With an extensive background as a mortgage broker and property advisor, Philippe Brach was in the perfect position to offer advice to our reader...

This is what Brach recommended:

1. How can Terry use his equity to pay off his home loan more quickly?

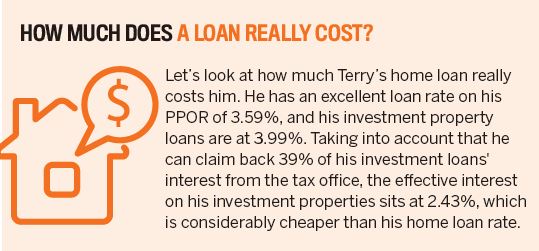

The short answer is that it's pointless to use equity in your investment property to repay your home loan. I hear many investors come up with this idea, erroneously believing that if you borrow against your investment property, the loan will be tax deductible. However, the tax deductibility of a loan is determined by what you use the loan for, not what asset secures it.

You can therefore borrow against your PPOR to invest in property (for the deposit, for example), and the amount you borrow to spend on your investment property is fully tax deductible. Also, you can borrow against your investment property to invest in another investment property, and this would be deductible.

However, if you borrow against your investment property to repay your PPOR home loan, the purpose of the loan is to help with a nondeductible investment (ie your home), and therefore you cannot claim a tax deduction on the interest. In other words, it makes no sense to extract equity from any loan to repay a PPOR loan.

As an aside, I would strongly recommend that investors who extract equity from their home to invest in property should set up a separate facility, rather than just top up their PPOR home loan.

As previously stated, the home loan is not tax deductible, so if you mix both deductible and non-deductible items in the same account, it becomes very messy to apportion how much interest is deductible and how much isn't. It can result in the ATO disallowing the whole interest amount if you can't prove convincingly how you calculated the apportionment.

Therefore, it's best to just keep your non-deductible loans separate from your deductible ones. It is also good financial management to keep your business affairs (ie your investment properties) separate from your private affairs (living expenses, home loan, etc).

Having said that, there are other easy ways to repay your home loan early. The most powerful one is to set up an offset account against your home loan.

An offset account is a fully transactional savings account that is linked to your home loan. At the end of the month, the bank will calculate the interest you owe by taking into account the net amount between your loan and your offset account. For example, if your loan is $400,000 and you have $50,000 in your offset account, then the bank will charge you interest on $350,000.

In other words, you will earn interest on your offset account at the same rate you pay on your mortgage. If you pay 4.5% on your mortgage, it is akin to receiving 4.5%, net of tax, on your savings – which is far better than the 1.5% you might get in a savings account (a profit on which you have to pay tax!). In Terry's case, on an income tax rate of 39%, the interest he would receive after tax in a normal savings account would only be about 0.9%.

However, if your home loan is with a no-frills internet lender, as Terry's is, then they will not offer an offset account. In this case, you can set up a current account for your normal monthly transactions (incoming salary and expenses), and any money left over at the end of the month can be transferred to pay down your loan, leaving the current account with a minimal balance. If large unforeseen expenses need to be paid, the redraw facility of the loan (which is not fully transactional) can be used by transferring money to your current account to settle these bills.

Another tip is to pay your home loan fortnightly rather than monthly. Lenders calculate interest on a daily basis, so it makes sense to make an additional payment in the middle of the month, as it will help shorten the life of your loan.

2. Should Terry transfer his properties into a trust to pay less tax?

Transferring properties to a trust is akin to selling the assets. It triggers a change of ownership, which means Terry would be liable for capital gains tax as the seller – and, as the purchaser, the trust is liable for the stamp duty.

The tax deductibility of a loan is determined by what you use the loan for, not what asset secures it

There are very few exceptions where there is stamp duty relief; they're usually limited to the split of assets following a divorce or death of a spouse. However, capital gains tax might still be payable. Terry would need to get formal legal advice on this subject.

Even if you decide to transfer your properties to a trust, despite the issues described above, you will face further hurdles. A standard newish property with an 80% loan-to-value ratio mortgage would normally generate a tax loss, which you cannot distribute from a family (or discretionary) trust. Tax losses remain quarantined in the trust unless you have other income in the trust to ‘soak up’ these losses.

