Expert Advice with Simon Pressley

There are a variety of different metrics which provide insight into future property market performance; rental market conditions are one such metric.

While a number of factors need to be considered to provide a clearer overall picture, Propertyology believes that current rental trends are showing signs of changing property market cycles in several Australian locations.

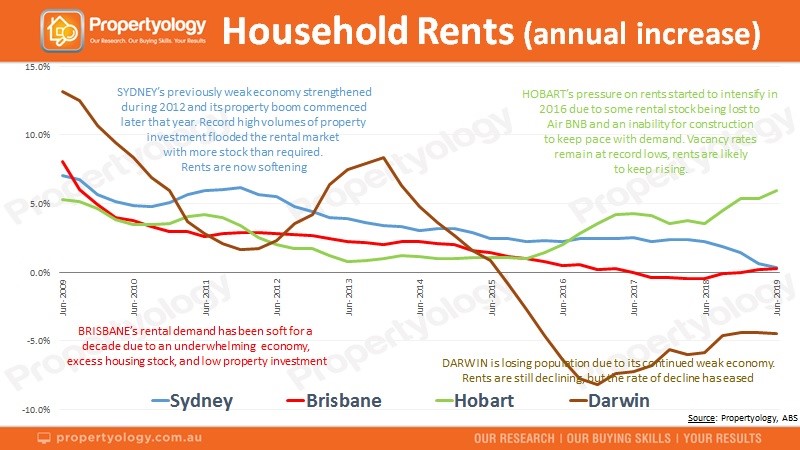

SYDNEY’s strong rental demand has been driven by overseas migration, an economy which has been healthy for the last 6 years, and the high cost of home ownership. For several years, Sydney’s rate of rental price growth has consistently eased due to record high housing construction combined with a high volume of extra investment properties being added to the rental pool during Sydney’s property boom.

Sydney vacancy rates are now at an all-time record high and rents are declining. With a sizeable pool of new properties, predominantly apartments, still in Sydney’s construction pipeline and consistently more Sydneysiders choosing to migrate to other parts of Australia, Propertyology forecasts that Sydney’s rental market will remain soft for some time yet.

HOBART’s rental demand increased significantly over the last four years. This has been driven by the biggest economic recovery produced by any state during this century, solid job creation, and internal migration. Adding to Hobart’s rental pressure was the popularity of Air BNB and the subsequent transference of stock from the long-term tenancy pool into the leisure and corporate letting pool.

Hobart’s construction sector has been unable to keep pace with the extra demand driven by its economic growth. Vacancy rates are still at record lows and has already resulted in rent increases for a standard house of circa $100 per week over the last 2 years. Propertyology anticipates that rising rents and reduced interest rates will trigger an increase in first home buyer activity, thereby further extending the growth cycle within Hobart’s property market.

Hobart still has the best overall fundamentals of all capital city property markets.

BRISBANE’s rental demand has been soft for a decade. An underwhelming economy, excess housing stock and low volumes of investment in residential real estate doesn’t produce rental pressure. More recently, Brisbane’s reduction in residential construction combined with an increase in internal migration (a biproduct of housing affordability pressures in Sydney and Melbourne) has returned Brisbane’s rental market back to equilibrium status.

Brisbane’s property supply levels are now supportive of a long-overdue property growth cycle however, significant price growth will not occur without meaningful (private sector) job creation first being produced. Meanwhile, Propertyology’s buyer’s agents are enjoying helping property investors to take advantage of opportunities in other parts of Australia that offer the leading indicators of job creation that Brisbane still lacks.

DARWIN’s 10 out of 11 years (ending 2012) of double-digit property price growth is now a distant memory. The Top End’s continued weak economy has culminated in a net annual population loss and Australia’s highest residential real estate vacancy rates. Rents are still declining, although the rate of decline has eased.

