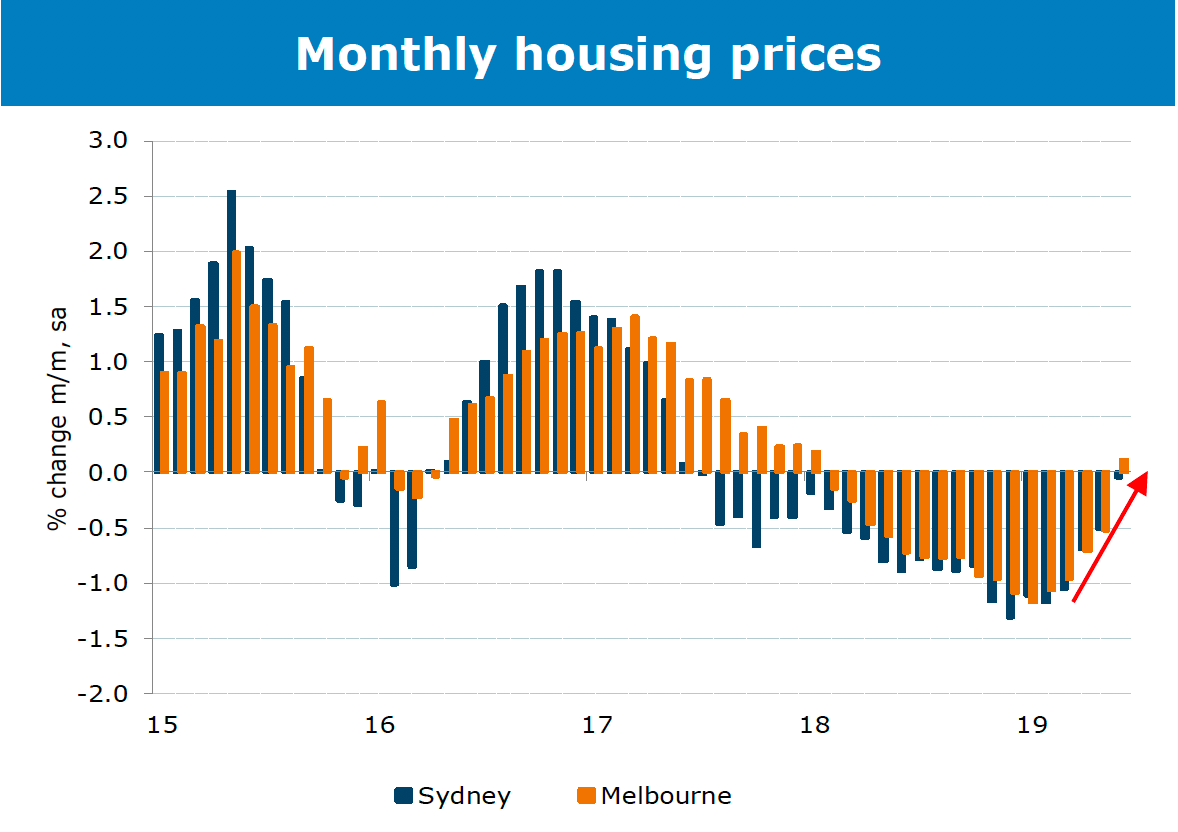

It looks like we’re moving into the next phase of the property cycle with increased buyer confidence, rising auction clearance rates, interest rates falling, and home prices stabilising in Sydney and Melbourne.

This graph of seasonally adjusted monthly house price moves, based on CoreLogic data, tells the story.

So it’s interesting to look back and see which properties were hit the hardest in the downturn and see what lessons we can extract.

Source: ANZ Bank

Two of the market segments that suffered were:

1. Top End properties

While overall property values fell between 11 and 14 per cent in the Melbourne and Sydney property markets, as has happened in previous downturns, the top end of the market suffered the most.

Of course properties in these suburbs rose substantially during the previous boom, but these markets are volatile and tend to overshoot during booms and slump worse during property busts.

It could now be a couple of years before owners in our top end suburbs see a recovery in home prices.

The lesson for investors is that the top end of town is never the right pace to invest – property values there have always been more volatile, rising strongly during times of economic prosperity and falling when the economy slows or the stock market slumps.

These suburbs are subject to discretionary spending. After all you don’t need that new $7 million mansion when your humble $4million home is still in good shape.

2. Mining Capitals

But it was the former mining capitals of Perth and Darwin that were hit the hardest, with respective falls of 20 and 30 per cent compared to a national decline of just over 8 per cent.

The big difference here is that Melbourne and Sydney’s property downturn was driven by tighter credit, particularly for investors and our government pulling out the welcome mat from overseas buyers, rather than rising unemployment and weak economic growth that was seen in Perth and Darwin.

The lesson for investors here is that while property markets always move in cycles, it’s best to invest in locations where the local economy is supported by multiple pillars of industry rather than relying on one sector for jobs and economic growth.

What’s next?

Most property economists believe house prices are now stabilising and expect a modest recovery over the next 2 years.

I know some commentators are suggesting house prices are about to surge, but I don’t think that’s the case.

I see more moderate price growth – around 3-4% overall growth in 2020.

Sure interest rates have dropped and APRA’s easing on lending criteria will make getting a loan easier, but other measures of assessing loan serviceability will continue to impact the availability of credit and there is still uncertainty about jobs growth and employment security.

Here is what ANZ Bank forecasts will happen to property values next year.

(1).jpg)

..........................................................

Michael Yardney is CEO of Metropole Property Strategists, which creates wealth for its clients through independent, unbiased property advice and advocacy. He is a best-selling author, one of Australia’s leading experts in wealth creation through property and writes the Property Update blog.

Michael Yardney is CEO of Metropole Property Strategists, which creates wealth for its clients through independent, unbiased property advice and advocacy. He is a best-selling author, one of Australia’s leading experts in wealth creation through property and writes the Property Update blog.

To read more articles by Michael Yardney, click here

Disclaimer: while due care is taken, the viewpoints expressed by contributors do not necessarily reflect the opinions of Your Investment Property.