I've been investing in property for nearly two decades, and one of my favourite sayings is “50% of something is better than 100% of nothing”, especially when it comes to joint ventures.

A joint venture (JV) is a business arrangement between two or more parties. The parties combine their resources for the purposes of buying a property. Generally speaking, JVs are usually between two parties, as this keeps things simple; however, you can have more parties depending on the size of the property purchase or its purpose.

What are the benefits of a joint venture?

There are many benefi ts to a JV. For example, it allows you to spread your risk by owning a percentage of a property rather than 100% of it, so if something were to happen you would have your JV ‘business partner’ to support things in the short term.

There are many benefi ts to a JV. For example, it allows you to spread your risk by owning a percentage of a property rather than 100% of it, so if something were to happen you would have your JV ‘business partner’ to support things in the short term.

If you are new to the property market and struggling to save for a full deposit, far less the additional settlement costs like stamp duty, etc., a JV business partner could help by contributing to the deposit. This would mean you could get into the market sooner and enjoy a property's capital growth, rather than taking the time to try to save for a full deposit.

By combining your income with your JV business partner’s in order to borrow from a lender, you might also be able to purchase a better property, closer to amenities, and that sees more demand from tenants and/or gives you greater cash flow or capital growth.

Going it alone could see you priced out of the market or start out with an inferior property. However, like all good things in life, there are risks associated with JVs, especially if you fail to dot your i’s and cross your t’s.

What are the risks of a joint venture?

The biggest mistake investors make with JVs is not paying attention to the fine print. That means many fail to have a legal agreement in place to protect all parties involved. I like to advise investors to get a JV agreement in place once they have decided they want to do a JV. It’s as simple as writing down the roles and responsibilities of each party so everyone is clear on who will do what and when.

Then it is also important to include a time frame, eg how long will the JV be in place before you sell the property or before either party can be bought out? What will you do if ‘life gets in the way’ and one party can no longer honour the agreement?

You also need to consider your exit strategy and buffers, and what you will do if the market falls or you can’t find a tenant.

When taking on a JV business partner, make sure you are clear upfront on what your exit strategy will be. You need to know if your JV business partner will be happy to hold on to the property for a number of years or whether they will want out of the deal in 12 months’ time.

It’s best to work out these issues in the cool light of day, while everyone is optimistic about the partnership, and to put contingencies in place. Not documenting the above increases your chances of disagreements and misunderstandings as it will be difficult to remember who said what and when. Your next move is to obtain professional advice from a solicitor, who can guide you on the best JV agreement for your situation.

What types of joint ventures can you use?

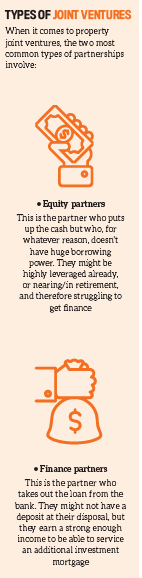

When it comes to a joint venture, you are only limited by your imagination. You can set up a JV in which one party provides the equity/deposit (20% plus costs), and the other party borrows the 80%. You could also split the deal 50/50 down the middle, whereby each party has half the deposit and also jointly borrows the money from the lender.

JVs work best when two parties can come together to leverage each other’s strengths and minimise each other’s weaknesses. For instance, you might enter into an arrangement with a friend or family member in which each partner contributes towards the deposit and/or the costs of managing the property investment. This enables you to not only split the costs in whatever manner suits both parties, but also share the risks.

When it came to our own JVs, we used an equity partner. This is how we purchased two of our properties. We found an equity partner who wanted to invest but lacked the borrowing capacity, whereas we had borrowing capacity but lacked equity. They put in the deposit plus costs and we borrowed the balance from the bank. It was a perfect arrangement – so much so that we did it again.

Our third JV was split 50/50: both parties put in 50% of the deposit plus costs and both parties jointly borrowed the money.

Example of a joint venture partnership

I understand that some investors would prefer to purchase a smaller-sized investment property just so they can get into the market. However, if purchasing the property limits your capacity to build your wealth, then you may be better off finding a JV partner and purchasing a larger property together.

I understand that some investors would prefer to purchase a smaller-sized investment property just so they can get into the market. However, if purchasing the property limits your capacity to build your wealth, then you may be better off finding a JV partner and purchasing a larger property together.

For example, if your deposit is too small, then consider a JV partner who can contribute and increase the overall deposit. Your combined borrowing power may also allow you to borrow more and purchase a better returning investment property.

