When Joy Williams put her Sydney apartment up for rent and packed her suitcase to undertake a study sprint in Melbourne, she envisioned it to be, at most, a nine-month stay in the Victorian capital. However, as is often the case, life had bigger plans for her.

Once she began to realise the true potential of the extra cash flow she had been receiving from her home-turned-investment property, it wasn’t long before Joy started investigating real estate opportunities in Melbourne.

AT A GLANCE

Years Investing

: 12

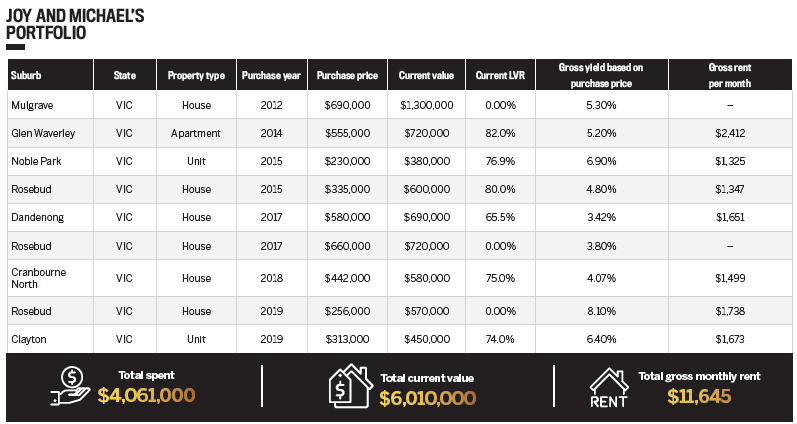

Current number of properties: 9

Portfolio value: $6,010m

“I had $100,000, half of which I saved and half my parents gave me for my first apartment in Sydney to live in. I purchased the apartment for $280,000 in 2008 and sold it in 2014 for $521,000,” Joy says.

After covering the cost of a renovation and paying back her parents’ loan with principal and interest, Joy had reached a momentous turning point – she had $300,000 in her pocket to start building a property portfolio.

The years that followed saw Joy and her husband, Michael, tackle a series of profitable renovations, and together they now hold nine investment properties across Melbourne.

Before

Landing a record sale

Though the profits have been substantial, Joy is quick to point out that a lot of blood, sweat and tears have been invested along the way.

“I remember some days my husband didn’t come home until 12 midnight because he was waiting for the cleaner to finish cleaning so he could hang the blinds, with furniture staging and a photo shoot scheduled for the next day. I drove 30km in my lunch break to the house one day to ensure the furniture staging went OK too,” Joy says of the large-scale renovation they did on a house in Frankston North. This included doing a full kitchen transformation, adding another bathroom and creating an en suite.

After

Joy and Michael bought their Huntingdale property under market value and achieved equity growth of $155,000 when they sold the renovated home just a year later

When Joy and Michael first bought the property in 2013 for $275,000, it was teeming with the kind of rich potential that comes with a generous 690sqm land allotment. They retained the property’s existing tenant and applied for a plan and building permit to develop a second house in the backyard.

However, by 2017 house values had skyrocketed in the suburb, and rather than diving into developing the second house, which could have delayed the sale date by eight to 10 months, the couple decided it was an opportune time to focus on renovating the existing property.

A quicker turnaround would allow them to sell and move on to another project while the market was still performing well.

“We vacated the tenant and did the renovation in 10 days. Thanks to my husband, who is a cabinet maker by trade and also very passionate about renovation, and super organised, we worked together very, very hard,” Joy says.

“Then we turned the three- bedroom, one-bathroom house into a three-bedroom, two-bathroom house, with a plan and permit to build another three-by-two house in the backyard.”

The sale of the property for $611,000 at auction in 2017 broke suburb records at the time, as it was also the only house that tipped over the $600,000 mark.

Before

After

Honing the selection criteria

Following the record-breaking sale, Joy came to believe that presentation and attention to detail were essential to achieving a high sale price.

Following the record-breaking sale, Joy came to believe that presentation and attention to detail were essential to achieving a high sale price.

“Always sell at vacant possession to ensure all-time access for potential buyers, and always pay for furniture staging – it does make a big difference,” she says of their property strategy. The couple also review the sales history of an area and interview three to four agents before they buy.

Choosing the right location comes down to an investor’s purpose, Joy adds, including whether they are renovating to hold or renovating to sell.

Some of the fundamental criteria that determine which properties they select include their budget, a suburb’s positive features (such as its proximity to schools and access to public transport), past sales performance of similar property types in the area, and deep research into current rental conditions.

“Our unit in Clayton was not in a liveable condition, and it was on the market for a long time, but we knew it was walking distance from Monash University and walking distance from the new M-City, which is a big shopping complex and cinema that is currently under construction and due to open in the first half of 2020,” Joy says.

The couple had purchased the property in Clayton in late 2018 for $313,000 and spent just $2,000 giving it a facelift. Following an influx of applications, it was tenanted within just three weeks.

“It’s all about pricing it right and providing what a tenant needs, and our renovations always give the place a nice, cosy feeling,” Joy says.

The lease term was also carefully considered: if the tenant moved out at the end of the lease, it would be timed with the start of the university season, giving the property a better chance of being snapped up more quickly and with a higher rental rate.

“We also obtained quotations to repaint the exterior of the unit block and repair the driveway and trim the trees around it. It was passed in AGM to proceed, so the complex will look much nicer and everyone will be benefiting from it,” Joy says.

In 2017, Joy and Michael purchased a beach house in Rosebud, Victoria, for themselves, which they renovated into four bedrooms and 2.5 bathrooms.

“Now, with the completion of the second dwelling on a separate title, all expenses [of the house] are well covered and capital grows fast,” Joy says.

Before

After

The importance of creating buffers

The couple’s secret to success is simple: they always base their calculations on worst-case scenarios. For instance, while the interest rate for their property in Noble Park was at 4.7% for interest-only loans at the time, they did calculations based on a 5.1% interest rate and a slightly lower rental rate. Currently, the rate sits at 3.89%, with a weekly rental income of $310, which is well above the buffer they gave themselves.

“Even if the bank will lend the money, [you] still need to ensure your out-of-pocket cost is minimised,” Joy says.

“Even if the bank will lend the money, [you] still need to ensure your out-of-pocket cost is minimised,” Joy says.

The couple have plans to renovate and sell their property in Cranbourne North, and while they are aware that the rental market is not as strong it was, they will still manage it as a rental for 12 months in order to receive a capital gains tax discount.

“We always aim to buy low. Our property in Huntingdale, before we purchased, had been on the market for almost 12 months and was not in a liveable condition,” Joy says.

“We offered $290,000 when the average price for similar properties in better condition was $350,000. We also offered no finance term and 30 days’ settlement.”

The couple immediately set to renovating the property, after which they rented it out for a year, then sold it at auction for $455,000.

The biggest lesson their ‘value-add’ strategy has taught them is that the best way to invest is when you retain control yourself, which is why Joy says she would “never buy off the plan” again.

“We bought a unit off the plan in Springvale, Victoria, which seemed like a very good price at $245,000 for a two-bedroom unit, but the construction took way too long and went way over the settlement date. Eventually we got our deposit back after going back and forth for over a year. At the end of the day, it wasted time and energy, and we could have used the money elsewhere and made a profit already.”