Are you a sucker for a juicy, click bait headline like me?

Maybe like the one I have just used…

A promise of endless cash flow would have to be the most fake headline in property investment advertising

It is the bait that lures you in, in the hope that you are snapped up by the salesperson.

After all, who doesn’t want more cash flow in their lives?

But as I will explain shortly, positive cash flow is only an outcome and not a strategic way of investing.

It is a very superficial way of looking at investing and only takes into consideration one of a multitude of factors.

I would also argue, whilst important, for mine, cashflow should initially be a secondary consideration.

There is always an argument around capital growth vs cashflow in property circles, but in my opinion, it is really a non-argument.

Let me explain.

The Theory

The theory is simple to understand.

Invest in assets that once you’ve covered the loan payments and ongoing expenses using the rent you have received, you have money left over.

Do it often enough and you may even be able to replace your income….. supposedly.

Having a property producing additional funds each year, is certainly an appealing prospect.

But you must ask yourself would and additional $5,000 or $10,000 each year really change your life?

You may even find that promised profit doesn’t eventuate, especially after removing tax adding an interest rate rise or two.

You are left with a property that is neutral or slightly positive that it is likely not growing in value at all.

This scenario leads to one of the most common quotes we hear as Property Strategists…..

“It has not grown in value, but at least it is not costing me anything.”

The big problem is they have made cash flow a primary focus and comprised on capital growth.

A similar outcome of neutral or positive cash flow could have been achieved with a higher growth asset, despite the lower rent initially.

You could achieve this outcome;

- Putting down a larger deposit

- Paying Interest Only initially

- Adding value through a simple cosmetic upgrade or two

- A combination of all of these.

Residential Property

As an investor you must understand that residential property in Australia is primarily a high growth, lowish yielding asset.

In most cases, it is also considered to be a relatively low risk investment.

With so many entry and exit costs, it is also much more beneficial as a long-term investment.

Many investors and salespeople attempt to change these principles to achieve a desired outcome.

They do this by promoting;

- Buying Off the Plan with rental guarantees

- Looking for Dual Income Properties

- Secondary locations with no growth but good rental income

- Adding a Granny Flat

These types of investments add further risk and it changes the investment profile for residential property altogether.

That is largely why, 92% of investors never get past their first or second property.

While it may not be costing these investors physically, the opportunity cost may be huge.

A Case Study

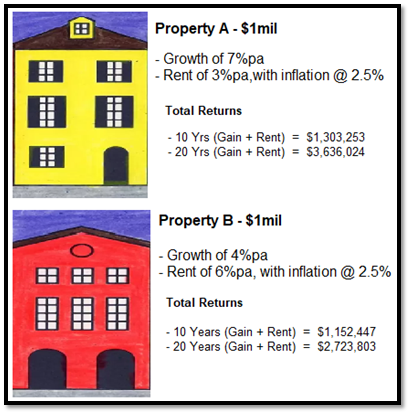

Lest us this example of two different investors and the purchase of a $1million property.

Investor A understands the principles of residential property and looks to buy an asset that will appreciate along the line of longer-term averages.

The property will grow and compound by 7% per annum and they will receive a rental return of 3% per annum.

Rents then escalate along the lines of long-term inflation being 2.5% per annum.

Investor B decides to compromise these principles and invests for cash flow.

They are chasing an outcome and require a property with a 6% yield and will receive a lower capital growth rate of 4% per annum.

These properties are much risker assets and as a result will attract a greater yield to compensate for that risk.

Demand for these properties also drop and growth declines, as they rule out most home buyers and savvy investors.

While a few percentage points in either direction may seem insufficient at the time, the results can be quite extraordinary over the longer term.

Over a decade Investor A would be $150,806 ahead, while after another decade of compounding, 20 years later they would be in front $912,222.

The Result

While the analytical minded may have some thought around some of the minor detail, the big picture is clear.

In 20 years’ time, Investor A ends up close to $1million dollars ahead by making capital growth their primary objective.

Now that would be life changing!

Not only has it put them in a better position later in life, but initially it would have also allowed them to purchase again much sooner, to build even greater wealth.

This is the opportunity cost that many investors do not understand.

I always tell my clients that are looking to build an investment portfolio that the right property for them is the one that gets them into their next property the fastest.

The simple message is NEVER compromise on the capital growth of your investment.

Summary

Whilst you are considering investing in property, don’t get sucked in my superficial headlines.

Take a much more strategic approach.

Rather than focusing on the outcome, follow a framework that enhances the benefits of residential property.

Use growth as the primary focus and then use the framework and modelling to produce the outcome you want.

If it is more cash flow you require, then change some of the inputs, such as a larger deposit, paying interest only or a quick cosmetic update.

A bit of extra cash flow here and there may be beneficial in the short term, but hundreds of thousands, perhaps millions of dollars more will be life changing

Our team at Metropole never advise our clients based on a gut feel, they follow a proven framework and use the data and numbers to guide their decision-making process.

It’ll start by creating a Strategic Property Plan to help them plan to become the person they plan to become.

And then explain to them not to expect their plan go to plan so we have a number of checks and measures in place, including regularly reviewing the performance of their property portfolio.

.....................................................

Brett Warren is a director of Metropole Properties in Brisbane and uses his 18 plus years property investment experience and economics education to advise clients how to build their portfolios.

Brett Warren is a director of Metropole Properties in Brisbane and uses his 18 plus years property investment experience and economics education to advise clients how to build their portfolios.

He is a regular commentator for Michael Yardney's Property Update.

Disclaimer: while due care is taken, the viewpoints expressed by contributors do not necessarily reflect the opinions of Your Investment Property.