The 2019 Perceptions of Housing Affordability report goes beyond the numbers. It delves deeply into what Australians are thinking and feeling about property, exploring their hopes and dreams.

What we know is that affordability has deteriorated in recent times. But the drive and passion to own that piece of Australia remains. The Australian dream hasn’t been tarnished. We found that over 81% of Australians – four out of five – believe it is still important to own a home.

However, we can’t be complacent. The Australia housing market remains unaffordable, and we could be entering a new period of price rises. With interest rates at record lows, prices are starting to recover, but we still face a critical situation. Let’s look at some statistics.

- The household income-todwelling value ratio today is 6.5 times. So the typical Australian household is spending, on average, 6.5 times their gross annual income to buy a median-priced dwelling for $524,000. Less than 20 years ago, it was 4.5 times.

- The market is hard to get into. It takes an average of 8.7 years to save for a 20% deposit. That’s a long time – one eighth to one tenth of a life.

- Once you overcome that steep hurdle and get your foot in the door, you spend 35% of your gross annual income on servicing your mortgage. That is a serious amount of disposable income you need to be able to service your loan.

Meanwhile, wages growth remains insipid. Australians just haven’t been getting the pay rises required to help them save and pay for more expensive housing.

It’s not surprising, therefore, that while half of Australians think affordability has improved in the last two years, more than 80% are still concerned about being able to afford their first or next home.

The ‘cubby house’ syndrome, in which young people decide to stay at home with mum and dad, is alive and well. Some 63% of Australians who are still living with their parents say they can’t afford to move out of home, up from 62% in 2017.

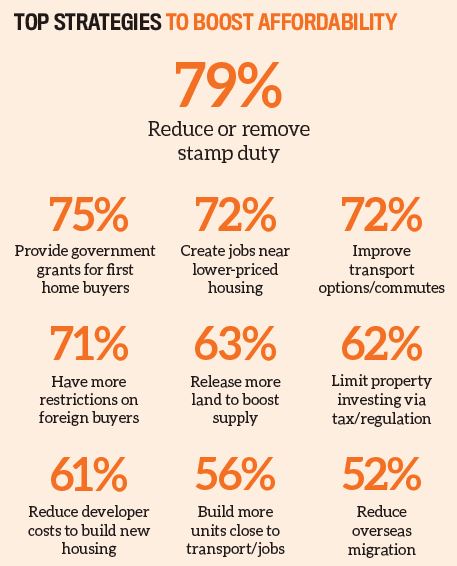

Unfortunately, to date we have applied some cosmetic levers – such as stamp duty concessions and first home buyer grants – to alleviate the affordability challenge. They do provide temporary relief, but we need to address more fundamental levers. We can’t rely on falling house prices to solve the affordability crisis.

As a priority, we need to transition from a stamp duty-based property tax scheme to a broad-based land tax. We accept that all governments need to raise taxes through property, but stamp duty is ineffcient. It very much falls at the point of purchase, so new customers carry the burden.

A broad-based land tax is a more democratic way of sharing the burden. I’m glad to see the ACT has embarked on a 20-year journey of moving in this direction. It would be fantastic to see other states and territories emulate it.

Lisa Claes

is the CEO of CoreLogic International,

the world’s largest property data and analytics company