James and Elizabeth are a married couple both aged in their mid-50s. James is a public servant and Elizabeth is a school teacher; between them they earn around $130,000 a year. They have two adult children and owe $115,000 on the mortgage on their home, which is worth around $550,000. They have no big debts, other than a $3,000 credit card limit, but they also have no big assets either – and with retirement just a decade away they're starting to worry about their financial future. What can James and Elizabeth do now to start planning for their future retirement?

FIRSTLY, James and Elizabeth should be congratulated for starting to consider their financial future – unfortunately many people don’t do this until it’s much too late to change the outcome.

That said, it takes time to build financial freedom and they only have about 10 years or so ahead of them before retirement, which does make it a little more difficult compared to if they had started planning when they were in their 30s or earlier. The scary fact is that the vast majority of Australians won’t retire with enough superannuation to see them through the remainder of their lives. This is because the average male’s superannuation balance is about $200,000 at retirement in Australia and a woman’s is about $100,000, and because we’re all living longer our super nest eggs need to financially provide for us during some 20-plus years of retirement.

So, if they are to enjoy financial freedom during their twilight years, James and Elizabeth will need to grow a significant quality asset base over the next 10 years, which will include their home, superannuation and investment properties. Needless to say, the number of properties they have in their portfolio on retirement won’t be anywhere near as important as the net value of those assets and the total rent achievable.

The thing is, to achieve financial freedom, they will need to do things differently to how they have done them in the past. They will need to invest in high-growth properties that generally have negative cash flow, as they don’t have a lot of time on their side to see the wonders of compounding growth work its magic.

This means James and Elizabeth will have to budget and sacrifice a little now so they can enjoy their retirement later. If they don’t, the alternative is that their golden years will be defined by money worries as they struggle to make ends meet on their pension and their inadequate superannuation balances.

Financial freedom is a goal for many people, but it is something that very few achieve. In fact, James and Elizabeth will need to do things differently to the majority of Australian property investors. Statistics show that of those who buy an investment property in Australia, 50% end up selling their property within the first five years, and of those who retain their properties, close to 90% never own more than one investment property. And of course one investment property is not enough to gain financial freedom.

So, with only a decade ahead of them, how can James and Elizabeth create a better financial future? Let’s consider some options for them…

TAKING STEPS TOWARDS FINANCIAL SECURITY

The first step for James and Elizabeth is to gain a sound education in investing, tax, superannuation and property. In particular, they must understand the power of leverage because it will be leveraging the equity in their home, and borrowing to buy high-growth properties, that will help them secure their financial future.

Secondly, they should gather a team of professionals around them who can offer sound investment advice. Their advisors should be independent and unbiased and not salespersons

or marketers trying to sell whatever shoddy, second-rate property they’ve got on their stock list.

This team should include an independent property strategist who can project manage their investment strategy, as well as the other consultants; a finance broker to help them through the maze of lenders; a financial planner who can discuss concepts such as self-managed superannuation funds (SMSFs) and insurance with them; and a property-savvy accountant.

Early in the piece James and Elizabeth will need to gain a better understanding of their current financial position – money warts and all! Questions that they need to know the answers to include:

• How much spare cash do they have to fund investments?

• What is their borrowing capacity?

• How can they improve this?

"Because they’re starting their investment journey late in life, they don’t have the luxury of time to make mistakes"

James and Elizabeth will then need to (with the assistance of their property strategist) build a strategy to accumulate the assets they will require to work towards financial freedom. They will need to take the following actions:• Prepare a comprehensive budget so they can see where they can increase their cash flow to help them invest.

• If James and Elizabeth are going to take on debt during the accumulation phase of their game plan, they’re going to have to focus on their incomes and spending

so they don’t get into financial difficulty.

• They’ll need to set up the right loan structures, including a financial buffer and an offset account, which is where it’s likely they will deposit extra savings to help minimise interest repayments on their home loan.

• James and Elizabeth could also consider filing for a PAYG variation. This way, rather than receiving a tax deduction at the end of the year, they will have more cash flow throughout the year to help finance their investments. They may put these extra funds into their offset account, which will again minimise their interest payments.

• I would recommend they make interest-only payments on their home loan and use the savings in repayments to fund investment loans – this way they can earn 10% (6% capital growth plus 4% yield) on their investment rather than paying off their home loan and saving, say, 4% in interest payments.