You can use a unit trust, where negative gearing is still possible, but then you have no flexibility as to who benefits from the distribution, as this is dictated by the unit ownership in the trust.

Furthermore, the capital gains discount of 50% is not available if a property is in a discretionary trust.

In other words, it is unlikely to be beneficial for Terry to transfer a property he owns into a trust, be it a unit trust or a discretionary trust. Trying to use a hybrid trust, which has common features with both a discretionary and unit trust, won't be an option either, for the same reasons – plus, banks are very reluctant to lend to hybrid trusts.

It should be noted that, in Terry's case, his wife does not work. He owns all the properties in his own name, which entitles him to all the tax deductions. So the current structure he has in place appears to be optimal from a tax point of view in his current circumstances.

Transferring properties to a trust is akin to selling the assets. It triggers a change in ownership, which means Terry would be liable for capital gains tax as the seller

3. In a broader sense, what should Terry's strategy be going forward?

There are a number of aspects to consider, including borrowing capacity, loan structuring and risk management.

While Terry did very well to acquire four properties, he currently has no borrowing capacity to keep investing or even to refinance, given the tightening of lending criteria. In addition, his wife is expecting a child, which will further decrease his ability to borrow or refinance.

His current loans are very competitively priced, so there is no reason to be refinancing in the short term. An issue might arise later when his investment property loans revert to P&I, as he may have no option to refinance elsewhere unless his financial situation changes. For example, his wife might go back to work at some point, or his salary might increase over time, allowing him to explore some options.

The next aspect is loan structure. Terry has three investment properties, mortgaged at attractive rates, all on an interest-only basis. He has a credit card, which is repaid in full every month, and he has no personal loans. His home loan is on a P&I basis with no offset account but a great rate of 3.59%, and he uses the redraw facility to minimise his interest cost.

Overall, Terry's loan structure is sound because it allows him to concentrate on repaying his most expensive debt first: his home loan.

Terry's properties are cash flow positive before tax, so there is no point in considering extracting equity from his home to set up a separate funding facility for the cash requirements of his investment properties.

In order to pay down his PPOR loan sooner, I suggest that Terry put all of his cash flow profi ts (after tax) into his loan.

Finally, a note on risk management. All three of Terry’s investment properties are in Tasmania – concentrated in the Hobart area – which is fi ne for now, but when the market turns in this location he will be exposed. It would be best for Terry to invest in other areas around Australia, as there are so many property markets peaking at different times. Spreading location risk is always the best scenario.

Again, in Terry's case, he has no capacity to invest in additional properties right now. However, if he were to sell a couple of his Hobart properties and reinvest in Victoria, NSW or Queensland, he would probably be able to obtain a loan for one property but would struggle to finance two properties to replace the ones he disposed of in Hobart.

In addition, he would have to pay capital gains tax on the sales and then pay stamp duty on the acquisition of the new properties. So, overall, he is probably better off keeping his portfolio as is.

He might want to sell one of them, if he feels the market is turning, just to cash in some of the value created in the current cycle. He could then use the proceeds to further pay down his PPOR mortgage.

The decision to sell one of the properties is purely a personal one. Does Terry prefer to lower his PPOR loan, or is he comfortable riding the ups and down of the property market in Hobart?

There are a number of aspects to consider in deciding a strategy, including borrowing capacity, loan structuring and risk management

In conclusion

Terry has done really well to create a portfolio of properties that have low loan-to-value ratios and good yields. His loan structure is good, interest rates are very competitive, and he is really on top of his PPOR mortgage. He is clearly on the lookout for ways to improve his debt levels, especially his home. The only way he can rapidly decrease his home loan is by selling one of his investment properties and paying down the home debt with the proceeds.

The potential weak point in Terry's strategy is that all of his properties are in one location. Given his current weak borrowing capacity, there isn't much he can currently do about this, but if his financial circumstances change and he becomes able to continue purchasing, I would certainly advise him to cast his net wider and focus on other locations in the future.

Philippe Brach is the CEO of Multifocus Properties and Finance