13/11/2013

Question: My son is keen to start investing in property, but he’s only 18 years old. Is there a minimum age the bank will lend to? He’s earning around $40k and saved up $10k over the years. What is his option if he can’t get a loan from the bank?

Answer: Great idea: the earlier he starts the better. Age 18 is the minimum for loans; banks don’t lend to minors.

Assuming he has no other debts (not even a credit card) and will earn $200 per week in rent; and he is paying $150 to you in board and current loan interest rates are around 5.5% pa, your son can get a loan of between $165,000 and $220,000, depending on the lender. The bigger issue is the deposit. It’s a fantastic effort saving up $10,000; however, it may not be quite enough.

Remember that as an investor your son is unable to access

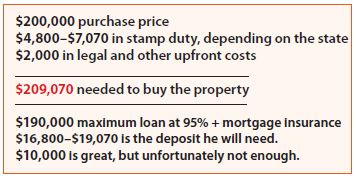

the First Home Owner Grant. He would need, at a minimum, 5% of the purchase price plus any stamp duty and costs.

Let’s look at the example below:

There are some options:

- He continues saving until he has enough.

- You or another relative/person gives him the extra $9,070 he needs as a gift.

- You or another direct relation provides a ‘family guarantee’, which means you put up your property as collateral for the loan and he will not need as much deposit. A family guarantee allows the bank to use some of the equity in your property to help out as extra ‘security’ for their loan.

It works because the bank will take a mortgage over your kid’s property and also over your property, meaning they will have more security for the loan. Banks like it when they have more security. This helps in two ways: it lets your kid buy faster, rather than waiting for years to save more, and it also removes the need for them to pay mortgage insurance. Remember that mortgage insurance is payable when the loan is more than 80% of purchase price. Mortgage insurance rates vary, and can easily be $10,000, $15,000, or even $20,000 in some cases.

These guarantees are not like the old-style guarantees where mum and dad put their whole house on the line. These days the guarantee is limited to an amount, eg 20% of the price/value of the property, and the loan remains in the kid’s name, not yours.

Rental income serviceability

When the bank calculates your serviceability, what proportion of the rental income will they use? Do banks differ in the amount they take into consideration? Which bank takes all or the highest? Generally, 80% of the rental income is used, although some banks only use 70% if it’s a high-rise. The policies are different at each bank.

AMP has a unique policy of accepting 100% of the rental income, provided the loan-to-value ratio is under 80%, but if it’s over 80% or if the total loans to AMP is more than $1,250,000, then it’s 80% of the rental income.

That said, the amount of rental income used for servicing is not the only factor a lender will look at when working out your serviceability. In fact, interest rate policies, depreciation, your income and credit card limits have a far bigger impact on the amount you can borrow.