WEALTH-BUILDING: THE 3 PHASES

Before we go any further, it’s important that James and Elizabeth understand the three stages of building wealth, which are:

1. Accumulation phase

This is the stage James and Elizabeth can’t afford to get wrong. Because they’re starting their investment journey late in life they don’t have the luxury of time to make mistakes, therefore they must ensure that they own the right assets, meaning investment-grade high capital growth properties.

2. Consolidation phase

The consolidation phase involves slowly reducing the debt on their properties, which conversely increases their cash flow when they need it the most – in retirement.

3. Lifestyle phase

The lifestyle phase is all about enjoying their golden years, as well as managing and protecting their assets to make them last the distance.

BEGIN WITH THE END IN MIND

In order to make realistic plans James and Elizabeth must begin with the end in mind.

Questions they must now consider include: what do they want their life to look like after they retire? They also need to decide how much income they would like to have after tax, and then determine what size asset base they will need to fund their end game.

It’s important that they understand that it’s not about the number of properties in their portfolio. I’d rather own two investment-grade properties than four or five secondary ones. Successful property investment is about the net value of your properties and the cash flow that the portfolio can ultimately yield.

Part of this process must also include an assessment of their current financial position:

What can they expect from their superannuation?

» How much have James and Elizabeth got in super today?

» How much are they likely to contribute over the next 10 years, and what will their super balance be when they retire? This will give them an idea of the gap between where they are now and where they would like to be.

» Do they have the ability to move some of their super into an SMSF and then leverage it to buy a property in an SMSF? (They will need to see a financial planner before deciding whether to go down this investment route.)

What is their borrowing capacity for an investment property?

» Learn the value of their home.

» Understand how the banks will calculate their available equity: the value of their

home minus the existing loan($550,000 – $115,000 = $435,000) x 80% = $348,000.

» This means they could borrow up to $348,000 against their home as a deposit for their first investment plus some extra for a ‘rainy day buffer’.

» A professional mortgage broker will look at their other debts, but other than a small credit card limit there doesn’t appear to be anything to be concerned about.

» From these calculations, it’s likely James and Elizabeth will be able to borrow around

$700,000 in today’s stricter lending environment.

What are their financial habits?

» James and Elizabeth have two good incomes, but it’s not really about how much they earn as it is about what they do with their income.

» Do they budget?

» How much cash do they have left over each month?

» James and Elizabeth should set aside at least 10% of their income to invest (and to service the new debt).

It’s also key to understand their risk profile, but I assume James and Elizabeth are risk averse because they haven’t invested up until now and haven’t taken on much debt.

WHAT ARE THEIR OPTIONS?

The financial options for James and Elizabeth include:

1. Do nothing – They could just keep going as they have been, slowly paying off their home and contributing to super. They will retire with no debt on their home and a few hundred thousand in super, but that’s not an overly pleasant financial outlook.

2. Contribute more to super – They need to see a financial planner to understand what the end result could look like, but it’s unlikely to give them adequate returns to secure their financial future.

3. Invest – They could use the equity in their home and their steady incomes to borrow and invest in a number of properties over the next decade, with the aim of lowering their LVRs near retirement so they can live off the cash flow or increasing equity in their properties. They may not necessarily need to sell their properties when they retire because they should have significant equity and reasonable cash flow.

THE GAME PLAN FOR JAMES AND ELIZABETH

Given the limited information I have about their financial situation, but knowing their desire to get closer to financial freedom, I propose a ‘buy, renovate and hold’ strategy, which will allow them to speed up the journey by manufacturing some capital growth, then use the magic of leverage, compounding growth and time to build their assets.

• Year 1

In the first year they should buy a blue-chip investment-grade property in Sydney or Melbourne with the intention of manufacturing capital growth and rental income through

a renovation. This will serve as the foundation of their future property portfolio.

They should draw equity against their principal place of residence (PPOR), not by increasing their current home loan but by securing a separate equity release loan to the maximum 80% loan to-value ratio (LVR). This new loan would be tax deductible, even though it is secured by their PPOR, as the purpose of the loan would be to buy an investment property.

Their $700,000 budget would allow them to buy an apartment in a high-growth location for, say, $640,000, and give them a $60,000 renovation budget. They should borrow at 80% LVR against this investment property and keep the balance of their home equity release loan as a buffer in an offset account or line of credit, to help them sleep at night!