Like all good things in life, there are risks associated with joint ventures, especially if you fail to dot your i’s and cross your t’s

If you’re set on purchasing an investment property on your own, be sure to consider its size. One investor purchased a studio apartment that was very small, and she struggled to obtain finance for it. The end result was an LVR of 60%. Had the apartment been 20sqm larger, the LVR would have been greater.

Remember, lenders’ policies and criteria are constantly changing in response to market conditions and pressures. It’s always best to adopt a conservative approach and to stick with the types of properties that you know are the least risky – and which banks will be most comfortable providing finance for. That way, you’re unlikely to be caught out and unable to secure a loan if they tighten their belts. Seek expert advice from your accountant and solicitor as to whether joint ventures are a good buying strategy for you.

Buying a property in a JV can give you the ability to leverage more from the investment than if you purchased a smaller property on your own. As I said, I have embarked on many successful JVs throughout my years of property investing, for a myriad of reasons, especially in the early days when building our portfolio.

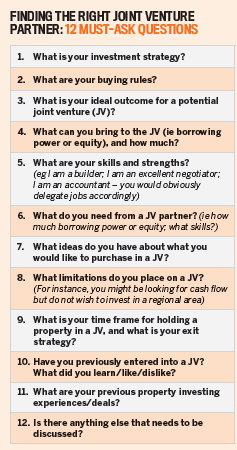

How to find the right joint venture partner

Finding a JV partner may not be as diifficult as you think. You can always start by discussing your intentions with like-minded friends, colleagues and family members and see what kind of reaction you get.

Investment programs and investor groups are also great places to meet similar, goaloriented investors who you may be able to partner with. It’s essential that you select a JV partner who has a strategy that aligns with yours, otherwise you may find that their agenda is not congruent with yours or beneficial for you.

When you’ve found the right person and you’re ready to enter into a JV, it’s important that you discuss all of your goals and your proposed outcome with your partner upfront as this helps to minimise any complications later on.

I have embarked on many successful joint ventures throughout my years of property investing … especially in the early days

Many successful JVs establish a minimum time period that each party must commit to, such as five years, at which time either party can commence negotiations to either buy each other out or extend the JV partnership.

Whatever your plans, it’s important to have a legal contract drawn up outlining the rules and responsibilities of each party. It’s also important to decide what will happen if an unexpected situation occurs, such as illness, divorce or death.

This is vital, even if you are investing with someone you truly trust, such as a close family member, because situations can and do change, so it pays to be prepared in advance.

Also, if you don’t feel comfortable discussing these types of situations initially with your JV partner, how are you going to cope if and when an unexpected situation arises?

How to structure your joint venture investment?

Joint ventures can be structured in two ways: as a ‘joint tenancy’ or as ‘tenants in common’.

In a joint tenancy, ownership of the property would pass to the other owners upon one partner’s death. In a ‘tenants in common’ structure, ownership can be held in equal or unequal shares (eg John 50%, Mary 25% and Jenny 25%), and upon one person’s death their ownership passes down to their heirs as per their will.

JV structures can get complicated, so it’s important to address these issues upfront and seek legal advice.

JV structures can get complicated, so it’s important to address these issues upfront and seek legal advice.

Can joint ventures be used in the current market?

Absolutely they can, especially in areas like Sydney where property prices are high. A JV could enable you to purchase in Sydney and enjoy the benefi ts of the next upswing.

The other point to consider, however, is finance. You need to keep in mind that a JV, from a fi nance perspective, could hold you back.

This is because when you purchase a property, whether on your own or in tandem with someone else, you are considered responsible for the entire debt.

You need to consider your exit strategy and buffers, and what you will do if the market falls or if you can’t fi nd a tenant

Let’s say you invest in a property with a JV partner and the loan is $500,000. You might decide you are responsible for $250,000 each. The risk here is that when you, as an investor, go for another loan with a lender, say for another investment property or to buy your own home, most lenders will calculate all of the debt against you (the full $500k), but they may only take into consideration half of the rental income.

This is something that many investors don’t think about, and it can stop them from moving forward. There are a couple of lenders that do not do this, so it’s vital that, to find the right lender, investors speak to an experienced mortgage broker who regularly works with investors.

To summarise, when it comes to investing in property it is always important to consider a joint venture as it can enable you to get into the property market or to continue building your portfolio, when done right.

Ensure that your chosen JV business partner is on the same page as you, with common goals, and always seek legal advice when getting your agreement in place.

Helen Collier-Kogtevs is a bestselling property author and the founder and director of Real Wealth Australia

Helen Collier-Kogtevs is a bestselling property author and the founder and director of Real Wealth Australia