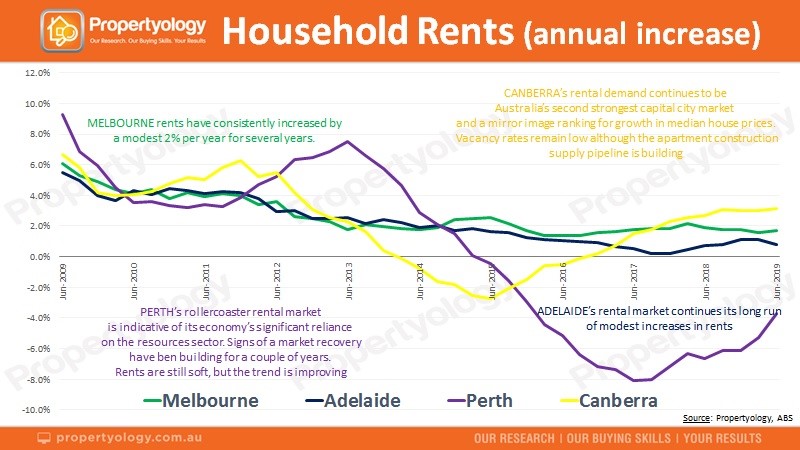

MELBOURNE’s rental market has been mostly balanced for the last 4-5 years and vacancy rates are currently steady at circa 2 per cent. While Melbourne’s economy is still strong, the construction industry became over-stimulated during Melbourne’s last boom. The housing over-supply and affordability pressures which caused Melbourne (and Sydney’s) property market downturn still holds some relevance today.

Beware the wishful thinkers who are hoping for a sustained bounce to Melbourne’s property market!

ADELAIDE’s uninspiring economy and weak population growth has meant little increase in rental demand throughout the last decade. New housing supply volumes have been low. The city’s vacancy rate has stabilised at a low 1 per cent, thereby adding some pressure on rents. Adelaide’s current property market fundamentals are a carbon-copy of Brisbane’s – job growth is the missing link required to trigger a growth cycle.

CANBERRA’s rental market has been Australia’s second strongest capital city over the last 2 years. Growth in median house prices is also ranked second, behind only Hobart. Canberra’s economy has benefitted from a strong tourism sector and an increase in professional services jobs and international students.

While rental demand looks likely to remain strong in Canberra, new supply (especially apartment stock) may produce a reduction in rental pressure.