If done well, their property would likely be worth about $750,000 after the renovation, so they would have already manufactured significant capital growth, plus they would get a higher rental return and depreciation benefits. However, it’s unlikely the bank would allow them to refinance their investment property for 12 months or so.

A common reason why many first-time investors never get to their second property is that they make a poor first purchase – one that hasn’t delivered capital growth that they can use for the deposit on their second property.

Beginning investors often choose the wrong area, or the wrong property in the right area, and when it underperforms this scares them off or limits their ability to finance a second property.

Most people find it too hard to save the deposit for their next property, meaning they rely on the increasing equity in their existing properties to help subsequent purchases. If investors purchase a property that doesn’t experience strong capital growth, growing their portfolio will become increasingly difficult. That’s why a strategic approach to asset selection is critical.

"By having properties in different markets, they’ll be more likely to own a property in a market that is performing well"

• Year 2The second year will allow the value of James and Elizabeth’s home and their investment property to increase, while they put any extra savings and spare cash into their offset account to minimise the non-tax-deductible interest payments against their home. Using an offset account will give them more flexibility and control of their cash flow than repaying their home loan but will still have the same net effect on their interest payments.

• Year 3

During the third year of their investment journey, James and Elizabeth should be able to buy a second investment property. This would be achieved by refinancing both their existing properties to 80% or 90% LVR, which would give them the deposit and purchase costs for a second investment property valued at around $500,000.

The acquisition phase is all about using leverage to grow their portfolio, putting down as little deposit as possible and borrowing as much as possible, which allows them to grow their portfolio faster.

Once again, James and Elizabeth should add value through renovations, which will give them an instant burst of capital growth and higher rental returns.

They might also like to consider diversifying into a different major capital city. By having properties in different markets, they’re more likely to own a property in a market that is performing well, meaning they’ll be able to access equity to use when they want to either purchase another property or live off their equity in their retirement years.

• Year 4

The fourth year of their investment strategy is all about hibernation and allowing the magic of time and compounding growth to increase the value of their properties.

• Year 5

In the fifth year of their strategy, James and Elizabeth should buy a third investment-grade property. Based on today’s lending criteria, they are likely to be able to afford a property worth around $500,000.

Again this can be achieved by refinancing their existing properties at 80% LVR, giving them all the funds they require for their deposit, acquisition costs and the cost of renovation.

• Years 6, 7, 8 and 9

When James and Elizabeth get to the consolidation phase of their wealth building strategy, this is the period that will allow their properties to increase in value while at the same time they are reducing their debt by lowering their overall LVR.

It would make sense to first reduce the non-tax-deductible debt on their home loan, but rather than using their spare cash or savings to pay off their home loan, I would prefer to see them put their funds into an offset account. This will have the same effect on their interest payments as paying off their debt, but will keep them in control of their cash flow.

Think about it… I’d rather have a couple of hundred thousand dollars sitting in an offset account, which will give me control of my funds if the banks changed their lending criteria, than have paid off my loans and be beholden to the banks.

During these all-important years the couple should regularly review the performance of their portfolio to make sure it’s performing optimally.

• Year 10

In the 10th and final year of the strategy, James and Elizabeth will retire. There may be some tax benefits to staggering the years in which each of them stops working, so they should discuss this with their accountant. At this stage, they should again assess their final financial position.

Our graph (see opposite page) suggests that, based on average capital growth of 7%, and after adding value through renovations, at the end of the 10-year period of their game plan James and Elizabeth will own just over $4m worth of real estate (including their home) and have less than $2m worth of debt. These figures assume they will not have managed to save any of their wages over the decade and used the money to pay down debt.

Despite all the assumptions that we may have made along the way, it’s really only at this point in time that they will be in a position to see how accurate our assumptions were and decide whether they will be in the financial position to keep all of their properties or instead will need to sell a property to reduce debt and retain the others as a cash machine.

The good news is that if James and Elizabeth follow the outlined strategy, they will have a substantial asset base and a relatively low LVR, with significant funds sitting in their offset account, meaning they will have many more choices than if they had not invested.

RISK MINIMISATION

Of course, any investment strategy involves some level of risk, and this is especially true for James and Elizabeth, who only have 10 years to grow a sufficiently large property portfolio to help fund their retirement.

