.jpg)

Fact: in a city like Sydney, inner-city period homes will almost always be a good investment.

“Every main city in Australia has a circle of heritage properties within a 15km radius, which historically have patterns of strong capital growth,” says John Kovacs, managing director of mortgagee and deceased estate portal NMDData.

But properties like this don’t always come cheap. In the harbour city, these types of homes will carry a seven-figure price tag – and the rental returns may only cover half of the mortgage repayments.

So how do you seek out quality yet affordable real estate opportunities in order to get ahead in the property game? As clichéd as it sounds, it all begins with location. You may not be able to afford the middle of the city, but there are sought-after pockets throughout every suburb.

“We’ve all heard it in a commercial sense, but location, location, location is critical. The property needs to be in a good location close to schools, shops, transport and recreational facilities,” Kovacs says.

“Quiet, leafy suburbs, or homes with ocean views and near parks and gardens, are the ideal settings.”

He also recommends investors look for growth corridors, which are areas where the government is spending money on infrastructure, roads, schools and public transport.

“The correlation between new infrastructure and property prices is a proven method and provides steady capital growth,” he says.

“Also, don’t be afraid to look outside your state for property investing. It’s a great way to diversify your investment portfolio and keep up with market trends and property cycles throughout the country.”

“The correlation between new infrastructure and property prices is a proven method and provides steady capital growth”

Look back to look forward

It’s all well and good to know the types of properties to search for. But with literally thousands upon thousands of suburbs Australia-wide to choose from, where should investors even begin?

This is where you really need to be focused on the numbers.

Start with the bigger picture in mind: where are all of the major cities in terms of their market cycle? CoreLogic releases national figures that are updated daily, which is a great place to start.

In the current market, investment activity is down across the board. Real Estate Institute of Australia president Malcolm Gunning has confirmed that the value of investment housing commitments “is at the lowest level since July 2013, when prices were much lower”.

“The continued decline in housing finance is reflecting the slowing market; APRA restrictions, which with hindsight were probably excessive; the fallout from the royal commission into banking; and concerns about changes to property taxation and its impact should there be a change in government.”

These threats and concerns are causing many investors to hit the pause button on their investment plans, but Jane Slack-Smith from Your Property Success says now is the time to “take opportunities to buy under the market value and lock in value”.

“Even though two of the biggest markets are struggling, there are still many good opportunities for investors,” Slack-Smith says.

“Even though two of the biggest markets are struggling, there are still many good opportunities for investors,” Slack-Smith says.

“There are even markets in Sydney and Melbourne that are still seeing growth, so don’t think that there is one state or even city market. There are markets within markets. And remember, these times of stagnant and slow growth will come and go; it is how the property cycle works. If you are investing for the long term, these short-term corrections shouldn’t concern you.”

Assuming you’re confident in your decision to move forward with your property goals, by now you should have settled on a shortlist of potential investment locations.

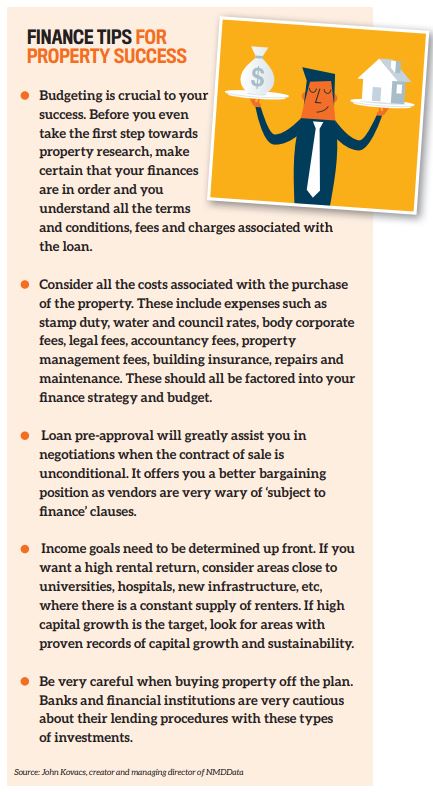

Kovacs suggests that once you have decided upon the major city you want to invest in – let’s say you’ve selected Brisbane or Hobart – you then need to research the changes in property prices and rental yields in each suburb or town of interest over the past three to five years. You can do this for free on the internet through data providers such as CoreLogic or Residex. “This will give you a good indication of growth patterns and an idea of cost comparisons of property sold within the area of interest. Local agents can also give you information about rental yields and vacancy rates, including the types of properties in demand for rental investment,” Kovacs says.

“Also, despite their sensitive and somewhat controversial nature, mortgagee and deceased estate properties may be worth the effort. These properties constitute real value in today’s ever-tightening property market, and can be purchased below market value. When buying a mortgagee or deceased estate property, careful analysis is required to determine its value. Supply, demand and location need to be carefully considered.”

Adding value

To be successful when buying an investment grade property, you need to have a clear plan for the property, which is why developing a strategy is so essential to your profit outcome.

Some investors prefer to have a hands-o property journey, where they invest in an asset and let a property manager handle the ins and outs of managing the home on a day-to-day basis. This is a ‘set and forget’ strategy.

Other investors choose to be more hands-on, opting to manufacture equity by investing in properties they can add value to.

To be successful with a renovation strategy, the property needs to have the potential for value to be added through upgrades.

“It should ideally have a neat and clean kitchen, bathroom and laundry facilities, because these are the most expensive areas to upgrade,” Kovacs says.

“If you’re considering a ‘renovator’s delight’ style of property, be very careful not to overcapitalise on the renovations. A decorated mansion in an industrial location is sure to fail. Prudent research is the key.”

Slack-Smith agrees. “Overcapitalising is a common problem in property investing. Going overboard with a property may not work out well if its location limits its value,” she says. “Your aim is to follow this golden rule: you need to make $2 for every $1 that you spend on the renovation.”

Of course, successful investing doesn’t end once you own your property and become a landlord. If anything, this is where your journey really begins, as there are a whole host of financial and tax-related tasks that will then jump onto your to-do list.

“Enlist a property manager to screen and locate a tenant,” Kovacs says.

“This is certainly money well spent. A property manager will prepare the leasing documents, arrange the bond, collect the rent, conduct regular inspections and also arrange for repairs to the property as required. Plus, these fees and charges are fully tax deductible against the rental income.”