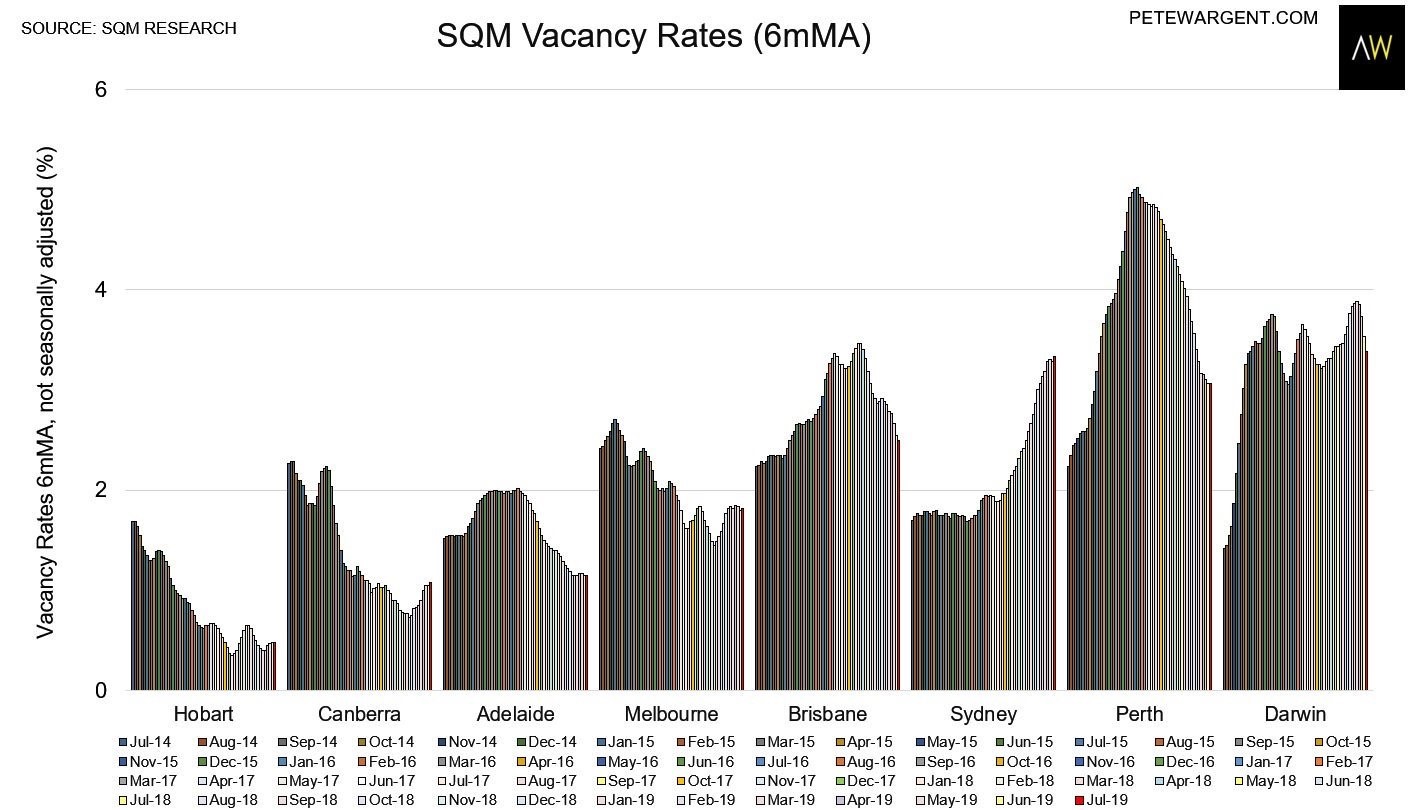

PERTH’s 10-year trend line in the above chart highlights the peaks and troughs of Australia’s fourth largest city. Significant population losses to interstate migration produced a reduction in rental demand and falling rents during each of the last 4 years.

While Perth’s residential real estate vacancy rates are still relatively high, they have declined significantly over the last 2 years. A resources-driven economic recovery is already underway, creating optimism that the start of Perth’s next property market growth cycle is on the horizon.

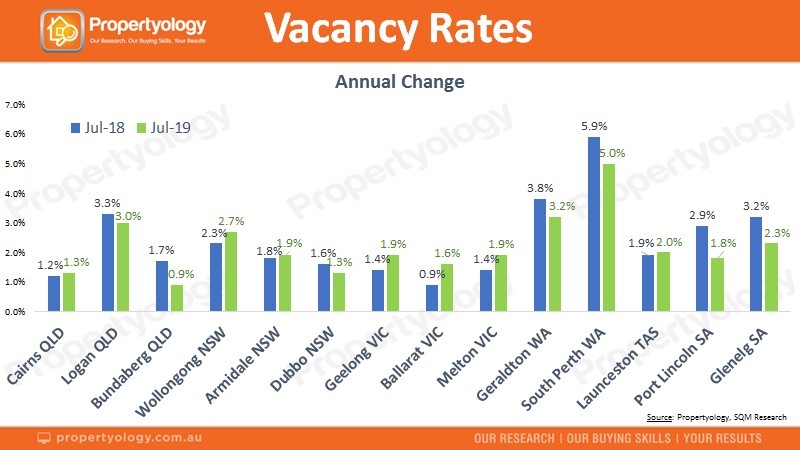

As for rental markets in Australia’s non-capital locations, the ABS do not publish quarterly rental data for us budding analysts to devour. There is nonetheless, a number of factors which we can monitor to measure rental market pressure in the many wonders of regional Australia.

The above chart is by no means a comprehensive analysis of all of regional Australia. What it does provide is examples from most states to illustrate that property markets are either already incredibly tight or the trend is heading in the right direction.

Cairns, Mackay and Bundaberg are just two examples of regional Queensland real estate markets with much lower vacancy rates than most capital cities, while rents in Moranbah are now skyrocketing.

Vacancy rates in Logan (Brisbane outer-south) is on the high side and rents have softened a touch as a result.

In New South Wales, Wollongong’s rental market, like Newcastle and Port Macquarie, is softening while Dubbo and much of the Central West has been tight for quite some time. Rental pressure is likely to further intensify in Armidale, Wagga Wagga, Griffith and others.

Geelong and Ballarat have been strong regional Victorian property markets for a few years however, recent relaxation within their rental market is just one example that suggests that their respective growth cycles have peaked.

Launceston has been one of Australia’s strongest property market over the last 12 months, however pressure is also tight in Burnie and Devonport from both a rental market and property price perspective.

Tasmanian real estate generally still offers the biggest bang for any property investor’s buck!

......................................................................

Simon Pressley is Head of Property Market Research and Managing Director at Propertyology.

Simon Pressley is Head of Property Market Research and Managing Director at Propertyology.

Propertyology is a national property market researcher and buyer’s agency, helping everyday people to invest in strategically-chosen locations all over Australia. The multi-award-winning firm’s success includes being a finalist in the 2017 Telstra Business Awards and 2018 winner of Buyer’s Agency of the Year in REIQ Awards For Excellence.

Disclaimer: while due care is taken, the viewpoints expressed by contributors do not necessarily reflect the opinions of Your Investment Property.