As I’ve already explained, one way of minimising their risk is to have a financial buffer in place (with funds in an offset account) for their personal needs as well as for any unexpected investment expenses.

This will allow them to keep their properties well maintained and to cope with any unexpected maintenance or vacancies.

Considering James and Elizabeth work in stable professions, they are unlikely to lose their jobs, but they should still consider taking out income protection and life insurance as well as landlord’s insurance to protect their interests.

I’d further recommend that they speak to their accountant before purchasing their properties to ensure they buy them in the most tax-effective manner. They should also arrange for depreciation schedules to ensure that they claim the most in deductions, which is especially important if they’re undertaking renovations, as recommended in their investment plan.

James and Elizabeth also need to consider estate planning because, while we never like to talk about it, it’s important to plan to look after their family (their spouse and children) in the event either of them dies early. They should see their solicitor and prepare a will, choose executors and organise a power of attorney.

"James and Elizabeth need to buy investment-grade properties that will outperform the general market"

Finally, it’s important that James and Elizabeth treat their investments like a business and regularly review their portfolio with their property strategist to track its performance, ensure that they have the right loans and the best interest rates, and assess when they’re ready for their next acquisition.

FINDING THE RIGHT PROPERTIES TO SECURE THEIR RETIREMENT

I’m conscious of the need for their newly acquired investment properties to deliver passive income in a relatively short timeframe, but in general it takes the average property 15 years to double in value.

This means James and Elizabeth need to buy investment-grade properties that outperform the general market to shorten this timeframe, and then accelerate the growth of their assets by manufacturing capital growth through renovations, as previously recommended.

Their properties also need to be strong and stable. By strong I mean their investment properties need to grow at wealth-producing rates of return, and by stable I mean they don’t fluctuate significantly in price.

"Their properties also need to be strong and stable. By strong I mean their investment properties need to grow at wealth-producing rates of return, and by stable I mean they don’t fluctuate significantly in price."

While many people would suggest paying off their home before they retire, instead I’d suggest using their funds to invest. In 10 years they will still have a $110,000 mortgage against their home, but this property may have increased in value to over $900,000, so their LVR will be low. They can then pay out their mortgage by using some funds from super or from the proceeds of selling or refinancing one of their investment properties.

On retirement, James and Elizabeth may also consider downsizing, so they may decide to sell their home, which isn’t subject to capital gains tax, and move into a smaller home or apartment, which means they won’t have a mortgage on their PPOR.

THE BOTTOM LINE

James and Elizabeth have left their run a little late and therefore won’t have the luxury of time to cover up the common mistakes most beginning investors make.

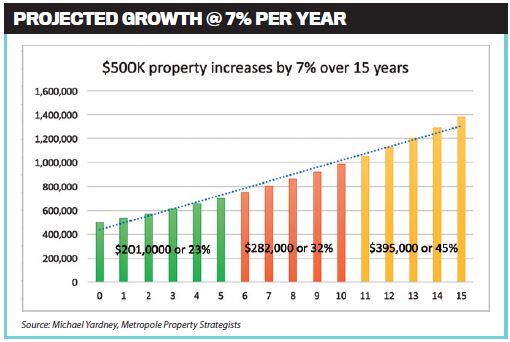

Time in the market is what delivers the most capital growth. As you will see from the above graph, if their $500,000 investment property increases in value by 7% per annum, it will be worth almost $1.4m in 15 years’ time, but almost half of this capital growth will occur during the last five years of this period.

This means that if James and Elizabeth could put off their retirement for a couple of years, or use their superannuation for the first couple of years of their retirement, before deciding to sell off one of their investment properties to fund their golden years, they’ll have time and compounding growth working longer for them.

It’s unlikely that in the 10-year timeframe they’ll build a sufficiently large asset base to completely replace their $130,000 annual income with rental returns. This would require them to own their own home with no debt against it plus $4.5m worth of investment real estate with no debt and returning a 4% gross yield, which would whittle down to 3% net after typical outgoings.

Instead, their aim should be to lower their LVR sufficiently to have enough positive cash fl ow to borrow a little bit more each year and live off the increasing equity in their properties. Alternatively, they could use this cash fl ow to supplement their superannuation income.

Either way, by implementing a sound investment strategy like the one I’ve recommended here, James and Elizabeth's financial future will be much rosier than it would have been if they’d done nothing at all.